Whether or not President-elect Donald Trump has a mandate to pursue the huge changes he aspires to make is a matter of debate. He won impressively from an electoral standpoint, but the popular vote looks razor-close. What is practically inarguable is the fact that the...

Donald Trump's victory proved a shock to pollsters, gamblers, and stock & bond traders. Stock futures swooned 4.5% last night, but have since mitigated most of their losses. As of this writing the S&P 500 is down only 0.5%. On the bond side, fears that Mr. Trump's...

As the election draws near, stock and bond markets have been divided as to the significance of the outcome. A Trump victory injects policy uncertainty - something markets generally dislike. And a Clinton presidency provides more policy certainty, but with recent revelations from the FBI,...

This year's presidential race has destroyed any remaining remnants of normalcy in our country's quadrennial 'peaceful' transition of power. The breadth of its chaos has shattered precedents in civility, legality, political polling, expectations, and reporting. Both candidates have survived what almost certainly would have led...

We are pleased to introduce you to Langley Cumbie, our new Director of Client Relations at Beacon Wealthcare. She is busy invigorating our communications, event planning, marketing, and new client on-boarding processes.

We are pleased to introduce you to Langley Cumbie, our new Director of Client Relations at Beacon Wealthcare. She is busy invigorating our communications, event planning, marketing, and new client on-boarding processes.

Ever notice after a hurricane how some trees remain standing while others have fallen? More often than not it’s the rigid, unyielding trees that have fallen, while the more flexible survive. This fact of nature provides an important lesson for anyone who wants to plan for...

Source: “What Do Data on Millions of U.S. Workers Reveal about Life-Cycle Earnings Risk?” by Guvenen, Karahan, Ozkan & Song[/caption]

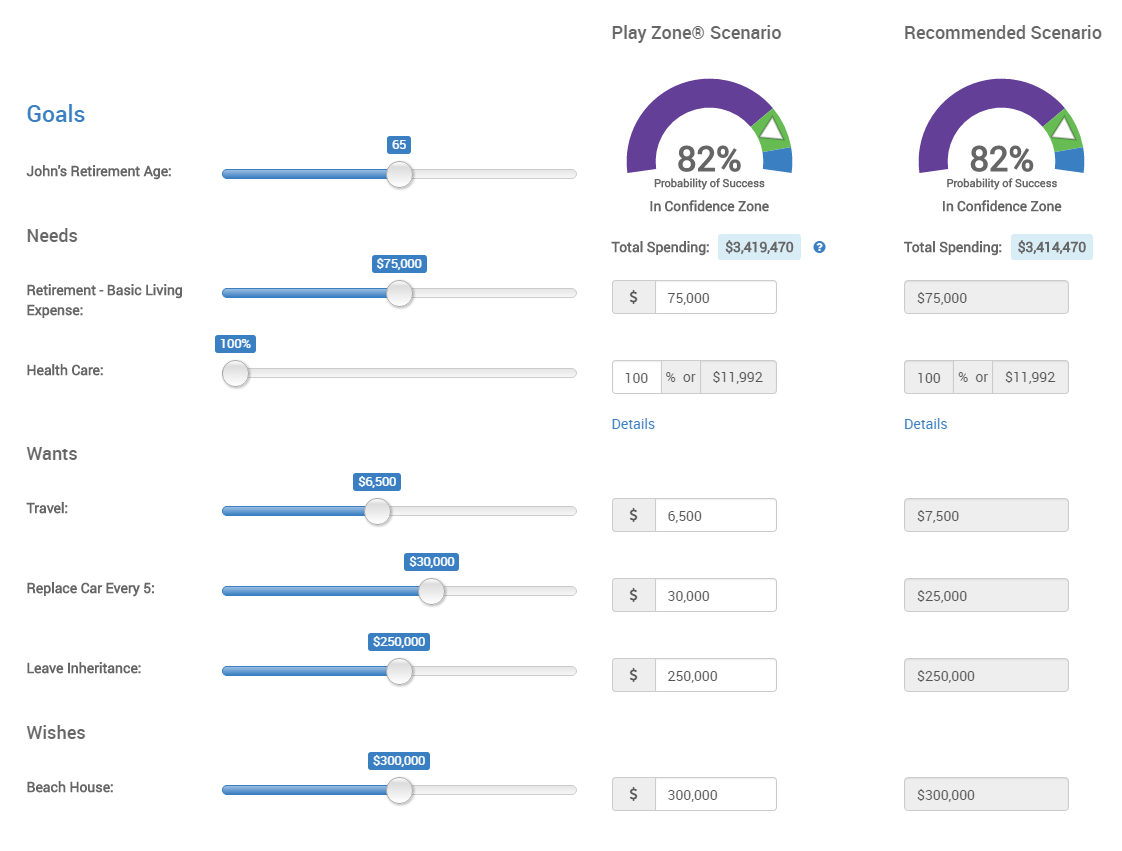

If you've been reading our Brief for any length of time you may have seen the term "lifestyle creep" come up once or twice. It's a fascinating concept with an equally emotive name, and it has all sorts of implications in the practice of long-term financial planning. Lifestyle creep is, more or less, the natural but potentially dangerous rising standard of living that occurs over the course of a lifetime as salaries increase with age (to a point). It's potentially dangerous, because if it creeps too much, then retirement becomes prohibitively expensive to fund at the level of your creeped up lifestyle, since your rate of consuming dollars will by definition have outstripped your rate of saving dollars.

Source: “What Do Data on Millions of U.S. Workers Reveal about Life-Cycle Earnings Risk?” by Guvenen, Karahan, Ozkan & Song[/caption]

If you've been reading our Brief for any length of time you may have seen the term "lifestyle creep" come up once or twice. It's a fascinating concept with an equally emotive name, and it has all sorts of implications in the practice of long-term financial planning. Lifestyle creep is, more or less, the natural but potentially dangerous rising standard of living that occurs over the course of a lifetime as salaries increase with age (to a point). It's potentially dangerous, because if it creeps too much, then retirement becomes prohibitively expensive to fund at the level of your creeped up lifestyle, since your rate of consuming dollars will by definition have outstripped your rate of saving dollars.