07 Aug 2020 A Summary of Mr. Biden’s Tax Plan

With the Presidential Election just over two months away, I felt it would be helpful to review presumptive Democrat nominee for President Joe Biden’s tax proposal. This is by no means a partisan review and will be an objective summary of his current plan. President Trump’s Tax Cut and Jobs Act (TCJA) that passed at the tail-end of 2017 and provided the largest overhaul to the tax code in thirty years will be referenced solely for the purpose of history and comparison, not as an indication of right or wrong, better or worse.

You may remember the TCJA brought about a host of changes: it lowered tax brackets and increased the income required to move from one bracket to the next, suspended personal exemptions, doubled the amount of the standard deduction, capped itemized deductions for real estate taxes and state income taxes at a total of $10,000, made it more difficult to fall into the Alternative Minimum Tax, eased limits on itemized deductions for high earners by eliminating the Pease Act, increased both the eligibility for and the amount of child tax credits, and limited the amount of mortgage interest that can be deducted on debt taken on after December 16th, 2017. There were also changes on the corporate/self-employed side of things including the introduction of the “Qualified Business Income Deduction”. In short, it was a massive restructuring of the tax code.

Similarly, Mr. Biden’s proposal includes some dramatic changes while at the same time harkens back to pre-TCJA law.

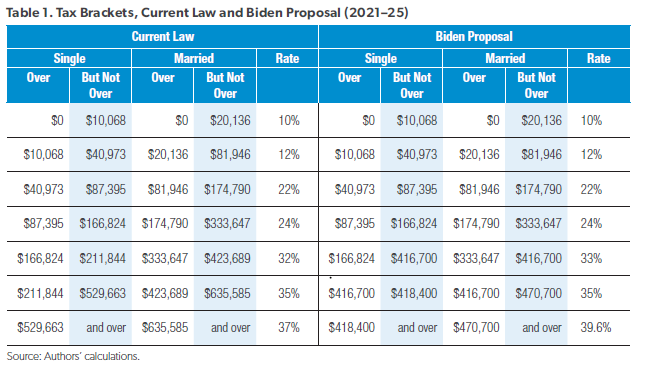

Let’s start by reviewing the proposed tax brackets. The chart below is courtesy of the American Enterprise Institute and shows current law on the left and proposed law on the right:

Mr. Biden’s proposal raises some rates, as you can see on the far-right column, and reduces income required to move from one tax bracket to the next as you get to the upper three tiers. The lower four brackets—10% through 24%—don’t change. The 32% becomes 33%, 35% stays 35%, and 37% becomes 39.6%, though at lower income levels. The latter two mirror pre-TCJA law.

One dramatic change Mr. Biden proposes is collecting Social Security taxes on earned income above $400,000. This would create a “donut-hole” where taxes for Social Security cease to be collected on income over $137,700 (2020 numbers) and then re-start once earnings exceed $400,000; Employees and employers would both be required to pay 6.2%. It should be noted that the lower number will increase for inflation while the upper number will not. Over time, the donut-hole will be devoured by inflation and all income will be subject to Social Security taxes.

The combination of increased rates and the re-introduction of the Social Security tax would essentially lift the top tax bracket to 45.8%, not including state taxes (which vary), the Additional Medicare Tax (.9%), and, potentially, the Net Investment Income Tax (3.8%).

The taxation of long-term capital gains (gains on assets held greater than 1 year) would also change but only for those with income above $1,000,000. Rather than receiving a preferential rate of 20%, these gains would be taxed at the taxpayer’s ordinary income tax rates. Additionally, the “step-up” in cost basis that occurs upon death would be eliminated.

Mr. Biden’s proposal also restores the Pease limitations, capping itemized deductions for those in higher tax brackets, and phases out the aforementioned Qualified Business Income deduction at certain income levels.

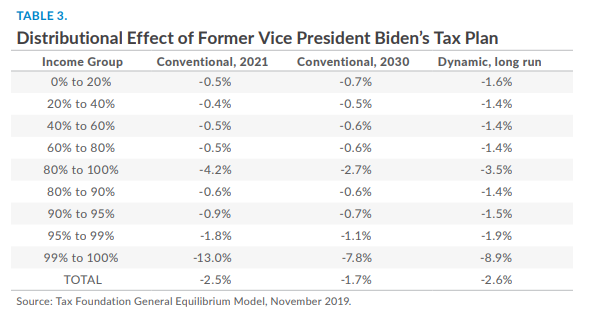

The cumulative effect on personal income, broken down by income group, is seen below. The chart is courtesy of The Tax Foundation:

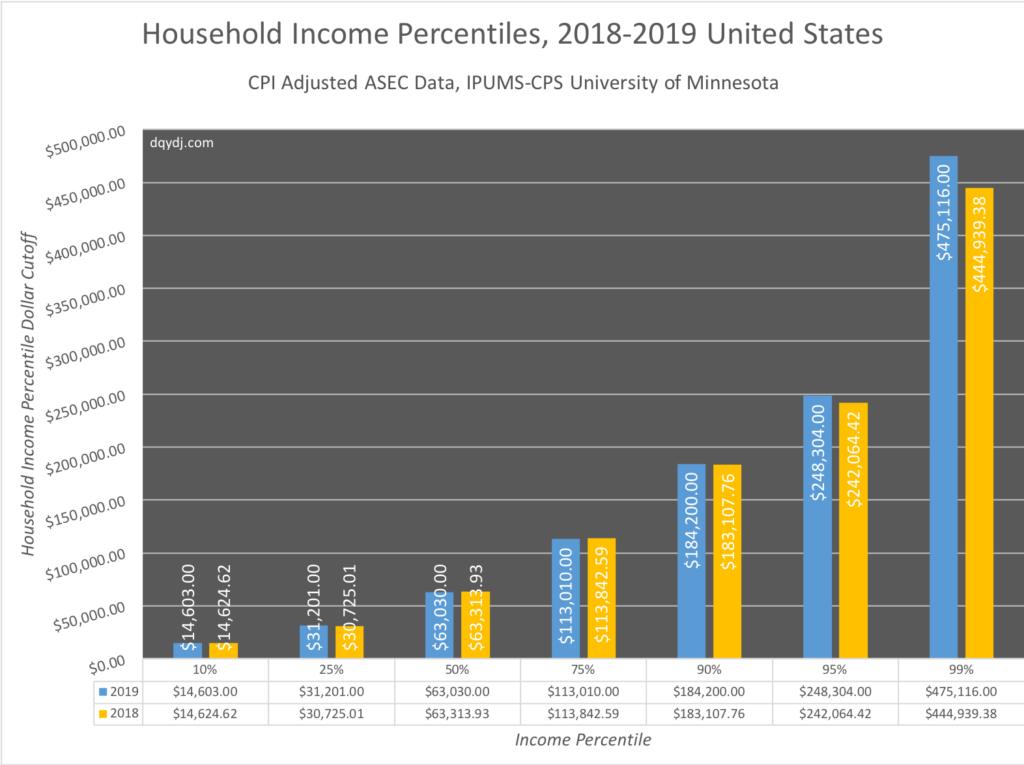

As you can see, the analysis shows incomes reduced across the board (“Conventional, 2021”), though marginally for lower earners. The lion’s share is borne by those in the top 1%. As you can see below, income of $475,000 or more gets you in the top 1%:

The American Enterprise Institute and The Tax Foundation estimate Mr. Biden’s proposal would generate roughly $3.8T in additional taxes from 2021-2030. Over 1/3rd is projected to come through higher corporate income tax rates as his proposal moves them from 21% to 28%.

There is no meaningful impact, positive or negative, on the national debt.

There are other proposals that I won’t address because they are light on details, but they include an $8,000 tax credit for childcare, closing off loopholes pertaining to the real estate industry, sanctions on “tax havens”, and greater premium tax credits for the Affordable Care Act, among other things.

Obviously, this is just a proposal and a few significant things need to happen before it becomes law, the first being Mr. Biden winning in November. If he does, he would also need Democrats to pick up enough seats in the Senate for a majority as it’s unlikely Republicans would agree to his plan.

Regardless of the outcome of November’s election, Mr. Biden’s proposal re-emphasizes the importance of tax planning. A pillar of Beacon Wealthcare’s investment philosophy is tax-efficiency and we accomplish this by selecting investments that have relatively little taxable activity, placing rebalancing trades in tax-deferred accounts whenever possible, capturing losses and gains (yes, there are times where it’s beneficial to accelerate income) at optimal times, and through asset location. We also strive to have a deep understanding of your tax return and a solid line of communication with your CPA. As tax laws change, your plan will adapt.

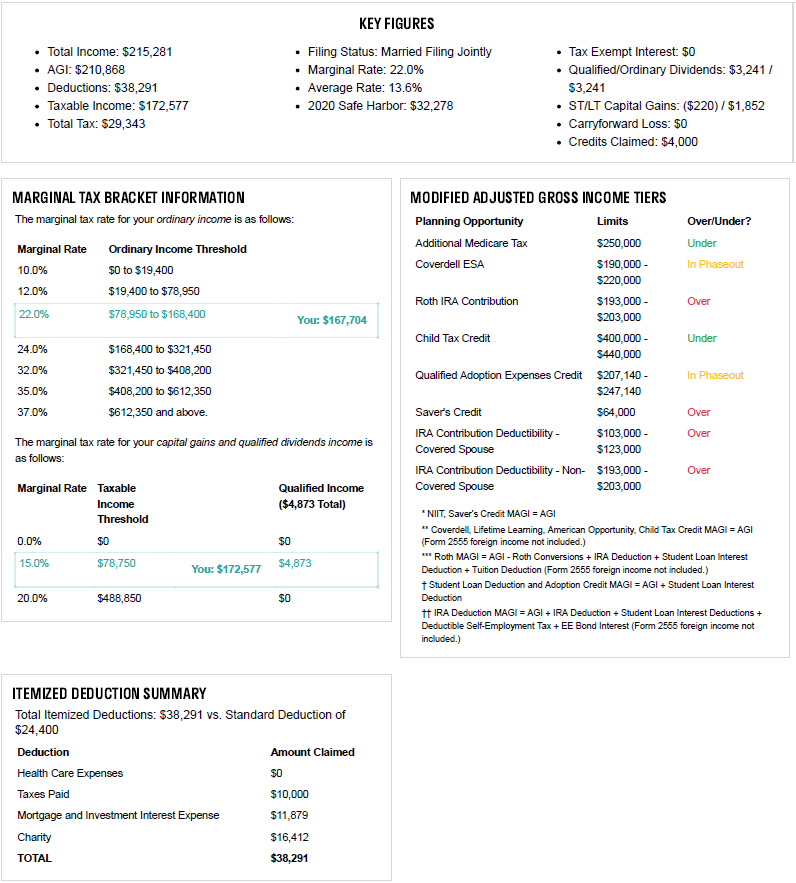

To ensure this, we recently added some transformative technology that will increase our efficiency as well as the level of understanding we have of your tax situation. Within minutes, we can upload a tax return and have a report generated that looks like this:

All these numbers may or may not mean something to you, but to us, they are gold, allowing us to provide better, more holistic financial planning advice to each of you. As our clients have been providing us with their tax returns over the past few weeks, we have been creating these reports and getting in touch if there are any immediate items to address. If there is nothing urgent, as we start working through our year-end planning checking in a few short months we will revisit your report to see if there are any planning opportunities to address. If you would like to see a copy of your report, please let us know.

In closing, you can be confident that no matter the tax landscape, whether expectations are rates will rise or fall, the importance to us of tax planning never changes.

As always, thank you for reading and let me know if you have any questions.

Have a great weekend!