27 May 2021 Real Estate is Hot. Has Our Home Been a Good Investment?

It’s not breaking news to say the U.S. housing market is on fire. From April, 2020, to April, 2021, median home prices increased by 17.2%. There are myriad reasons for this: lack of supply (the roots of which can be traced all the way back to the Financial Crisis), urban flight/remote work (exacerbated by COVID-19), and fiscal stimulus (the Fed has introduced $3T+ dollars into the financial system in the last 12 months), to name a few. While builders are doing their best to meet demand, the fact that no one is building starter homes only pushes prices higher and higher.

A 17.2% year-over-year increase is incredible, and it’s not like the previous years were lackluster: According to the Federal Reserve, home prices across the U.S. increased by 73% during the 10 years ending February, 2021.

Closer to home, real estate in the Triangle is hot, think, surface-of-the-sun hot. Within the last month, a client of ours listed their home for around $850,000 and on the first day had more than half-a-dozen offers before accepting one at ~$950,000 with a $100,000 contingency and no inspection required. HOT.

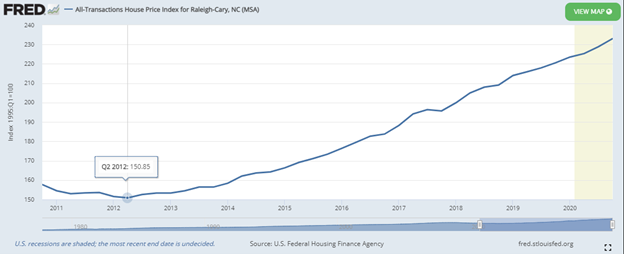

While the Federal Reserve hasn’t updated numbers for Raleigh since October, 2020, appreciation over the preceding 10 years was about 48%, as you can see below. While lower than what the U.S. has seen in aggregate, much of that is due to how well insulated the Triangle was during the Financial Crisis; it didn’t have as great of a crash to recover from.

You’ll notice the low point of the last decade was Q2, 2012, which, coincidentally, is when Emily and I purchased our home. It was a different market back then: the house had been on the market for a few months, we paid $10K below list price, and were able to push back against the seller’s request for no inspection. You can see original pictures of Jack’s bedroom and the master bathroom below, providing all the reasons you need for why it sat on the market so long!

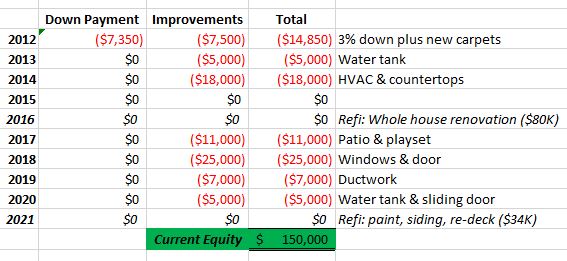

Given a real estate market that’s ablaze, I’m curious to see how much Emily and I have benefited. To that end, here are our out-of-pocket costs over the last ~9 years*:

Total spending: $85,850. You’ll notice that we did a major renovation in 2016 and are working on additional improvements this year, but I haven’t input a cost. The reason: we tapped the equity in our home in both instances. In 2016, the total was $80,000. This year we pulled $34,000. Rather than showing that as an out-of-pocket cost, it’s accounted for by looking at the difference between the value of our home and the debt on our home, i.e. the equity.

All that said, here’s our annual rate of return: 9.1%, which, if I’m being honest, is much higher than expected.

Here are a few of my takeaways:

First, leverage, i.e., buying an asset using debt, is the reason real estate can offer such attractive returns. Proof: Emily and I put $7,350 down, mixed in some sweat equity by painting the entire inside of the house ourselves, added $30,000 in improvements, and five years later had roughly $120,000 in equity. That’s 45% annual returns! Emily and I bought a neglected, dated house with good bones in a wonderful neighborhood at the low point of the last 10 years. It was the perfect situation and we’ll probably never see returns like this again. Yet, purchasing an asset with debt can also go against you. If the market hadn’t cooperated, we could have been “upside down” in a heartbeat.

Second, improvements can add value, to a point. Again, after five years we had $120,000 of equity. About 5 years later, we have $150,000, or $30,000 more. Yet, we’ve spent considerably more to improve the house over the last five years than we did during the first five years: Our annual rate of return from 2016 until now is -12%. The easy money was made the first few years because the house was in such bad shape.

Third, spending money on your home is emotional. While the spending of the last five years hasn’t offered the same returns as the first five years, I’ve enjoyed the fruits of the former much, much more than the latter. Prior to the renovation we had a dining room we never used, a master bathroom that was inferior to the one in my college dormitory, and an unfinished third floor. Now, we have a functional, warm, welcoming home that can easily accommodate guests.

Fourth, and finally, the costs associated with selling our home (any home) and moving are substantial. Paying 6% in realtor fees plus, let’s say, $10,000 to move, cuts our annual rate of return from 9.1% to 4.05%. We’d potentially surrender half our annual returns by moving.

This has been a fun exercise because it took me back to when Emily and I bought our first house, the rough shape it was in, and the work we did to make it our home. It’s also been fun in showing the work we did paid off, but it doesn’t change my opinion that where you live is never an investment. We didn’t buy our home on Basil Drive for the potential returns. We bought it because we wanted to be close to friends, part of a neighborhood, and to have stability. That it’s turned into a good investment is icing on the cake.

As you consider the purchase of a home, whether it’s a second, third, or first, do your best to keep the same perspective. Make sure it fits comfortably into your budget. Find a good neighborhood. Be mindful of renovations. A home is the largest single transaction you’ll make in your life, so you want to make it a good one.

We can help with that. Click here to schedule a call.

*I intentionally excluded our mortgage payment because we have to live somewhere and our monthly payment, including escrow, has hovered around $1,800 and is close to what we’d pay in rent.