14 Oct 2021 The American Families Plan: Will You Pay More?

The American Families Plan (AFP) is not yet law but we know what’s in it, at least in its current form. (I wrote a summary of it a few weeks ago.) There’s no guarantee the bill will survive the inevitable negotiations in the House and Senate unchanged, but for now, at least, we can estimate how it will impact taxpayers.

So, let’s cut the chit-chat and run some numbers to see if you, or a hypothetical taxpayer similar to you, will pay more in taxes under the proposed American Families Plan than you do under the current rules established by the Tax Cut and Jobs Act.

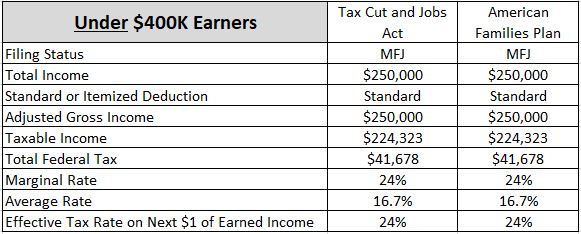

Under $400K Earners

President Biden promised that no one earning less than $400,000 will see their federal income taxes increase under the AFP, and our initial projections bear that out:

Assuming equal income, deduction, and credit inputs, you can see our hypothetical taxpayer’s federal income tax liability is the same in 2022 no matter which tax law governs. Federal taxes paid are the same, marginal and average rates are the same, and the effective tax rate on the next dollar of income (which accounts for how an additional dollar of income increases income taxes, capital gains rates, impacts deductions and credits, etc.) is the same.

The $250K amount for income is arbitrary. Increasing income to $390K, just below the $400K threshold, and the result is the same: no change.

There’s also no change for a retiree whose income is made up of taxable IRA distributions, Social Security, and capital gains, or a single parent with wage income of $125,000. There’s no direct impact on taxpayers below the $400K threshold, as President Biden promised.

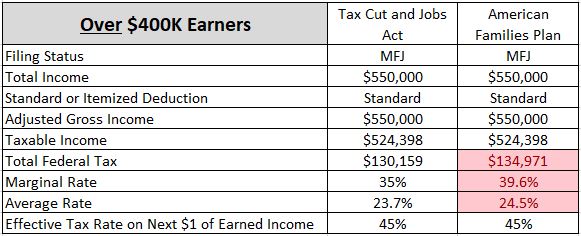

Over $400K Earners

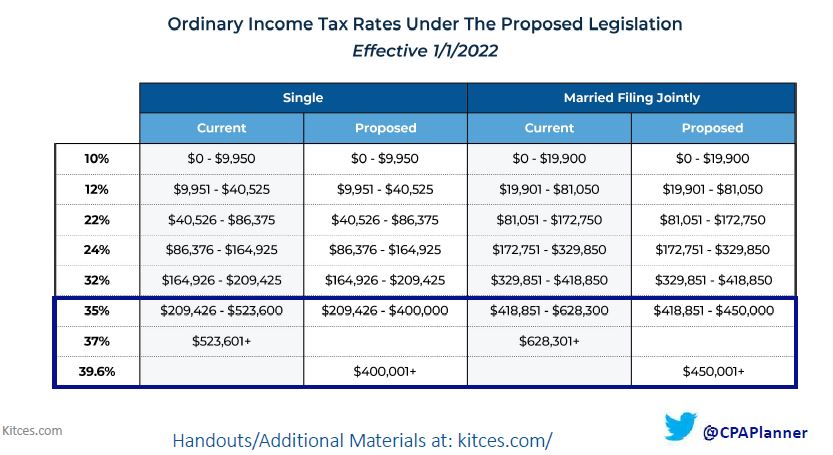

Over $400K is where you begin to see differences between the two laws. Here’s an image I shared a few weeks ago along with what I wrote:

“It’s when income rises over $418,850 (MFJ) that you begin to see changes. Current law taxes income from $418,851 through $800,000 at two different rates: 35% and 37%. AFP changes that, compressing the majority of income in the 35% bracket and the entirety of income in the 37% into a unified 39.6% tax bracket. In looking at the chart, it sticks out how small the 35% bracket is, meaning taxpayers can leap from 32% to 39.6% very quickly.”

A smaller 35% bracket plus a new top tax rate of 39.6% increases taxes for a married couple filing jointly that earns more than $418K or a single filer earning more than $400K:

As you can see by the highlighted boxes, our hypothetical taxpayer who earns $550,000 will pay roughly $4,800 more in federal income taxes. Their marginal rate, the rate at which each additional dollar of income is taxed by the federal government, rises to 39.6% versus 35% under current law. Interestingly, the effective tax rate on the next dollar of earned income is unchanged; they are both taxed at 45%, though for different reasons.

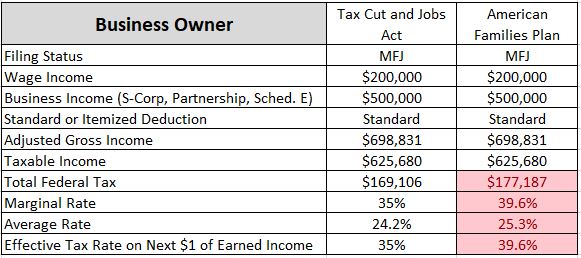

Business Owner

What about business owners? Here’s an example of one with $700,000 in total earnings (wages plus distributions). As you can see, their taxes will also go up:

The exact amount depends on how they receive their compensation, of course, but in my example, where an owner receives wages of $200,000 and distributions of $500,000, their federal tax bill will increase by $8,000 under the AFP. The marginal rate, average rate, and effective tax rate are higher across the board.

It’s clear, at least based on what we know about the American Families Plan right now, that federal income taxes will rise for the top 1-2% of earners. (Click here for an easy way to see which percentile your income places you in.) By how much depends on the kind of income you receive (wages, distributions, capital gains, etc.) your deductions, and the nature of any credits you are eligible for. But the bottom line is that taxes are projected to rise for those with earnings about $400,000.

Knowing this, what should you do if you’ll be impacted? At this point, we don’t recommend taking significant action beyond gathering information and evaluating strategies that might help if the AFP becomes law. The kinds of strategies that may work revolve around increasing earned income this year (to the extent you can) when rates are lower and pushing off deductions into next year when rates may be higher.

As always, contact us if you have specific questions about how the American Families Plan might impact you.

Have a restful weekend!

*This is not tax advice. Please consult your tax professional. Projections are assumed to be accurate but given the ever-changing nature of the American Families Plan, could be incorrect.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.