16 Sep 2021 The 411 on President Biden’s “American Families Plan”

A little over a year ago I wrote a Brief about the tax plan Joe Biden was proposing during his campaign to be the Democrat nominee for President. Here we are, 13 short month later, and the White House has unveiled their new “American Families Plan” (AFP). There are differences between the two plans, some that are quite stark, and extreme differences from current tax law. As Jeffrey Levine, Chief Planning Officer for Buckingham Strategic Wealth, said on a webinar two days ago that dissected the new plan, as big a change to the tax code as Trump’s Tax Cut and Jobs Act was, what the White House is currently proposing is even bigger. Today I’ll cover what I believe to be the most impactful points for our clients–the new income tax brackets, the new capital gains tax rules, Roth Conversions/Back-Door Roth contributions, and the estate tax exemption. I’ll close with what’s not in the bill.

Three more things before we get stared: First, next time you see your CPA, any CPA, give them a hug (socially-distanced or otherwise). I can’t imagine the challenges they have faced over the last few years navigating a new tax law from then-President Trump, the short-term tax code alterations brought about by the pandemic, and now the American Families Plan. Second, many thanks to the aforementioned Jeffrey Levine and the entire team at Kitces.com, who spent hours unpacking the proposal and sharing what they learned on a webinar a few days ago.

Finally, I’ll say the same thing as I said 13 months ago: This is by no means a partisan review and will be an objective summary of the current proposal. President Trump’s Tax Cut and Jobs Act (TCJA) that passed at the tail-end of 2017 and provided the largest overhaul to the tax code in thirty years will be referenced solely for the purpose of history and comparison, not as an indication of right or wrong, better or worse.

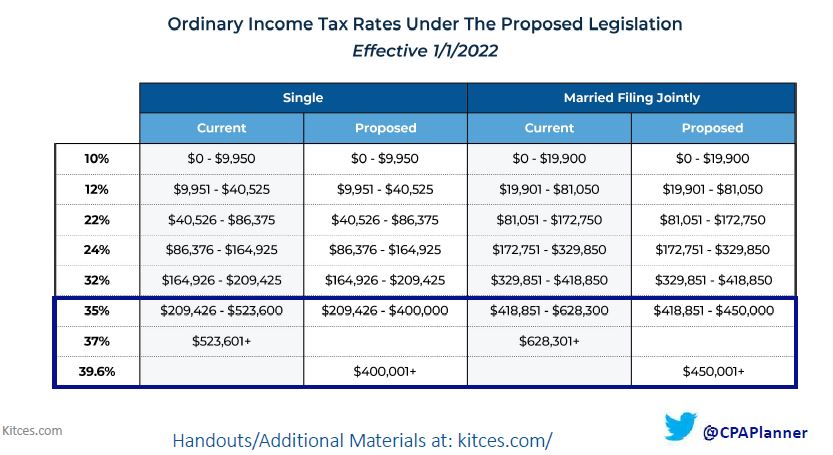

New Ordinary Income Tax Brackets

President Biden has consistently said that no person earning under $400,000 a year will see their income taxes go up, and he has stayed true to that with this bill. As you can see from the chart below, there are no changes to any of the bottom five tax brackets.

It’s when income rises over $418,850 (MFJ) that you begin to see changes. Current law taxes income from $418,851 through $800,000 (this figure is used only as an example. There’s no significance to it) at two different rates: 35% and 37%. AFP changes that, compressing the majority of income in the 35% bracket and the entirety of income in the 37% into a unified 39.6% tax bracket. In looking at the chart, it sticks out how small the 35% bracket is, meaning taxpayers can leap from 32% to 39.6% very quickly.

The changes aren’t isolated to married couples, though. Single filers will see every dollar of taxable income over $400,000 taxed at the highest 39.6% rate. Similar to MFJ, a portion of that used to be taxed at 35% and the rest at 37%.

It’s noteworthy to point out this tax bill brings back what’s commonly called the “Marriage Penalty.” That is, two individual filers earning $250,000 each will pay less in income taxes than if those same two filers got married.

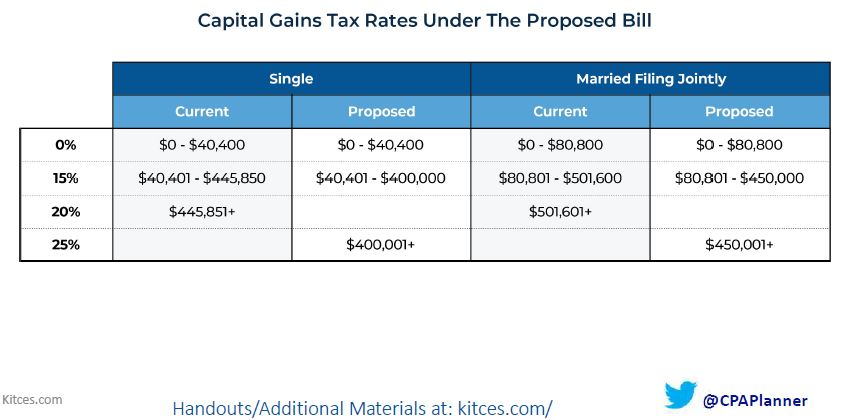

New Capital Gains Tax Brackets

On the campaign trail, Joe Biden indicated a desire to increase capital gains taxes for those earning more than $1,000,000 a year. Rather than receiving preferential 20% taxation, he wanted to see them taxed at the highest income tax bracket of 39.6%.

Neither of these wishes are included in the AFP. Rather, the highest capital gains tax will be 25% and will be assessed on single filers earning more than $400,000 and joint filers earning more than $450,000. In sum: lower rates, but also lower thresholds. More taxpayers will be subject to the new capital gains rates, but the cut won’t be as deep.

Interestingly, if this bill were to pass the new capital gains taxes would not be effective as of the day of passage, but going back to September 13, 2021, the day the White House released the proposal. The intent is to prevent taxpayers from accelerated long-term capital gains into this year at lower rates. There are certain exceptions, but most revolve around having a deal in place, contracts signed, etc.

It’s worth pointing out that those with earnings in the $400,000-$800,000 will feel the most significant impact from the tax law change. This is due to a double-hit of higher capital gains taxes and a greater portion of their income being subject to 39.6% taxation.

Roth Conversions and the Back-Door Roth Loophole

I said at the top that the AFP is a major tax overhaul. So much so that it creates a new category of income for tax purposes. Many of you are familiar with Adjusted Gross Income (AGI), less of you may have heard of Modified Adjusted Gross Income, and then of course there’s Taxable Income. The AFP introduces us to a new member of the family: Adjusted Taxable Income (ATI).

Let me say it again: Hug your CPA.

Adjusted Taxable Income is used in determining eligibility for Roth Conversions. A taxpayer(s) with ATI above $400,000 (S) or $450,000 (MFJ) will be prohibited from any kind of Roth Conversion whatsoever. This aspect of the bill doesn’t go into effect until 2032.

I don’t believe this piece of the bill is too impactful because Roth Conversions for someone in the highest tax bracket don’t usually make a lot of sense.

What is impactful is that this slams the door on any conversions of after-tax funds in retirement accounts beginning January 1st, 2022. There’s long been a loophole that allows high earners to make after-tax contributions to a Traditional IRA and then convert them to a Roth IRA, a strategy called a Back-Door Roth Contribution that essentially allows a high earner to side-step Roth IRA eligibility restrictions. This strategy would go away if AFP passes in its current form.

Estate Taxes

The AFP would reduce the federal estate tax exemption from $11.7M per person/$23.4M per couple to exactly half that: $5.85M per person and $11.7M per couple. This isn’t as dramatic a drop as many had feared and the vast majority of Americans will still pay no federal estate tax.

Especially noteworthy is that the AFP does not touch the step-up in basis rules. President Biden was hopeful of having this included but there is no mention of it in the bill as it currently stands.

Miscellaneous

While not comprehensive, because much of the “other” stuff won’t impact most of you, here are a few other items of interest: the AFP extends the increased Child Tax Credit monthly advance payments through 2025 for qualifying children and taxpayers, makes permanent the American Rescue Plan Act’s method of calculating subsidies for the Affordable Care Act, modifies the Qualified Business Income (QBI) deduction, establishes wash sales rule for cryptocurrencies, creates mandatory RMDs from IRAs with balances exceeding $10M (the “Peter Thiel rule”), and creates a 3.8% surtax on S-Corporation business profits for taxpayers with modified adjusted gross income exceeding $400,000 (S) or $500,000 (MFJ). The mechanics of this surtax are complex and deserve more explanation, I just don’t feel I have a good enough grasp of it yet to do that.

What’s NOT in the American Families Plan Tax Bill

No wealth tax; No adjustment to the limitations on deductibility of state and local income taxes (“SALT”); No “alignment of top capital gains rate with ordinary income tax rate”; No elimination of the step-up in basis; No phaseout of the QBI deduction.

In closing

First, do not take any dramatic action based on what’s in this bill. It still needs to pass, though Jeffrey Levine put the odds at “85%” during the webinar. Even if it does pass, it may look different than it does now. Please be cautious of any solicitations or strategies you hear about that are a reaction to this bill.

Second, as I just said, Mr. Levine feels a new tax law will pass this year. He comes to this conclusion because not passing a bill would be too politically damaging to the Democratic party.

Third, the American Families Plan highlights the importance of tax planning. As I said 13 months ago, you can be confident that no matter the tax landscape, whether expectations are rates will rise or fall, our commitment to tax planning never changes. As we learn more and get a better sense of what the bill’s final form may take, we will reach out to discuss proactive steps you can take to mitigate the impact.

As always, if you are a client with pressing concerns or questions, contact us. If you’re not yet a client, click here to learn more about our team and schedule a time to chat with one of us.

Now go find a CPA to hug.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.