18 Nov 2016 What if Financial Planning Was More Inspirational and Fun?

For most folks, the idea of financial planning sounds like as much fun as doing lab work, going to the dentist, or creating a budget. And in truth, the way it is widely practiced only amplifies the perception that it is a painful exercise in all things uninspiring. As sensual creatures, we enjoy things that appeal to our senses and instinctively avoid the things that affront them.

When we focus primarily on the needles of lab work, the grinding at the dentist, and the compromises to lifestyle budgeting suggests, we quite naturally shun them. But when we look to the why of doing them, we become more willing participants in the process. Better physical health comes from lab work and dental care, and better financial health comes from budgeting. But they are still not much fun.

We do financial planning to accomplish important need-related goals in our lives; like educating our children, retiring comfortably, and ensuring we will not be a financial burden to them later in life. Some plans include more fun and inspiring goals as well like starting a career that is more aligned with one’s skills and passions, but offers less pay, taking a long-term sabbatical abroad, building a second home, or leaving the kids and grand kids a legacy to supplement family needs.

The Why of financial planning is to confidently achieve life goals, but these goals often seem far off and perhaps more than a bit unlikely, despite assurances from our advisor. But one thing is sure, when the why of financial planning becomes eclipsed by an overly mechanical process – it is a virtual guarantee that both your plan and process will become like needles and grinding, eclipsing the purposes.

We have discovered something quite profound at Beacon – planning must be inspirational and fun to be truly effective in people’s lives. By necessity, planning is a collaborative process that simply cannot be delegated to a financial professional for ‘management’ and ‘monitoring’ any more than a ship can cross the Atlantic Ocean given a single compass heading. Winds and currents will necessitate numerous adjustments along the way. Similarly, life changes, new challenges and opportunities will come along, requiring updates to the plan. These elements, when shared and analyzed regularly with your advisor, provide life to the planning process and give it new energy and direction. Without these interactions, the financial plan becomes nothing more than an uninspiring, lifeless, mathematical robot wobbling toward increasingly meaningless objectives set long ago into its programming.

So how can planning be made more fun and inspirational? It starts with goals – the why of planning. Great financial planning takes goal setting to a new level – an inspired level. No one gets really excited about projecting today’s lifesyle into the far off future – that’s no more inspiring than long-term budgeting.

But what if you asked yourself questions like:

- What would I do with my time if I no longer needed to earn a salary?

- What would I do more of if I learned I had only a limited time to live?

- What would I do if I knew I could not fail?

Every goal has relative importance to others and the quality of each ranges from acceptable to ideal. For example, a woman might be willing to work until she’s 65, but ideally she would love to to teach college-level finance starting in the fall. The immediacy suggests significant desire, but the apparent willingness to remain in a dull job for the rest of her working career for the assurance of security suggests resignation to her fate. What if, through an inspired planning process, this woman learned how she could best align her resources to spend from goals less important to her in order to meet her most important desire to teach college finance? Is that inspirational?

Effective planning is also ongoing and interactive. The best way we have found to keep clients engaged in the process is to make it fun. The old adage of the carrot vs. the stick could not be more appropriate here. For example, the stick of fear is a great motivator for convincing someone to buy and annuity or a CD, but not good getting them to engage in effective planning. In fact, the overwhelming reaction to fear is to run, and running’s not a plan.

We learn emotionally, through trial and error, much more than we care to admit. Behavioral psychologists have shown that most human learning takes place in the parts of the brain where senses and emotions are processed, far from the logic areas of the brain. So why would we expect a planning process founded on abstract questionnaires, calendar dates, and dollar amounts to be more exciting or compelling than blood work? When planning engages the senses in pleasing visual and tactile ways to provides instant results to important what-if questions, it actually becomes fun and compelling. Plans simply get better.

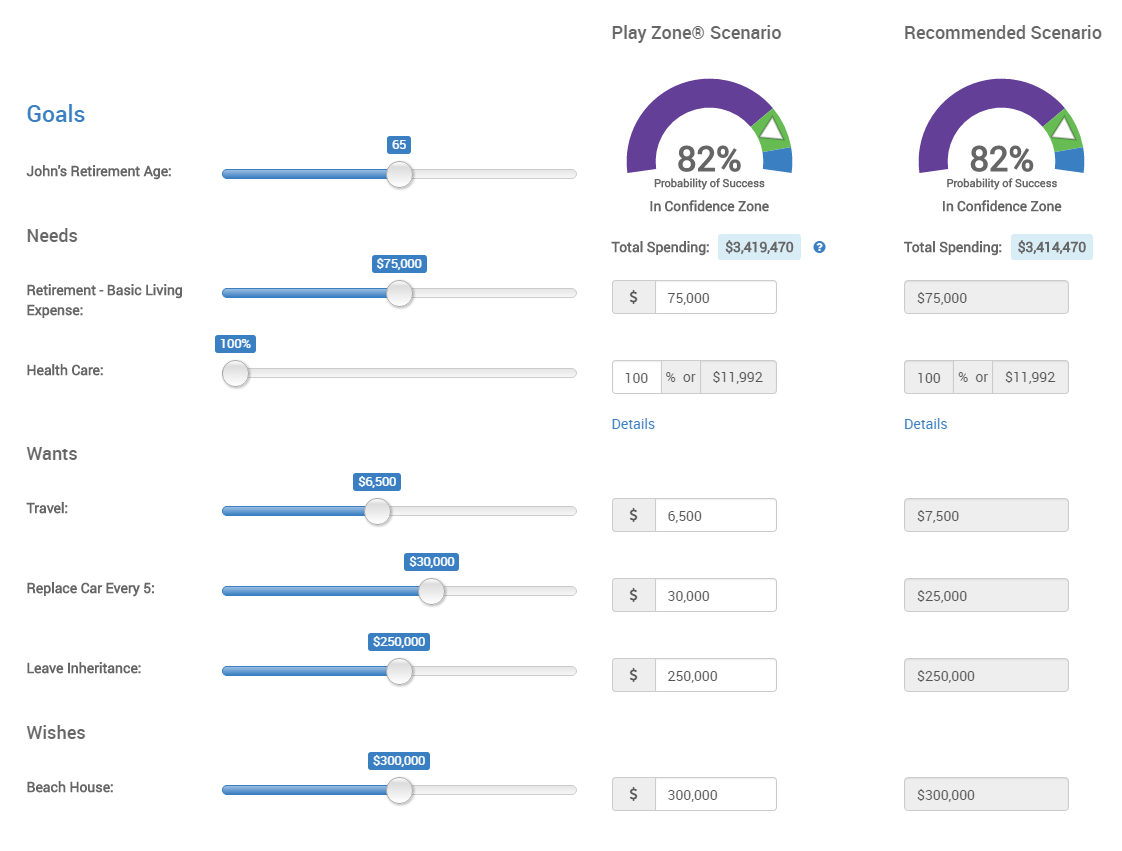

We use MoneyGuidePro® to draft and test our client plans because they share our same beliefs that good planning needs to be fun and engaging. Below is an example of the goal platform in MGP. Goals can be dragged into the plan and changed in priority by the client or the advisor at any time. But don’t let the simple interface fool you. The Monte Carlo probability testing engine of MGP is second to none in its robustness.

Another important feature of MGP is the ability to provide our clients with access to their plans, anywhere, anytime, and on any device. The software allows them to interact with their plans immediately when ‘what-if’ ideas come to mind. We find that clients add more goals and better align their methods of achieving them according to their priorities than we can accomplish in an hour at the table. Their imaginations are freed to manipulate their plan and resources literally in the palm of their own hands – very powerful. In the example below, John and Mary determine that they will not travel as much as they earlier thought when they build their beach house. They also will need to spend a bit more on their replacement cars after driving each one for 10 years. They move their sliders and find they can maintain confidence in their plan if they reduce travel by $1,000 each year and increase car prices by $5,000 each five years. All amounts increase with their own inflation assignments.

While we continue to look for ways to improve all aspects of our planning and management processes, we know that the best is not achievable if our clients are not 100% actively and eagerly engaged in the process of ensuring they confidently meet or exceed every goal they value. We are committed to ensuring just that.