28 Jul 2022 It’s Been a Year (Checking In On Mr. Lynch)

Almost exactly a year ago, I wrote a brief about the Morgan Stanley Inception Fund, Wall Street Journal’s top mutual fund for the one-year period ending June 30th, 2021 (you can read the brief here). In summary, the Inception Fund, managed by Dennis Lynch, was up 150% in 2020, besting its peers by nearly 112%. In addition to praise from the Journal, the fund was rewarded with more than $1B from investors as its overall size swelled from $260M to more than $2.2B (new money + appreciation) in less than 13 months. Using the Inception Fund as an illustration, I provided three reasons this is exactly the type of investment to avoid:

-

- One year performance is meaningless;

- Being a successful active investor year-over-year is really, really hard;

- A top-performing fund attracts a lot of new money, making excess performance more difficult to achieve.

Anyway, nerd that I am, I politely asked Siri to remind me in one year to check in on the fund (I’m sure many of you did the same). Reliable aide that she is, she did. So I checked.

It’s not good. In fact, it’s much worse than I expected it would be.

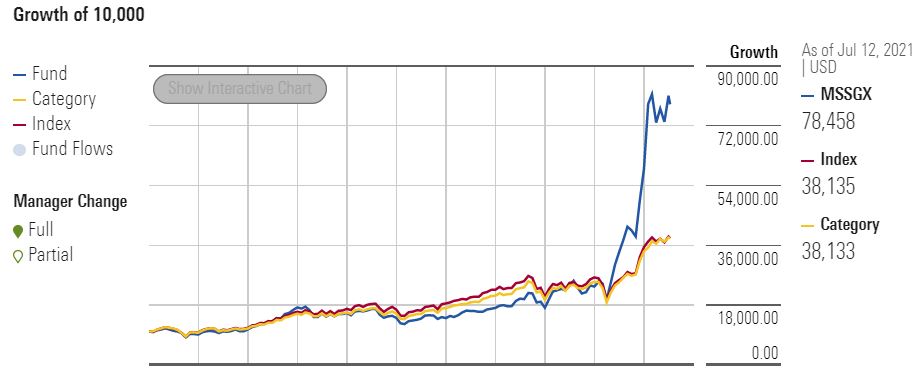

As a reminder, here’s how the fund’s performance looked through July 12th, 2021:

The blue line is the Inception Fund, the yellow line is the category average, and the red line is the index it tracks.

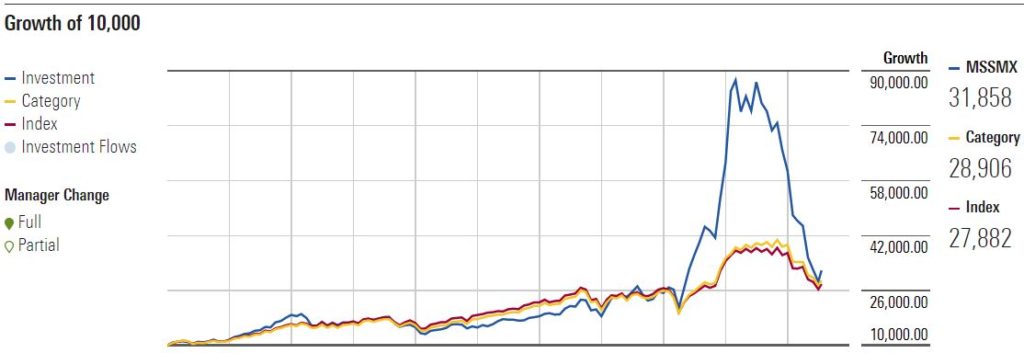

Here’s how the chart looks now:

And here is how the fund has done since my brief was published (7/12/2021-7/20/2022):

The S&P 500 (green) is down less than 10% over the last year while the Vanguard Small Cap Growth index (yellow), the ETF that tracks the Inception Fund’s benchmark, is down 27%. The Inception Fund has lost nearly 70%. At its peak, the fund had $2.2B of assets but now, due to depreciation and withdrawals, it has less than $525M.

As I said last year, this isn’t at all about Mr. Lynch or his fund; they just happen to serve as the best, most recent example of the challenges with active investment management and chasing performance. I could just as easily use the Ivy Asset Strategy fund, an investment I recommended to clients back in 2008-2009. The short story: In 2007, the S&P 500 was down around 2% while Asset Strategy was up nearly 40%. Young and inexperienced, I didn’t grasp the unique circumstances that contributed to its performance, or how the way in which it was invested was well-suited for a once-in-a-generation financial crisis, but not a normal stock market environment.

Which highlights another challenge with active investment management: How do you separate skill from luck? Does the manager of a fund that blows away the competition for a year or two possess real skill, or was he or she just lucky? If the financial crisis hadn’t happened, would I have ever heard of the Asset Strategy fund? It’s net negative since 2008, so probably not. The same goes for a fund like Inception: if a global pandemic hadn’t forced all of us to stay home for months on end, would it have earned the stellar returns it did in 2020?

At the beginning, I gave three reasons to avoid investments like this, and you should know they aren’t original thoughts. They are backed up with research, lots of it. Yet, we all need periodical reminders of the attributes that drive investment performance: fees, taxes, broad diversification, and our behavior. They may not win you praise from the Journal, but, well, look what that did for Mr. Lynch.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.