20 Oct 2022 2023 Contribution Amounts, Tax Bracket Changes, and Social Security Increases

Within the last 7 days, the Social Security Administration (SSA) announced the cost-of-living adjustment (COLA) recipients will receive, while the IRS released tax brackets for 2023. Add in projected retirement plan contribution limit increases, and next year you have three silver linings to the high inflation coursing through the global economy.

Let’s take a closer look.

Social Security COLA

The COLA for 2023 will be 8.7%, which means the average monthly benefit paid in 2022, $1,681, will rise by $146, to $1,827. Citizens who qualify for benefits and are between their full retirement age and 70, and who aren’t yet receiving benefits, will get the COLA plus delayed retirement credits (DRC) of 8%.

For those still working, the amount of income subject to the 6.2% Social Security tax paid via payroll deduction, will rise from $147,000 to $160,200. If your earnings regularly exceed the wage base limit, you will pay an additional $818 in Social Security taxes.

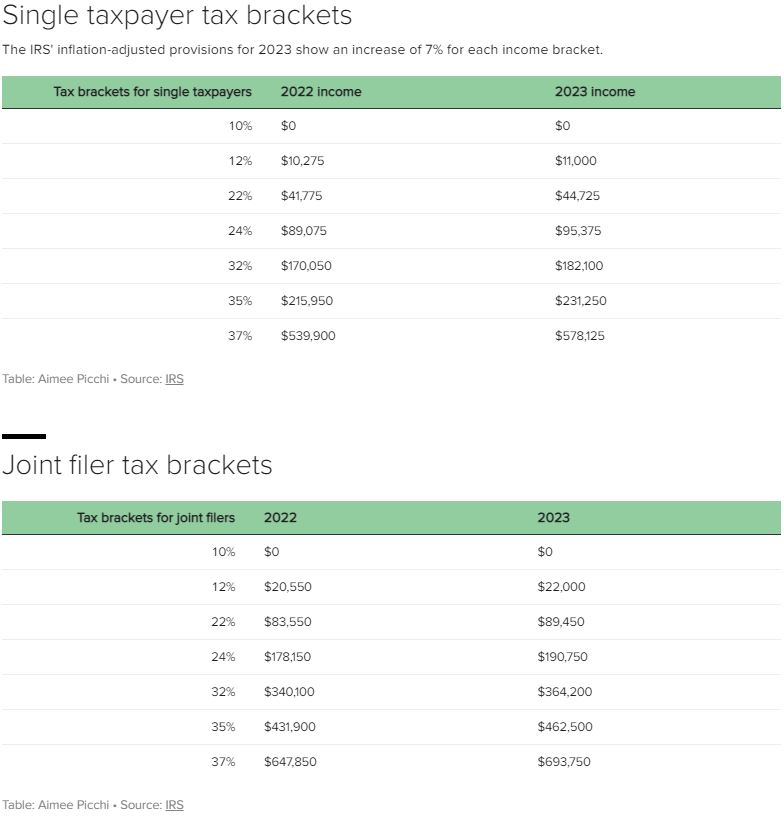

2023 Tax Brackets

On Tuesday night, the IRS announced a 7% increase to their tax brackets, meaning higher levels of income fall into each respective income tax bracket.

In application, this means a married couple filing jointly (MFJ) with taxable income of $400,000 in both 2022 and 2023 will pay about $3,000 less in federal income tax. One with $200,000 in taxable income will see their tax bill drop by $900.

A single filer (S) with taxable income of $200,000 will pay roughly $1,400 less in federal income tax. A single filer with $100,000 in taxable income will owe $435 less.

In addition to these changes, the Standard Deduction is increasing from $25,900 to $27,700 (MFJ), and from $12,950 to $13,850 (S).

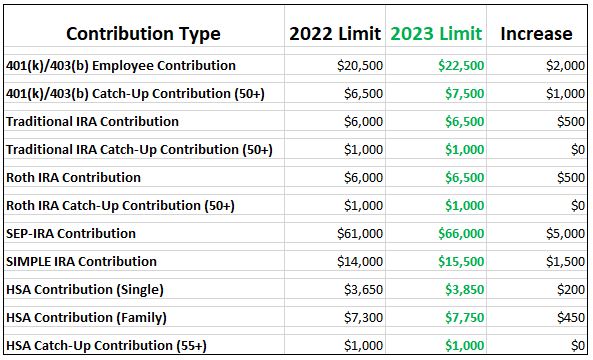

Retirement Plan Contribution Amounts (Projected)

While no official announcement has been made, we can make assumptions about what can be contributed to retirement accounts next year by looking at the inflation numbers. Here are some projections:

Again, these are only projections, and there are eligibility rules you must meet before contributing to these accounts, but we anticipate unprecedented increases in contribution limits.

While these silver linings don’t fully offset the increase in prices we’ve experienced over the last 12-18 months, they do soften the blow and provide planning opportunities, both for retirees and workers.

If you have questions, please reach out to us, and as actual contribution limits for 2023 are released, we’ll be sure to communicate with you.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.