15 Jul 2021 Will Mr. Lynch Become a Victim of His Own Success?

In last week’s brief, Jared opened with this quote from Howard Marks: “By being in the top half for 14 years, he was in the top decile for the whole period. And I thought that was a great realization.”

Jared went on to say, “You don’t need to outperform the market. Ever. By taking what the market gives you for basically free, and by doing so for as long as you can, you will naturally outperform the overwhelming majority of investors who think they need to make bold tactical decisions in order to be successful investors.”

Which brings me to Dennis Lynch.

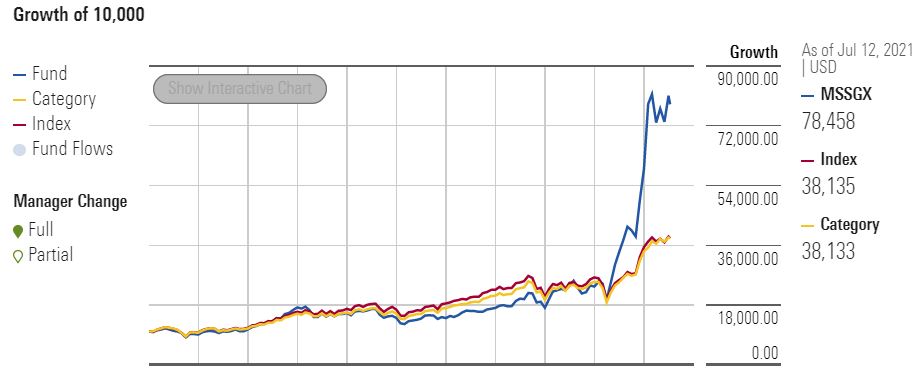

Mr. Lynch runs the Morgan Stanley Inception Portfolio (MSSGX) which was, until the past few months, a small, relatively unknown mutual fund. Until, that is, it returned 150% in 2020 and was labeled the “Top Mutual Fund” for the 12 months ending June 30th, 2021 by none other than the Wall Street Journal. The returns he posted in 2020 beat the category average by a whopping 111.95%, as you can see below.

It’s impossible to read the preceding paragraph or look at the chart above and not think to yourself, “I want returns like that! Gimme those!”

Yet, this fund is a perfect example of why we believe it is in your best interest to not seek out these kinds of returns. Here are three reasons why.

Before I start, let me say this isn’t about Mr. Lynch or the Inception Fund, specifically. It’s just their recent success is a perfect example of why active management is so challenging, generally.

First, while Mr. Lynch’s recent returns are inarguably stellar, his long-term numbers tell a different story. The graphic below, taken from Morningstar, shows you calendar year returns for the Inception Fund along with comparisons to its category and its index. The 2020 numbers immediately jump out: his average annual return going back to 2011 is an impressive 26.04%. The average for the index is 14.649%. That’s an extra 11.5% per year!

Yet, the numbers are skewed by 2020. If you take the average annual return from 2011-2019, omitting 2020, the index actually beats the Inception Fund: 12.43% vs. 12.21%, respectively. Prior to 2020 this fund was adding no value, as you can see by the numbers just above, and more clearly by looking again at the chart at the top of the page. Sadly, many investors won’t dig much deeper than 2020 before making the decision to invest in his fund.

Which brings me to my second point: It is really hard to be a successful active investor year-over-year. Here are two pieces of evidence to back this up.

The first is from the fund’s own track record. The chart below shows the Inception Fund’s Quartile Rank, again taken from Morningstar. Going left to right, 2011 is the first year, year-to-date 2021 is last. As you can see, the performance against its peers is all over the map. In fact, there was a three year stretch from 2015-2017 when the Inception Fund was one of the very worst in its category. As an investor, which set of returns might you get? The ones that put you at the top or the bottom of the heap? And if you start at the bottom, are you willing to stick it out in hopes of climbing back to the top?

![]()

The second piece of evidence is referred to as the Persistence of Returns. That is, can we rely on past performance to predict future performance? According to a research paper from Mark Carhart, no. While prior year returns have some impact on the next year (and this is mostly due to momentum rather than skill, the author finds), there’s no long-term correlation between past performance and future performance.

Third, it is worth watching if Mr. Lynch will become a victim of his own success, as have many managers who have come before him. In my humble opinion, what follows is the biggest challenge he faces.

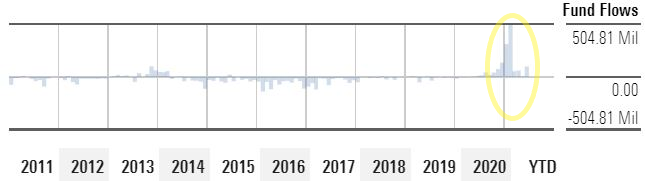

Considering all the praise Mr. Lynch is receiving, it’s not surprising investors are handing him their money. What is surprising is the amount he’s raised and the speed with which it’s happened.

Looking at the June 30th, 2020 semi-annual report from Morgan Stanley, total net assets for the Inception Fund were $260M. Six months later, in their annual report dated December 31, 2020, they list total net assets as $863M. A portion came from appreciation, but $411M was new money.

As if that jump wasn’t enough, as of July 13th, 2021, Mr. Lynch’s fund has more than $2.2B invested in it. As you can see below, in January and February of this year alone, more than $700M in new money poured into the fund.

From $260M to $2.2B in just over a year.

That may sound like a blessing (I’d take that increase in my net worth!) but for a mutual fund manager it’s a real headache. Especially for one whose objective is to find small, growth-oriented investments, as Mr. Lynch’s is. A year ago, the Inception Fund was a small boat in a big ocean, able to stop on a dime and change direction at will. Now, it’s the Evergreen navigating the Suez Canal.

How can we tell? Because he’s holding over $300M in cash; 15% of the portfolio is uninvested. In his defense, you can’t hand someone more than $1B in new money in 13 months and expect them to have that many other ideas worthy of an investment.

As I said, this isn’t about the Inception Fund or Mr. Lynch, specifically. It is, however, about the challenges of seeking out great performance. Or, worse, finding great past performance and expecting it to continue. The odds are not in your favor.

For our clients, and with our own investments, we take what the market gives us “for basically free”, as tax-efficiently as possible, for as long as possible, knowing these factors increase the likelihood of outperforming the majority of investors. It’s the great realization all the advisors at Beacon Wealthcare have had, and it’s one we enjoy sharing with our clients.

Interested in learning more? Click here to schedule a call.