01 Feb 2024 Another Reason It Pays to Delay Social Security

Any client of mine knows I am a proponent of delaying Social Security until age 70. There are times where it doesn’t make sense, such as poor health or a family history of shorter than average life expectancy. But, by and large I encourage my clients to delay. There is ample research that proves it results in improved outcomes (i.e., your money lasts longer), especially for those with long life expectancies. That is why Social Security is often referred to as “longevity insurance,” a term of art coined, I believe, by William Bernstein and William Richtenstein. Their research is largely responsible for the increased awareness of Social Security being a significant hedge against the financial risk of long-life expectancy.

It provides this hedge in three ways: First, Social Security benefits are backed by the U.S. government, so you’re not at risk of having that stream of income turned off, as portfolio income could be by poor market performance. Second, they are more tax-efficient than an equivalent amount withdrawn from a pre-tax retirement account. At most, 85% of benefits received will be subject to tax, but as little as 0% could be. Third, and finally, Social Security benefits are indexed to inflation, meaning that your benefits keeps pace as prices rise.

While past research proves Social Security’s viability as “longevity insurance”, a recent study in the Journal of Financial Planning titled “Which Social Security Claiming Strategy Generates the Highest Legacy Value?” seeks to answer this question: Does delaying benefits lead to a larger inheritance?

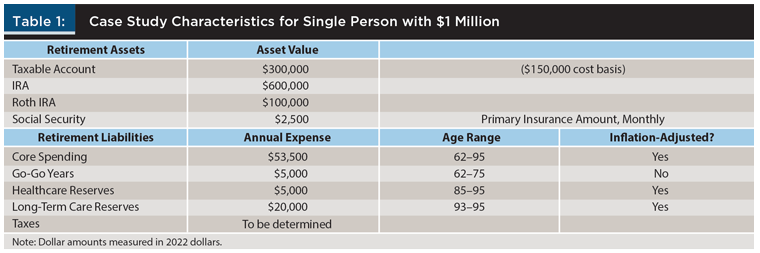

To find the answer, the researchers, Wade Pfau and Steve Parrish, used data going back to 1870 to run projections for a retired 62-year-old using the following financial information:

The Social Security amount listed ($30,000 annually) is the individual’s full retirement age (67) benefit. If he or she claimed at 62, their annual benefit would be $21,000; claiming at 70 would produce an annual benefit of $37,200. Federal taxes are not shown but they are factored into the projections, and it’s assumed the individual lives in a state with no income tax. Additionally, they ran three sets of projections, each using a different portfolio mix: 25% stocks, 75% bonds; 50% stocks, 50% bonds; 75% stocks, 25% bonds.

The researchers have two priorities: First, ensure the individual can meet the above spending goals until age 95, and second, to leave as large a legacy as possible.

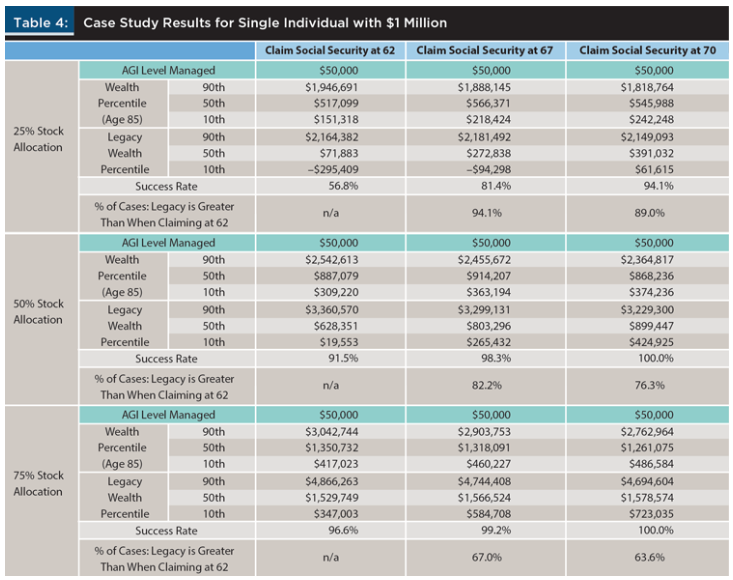

Here are their findings:

There’s a lot to digest, so I’ll summarize the output from the 50/50 portfolio (middle section).

Claiming Social Security at age 62 results in “success,” that is, having enough money to meet spending goals, 91.5% of the time. (As a reference point, we aim for 84% in our client projections.) Claiming at 67 results in success 98.3% of the time, and at 70, 100% of the time. As you can see, waiting to claim until at least full retirement age increases financial security, which accomplishes the first priority.

How about the second priority: leaving a legacy? As you can see in the row underneath “Success Rate”, claiming at 67 versus 62 yields a larger legacy 82.2% of the time, and at 70 versus 62, 76.3% of the time.

If you look over the results from the 25% and 75% stock portfolio, you’ll notice the findings are consistent: delaying increases both the success rate and the odds of leaving a larger legacy.

Two additional facts worth pointing out: First, if you look at the row titled “Wealth Percentile (Age 85)” you’ll notice the results are more mixed. That is, legacy value can be impacted negatively by delaying until age 67 or 70 and passing away at 85 or younger. Intuitively, this makes sense: delaying means you meet spending needs with withdrawals from your portfolio, and it takes time for your portfolio value to recover. Second, a higher allocation to stocks makes it less likely you will leave a larger legacy by claiming at 67 or 70 than at 62. Why? Because the returns of the stock market are unpredictable, while the delay credits offered by Social Security are both generous and guaranteed. Put another way, you are banking on unusually high stock market returns by choosing to claim at 62. Is this possible? Yes. Probable? No.

While the research proves that legacy is positively impacted by claiming Social Security later than age 62, its findings are important even if leaving a legacy is not a goal of yours in that it supports the argument that Social Security increases your ability to meet spending needs in the event of a long life expectancy.

Again, there are times where filing for benefits as early as possible makes sense, but those times are the exception, not the norm, and the research continues to show that waiting as long as possible to file for Social Security increases your long-term financial security.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.