03 Feb 2022 What Tax Forms Should You Expect To Receive?

Like it or not, on Monday, January the 24th, the Internal Revenue Service announced the start of our nation’s tax season. That’s the date when the IRS began accepting and processing 2021 tax year returns. Of all the seasons we could pick from–the holiday season, beach season, football season, fall leaf season, even allergy season!–I suspect that tax season is the least favorite for many of us.

And rightfully so, as filing our taxes can be a difficult and complex process. That’s true every tax year but the IRS continues to be plagued with staffing shortages, reduced funding and a backlog of 2021 returns which could make this tax season even more onerous than usual.

Perhaps one day someone will figure out how to streamline the IRS, simplify the US tax code and lower taxes across the board. Until then, here at Beacon, we’ll continue to work hard to minimize our client’s tax bills and simplify their filing process as much as we can. With that in mind, we thought it might be helpful to offer a summary of the different tax forms you might expect, and when you might expect them, based on the types of accounts you own and the different financial strategies or transactions we employed. I’ll be speaking specifically to our clients here at Beacon, but I think you’ll find this helpful even if you work with another advisor or are a DIY type.

Forms you might expect from Charles Schwab…

1099-INT or 1099-DIV: If you owned investments in a taxable (non-retirement) brokerage or trust account that paid interest or dividends you should expect to receive a Form 1099-INT and/or 1099-DIV. Note: You’ll receive a 1099-Int if you had money in a bank savings, shares or money market account or cd, too.

1099-B: If you or your advisor bought or sold investments in your brokerage account, or if you simply owned a mutual fund (but not ETF), you should also expect to receive a 1099-B. It will include a brief description of the securities you sold including the date you bought them and price you paid. If we did any tax loss harvesting during the year it will be reflected on your 1099-B. Your 1099-B will not, however, report any charitable gifts of stock you made during the tax year. Therefore, makes sure you remember to gather the letter or notification from your receiving charity along with supporting documentation like your 12.31 brokerage statement.

If your brokerage account is held at Charles Schwab you’ll receive a Form 1099 Composite and Year-End Summary Report. It should contain any 1099-INT, 1099-DIV and 1099-Bs for your brokerage account that you’ll need complete your tax preparation. You’ll either receive your tax forms in the mail via USPS or electronically via email depending on your election. Schwab expects these forms to be posted to your account or mailed by 2.16.2022. Note: you may receive other tax documents for IRA accounts (see below.)

1099-R: If you took a distribution, including RMDs (Required Minimum Distributions), from a traditional, SEP or Roth IRA, an annuity, profit-sharing plan, 401(k) or 403(b), insurance contract, or pension, you should expect to receive a 1099-R. Like the forms I mentioned above, you may receive these sooner but Schwab expects these forms to be posted to you account or mailed by 2.16.2022 at the latest.

In addition, if you completed a rollover from a 401(k) or other retirement plan to an IRA last year, you might also receive a Form 1099-R from your transferring provider. Don’t panic, as long as you completed a direct rollover of your account the transaction shouldn’t be taxable, just reportable. If you are unsure whether a distribution is taxable, it may be a good idea to consult with a tax professional.

If you gave money to a charity directly from your traditional IRA you made a QCD or Qualified Charitable Distribution. QCDs can be a powerful tax tool but they are tricky to report. It’s important to note that the amount of any QCD you completed in 2021 will be reported on the 1099-R you receive from your IRA custodian for that tax year. The tricky part is that your 1099-R won’t specify whether it was a regular withdrawal (or RMD) or a tax-free transfer to a charity (QCD.) When you file your Form 1040, you report the total IRA distribution on line 4a. Then report the taxable (non-QCD) amount on line 4b and enter “QCD” to indicate that the remaining amount is a qualified charitable distribution, which is not taxable. (If you had contributed your full IRA distribution to charity, you would write $0 and “QCD” on line 4b.) Also, make sure you keep an acknowledgement from the charity showing that it received your contribution in your tax records.

5498:If you made a contribution to a traditional, SEP or Roth IRA , your IRA trustee (Schwab in our case) is required to file this form with the IRS. You don’t need to file this form with your tax return. In fact, you may not receive a copy of this form until as late as May 31 of the year following the previous tax year. Do keep a copy of any 5498s for your records and do make sure to report any IRA contributions you made during the tax year when you file your return.

If you completed a Back Door Roth IRA contribution you’ll receive a 1099-R showing the distribution from your Traditional IRA that was converted to your Roth IRA during the previous year. You’ll also receive a Form 5498 that shows the contribution you made to the Traditional IRA and the amount that was converted to Roth.

These forms won’t come from Charles Schwab but are common, too…

SSA-1099: Look for one of these if you’re receiving Social Security benefits.

1099-S: You could receive one of these if you sold your home or any other real estate during the previous tax year.

5498-SA and 1099-SA: If you own an HSA (health savings account) you may receive one or both of these forms. Form 5498-SA reports contributions you made to your health savings account (HSA) for the prior year. If your HSA contributions are run through payroll at work, they are reported on your W-2, so the 5498-SA is more of an informational document and may not accurately reflect the tax year contributions. Form 5498-SA also reports your HSA balance as of Dec. 31 of the prior year. The 1099-SA is used to report any distribution of funds from your HSA during the prior year.

Note: For both HSA contributions and IRA contributions, the 5498 forms report contributions based on the calendar year, not your tax filing year. So if you make a 2021 contribution in the first few months of 2022, it is of utmost importance to communicate that to your CPA as there won’t be any supporting documentation until well after filing deadline!

Something potentially unique to your 2021 taxes…

If you received Advance Child Tax Credit payments and/or Economic Impact Payment #3 you should receive a Letter 6419 for the ACTC and a Letter 6475 for EIP #3. You’ll need to reconcile them on your 2021 return so make sure you provide these letters to your tax preparer or report the information accureatly when you file. Failure to do so could result in unessesary processing delays. Click here to read more on this.

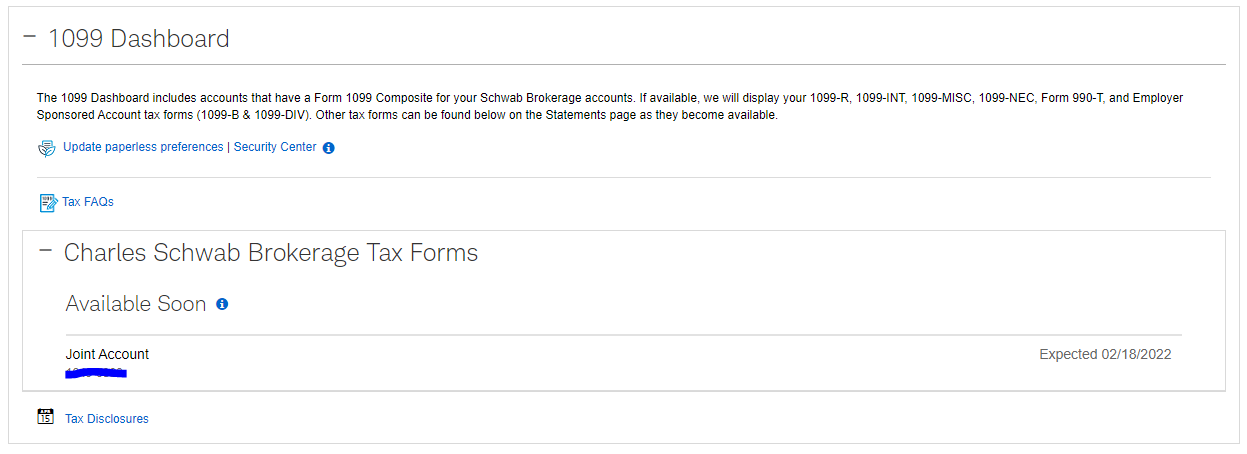

Introducing the Charles Schwab 1099 Dashboard…

If you have an account with Charles Schwab (through Beacon or otherwise) you have access to a handy new tool called the 1099 Dashboard. It’s located on their website and you can access it by logging into your account and then clicking on “Accounts” and then “Statements.” I like their new tool because it shows the tax forms you can expect along with their expected availability dates. Below is a snapshot of my 1099 Dashboard. Crystal and I will get a Form 1099 Composite and Year-End Summary Report for our brokerage account but no 1099-R since we didn’t take a distribution from a retirement account. You can check out your own 1099 Dashboard by clicking here to log into your Schwab account.

Taking the time to gather the appropriate tax documents ahead of time and communicating them effectively if you use a tax preparer can go a long way in taking some of the edge off of tax time. Of course, there are a multitude of other tax forms and documents I could have included in this Brief, but I wanted to keep this informative yet readable. I hope you find it helpful and please do let us know if you have any questions as you prepare your 2021 taxes.