25 Sep 2020 Taxes and Thinking Long-Term

A few weeks back I wrote an explainer of Joe Biden’s tax proposal and received some questions about the following passage: “(Y)es, there are times where it’s beneficial to accelerate income.” It’s a counter-intuitive statement because most of the conversation around taxes is that you want to pay as little as legally possible year-in-and-year-out. This isn’t to ignore the debate around whether income tax rates are too high or too low. It’s just that the natural bent for most people is to pay the least amount of taxes that the government allows with very little thought to the future.

Yet, that’s not always the best route. There are scenarios where it is beneficial to choose to pay more in taxes. To illustrate, let’s use the example of a couple on the verge of retirement, though we could just as easily use a couple in their mid-50’s at the peak of their earnings power or a business owner anticipating a few bad years.

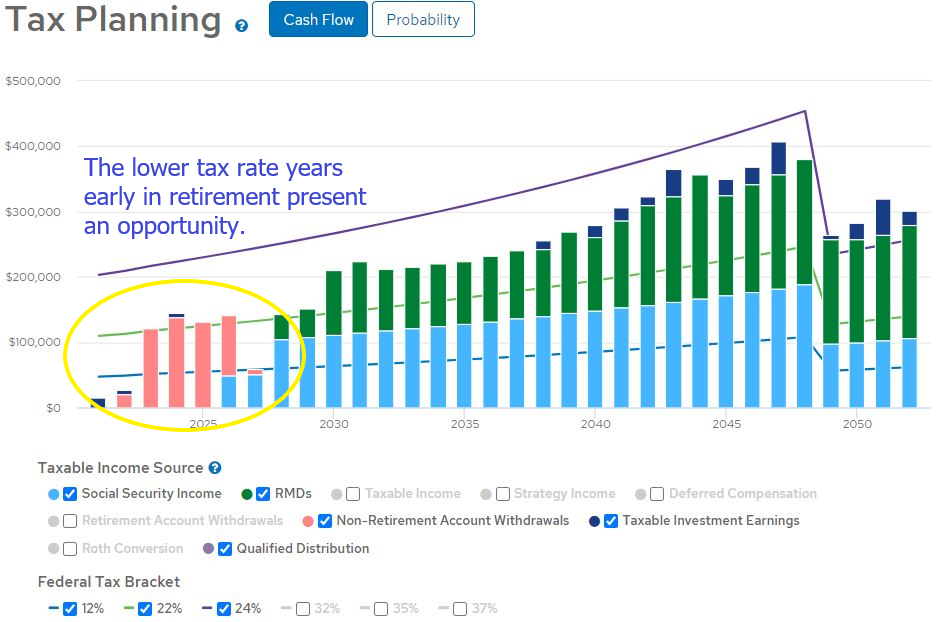

The chart below shows projected income and tax brackets for a couple throughout their retirement. The most important thing to notice is that after the first six or seven years of retirement there’s very little flexibility with taxable income as Social Security, in blue, and Required Minimum Distributions, in green, kick in. Whether or not all that income is required to meet spending, taxes are being paid on it. It’s also important to notice how the couple’s federal income tax bracket increases as a result: they are in the 12% bracket (light blue line sloping upward left to right) in the early years yet well into the 22% bracket (green line) in later years. Finally, as I’ve circled on the chart, the lower income tax brackets in the early years present a tax planning opportunity.

The strategy is to realize additional income in the earlier years when only 12% in Federal taxes is paid to reduce the amount of income that in later years would be subject to 22% Federal taxes. How that is done depends on a client’s needs and goals. The additional income could be in the form of a Roth Conversion if it isn’t needed to meet expenses, for example, or using pre-tax retirement accounts rather than after-tax brokerage accounts if it is.

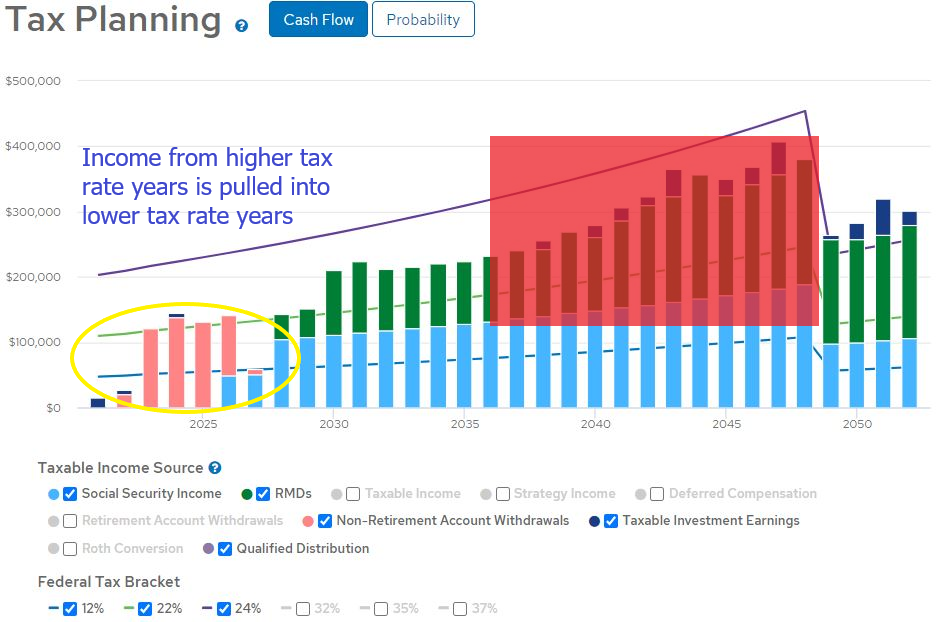

The chart below assumes the former strategy: that pre-tax accounts are used early in retirement to meet living expenses. This increases the amount of income subject to 12% Federal tax and reduces that amount later on subject to 22%. Spending doesn’t change. Goals aren’t negatively impacted. The overall impact, though, is that less wealth is lost to Federal income taxes.

.

While I’ve made some smaller points, the main point is that tax decisions need to be made with the long-term in mind. Far too often decisions around taxes are made using the mindset, “How do I get my tax bill as low as possible this year?” Yet, by doing that, you’re only delaying the tax bill, pushing it off into the future. Do that too much or without any long-term plan and you create a situation, usually in retirement and right around the time Social Security and Required Minimum Distributions begin, where you have no flexibility and, not only is your Federal tax rate higher than it otherwise could be, but your Social Security taxes and Medicare premiums could also be higher.

This isn’t to say that tax planning is some magical panacea. It’s not. Tax rates can change, goals change, circumstances change. Taxes are a way of life, one of only two certainties, according to Benjamin Franklin. But, with proper planning, long-term thinking, and collaboration between your financial advisor and tax professional, less of your wealth can be lost to taxes.

As always, if you have questions, give me a call or schedule a time to chat.

All information contained herein is for illustrative purposes and should not be construed as tax advice. Please consult your tax professional and financial advisor before undertaking any of the strategies discussed.