12 Jan 2023 How SECURE Act 2.0 Impacts IRAs, 401(k)s, 529s, and RMDs

As 2022 came to a close, Congress passed a spending bill that included a retirement bill commonly referred to as “SECURE Act 2.0.” Its predecessor, 1.0, passed at the tail-end of 2019 and lifted the starting age for Required Minimum Distributions (RMDs) from 70 to 72, while also doing away with the inherited IRA distribution strategy known as the “stretch IRA” for non-spouse beneficiaries, among other things.

By any measure, 2.0 is huge, containing a plethora of changes that will impact both broad swaths and narrow niches of the American public. Today’s brief will focus on the former, of which there are three, and will summarize a few, though not nearly all, of the others.

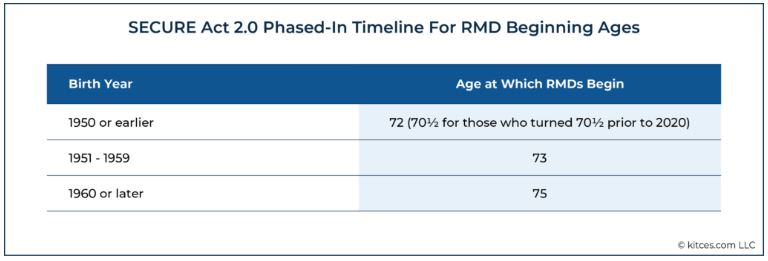

RMD Start Age Changed to 73, then 75

The change that will have the broadest impact has to do with Required Minimum Distributions for pre-tax retirement accounts. As mentioned above, 1.0 pushed the RMD age from 70 to 72, and 2.0 pushes it back further. The age at which you need to start taking distributions now depends on the year you were born:

If you turn 72 this year and, under 1.0, were scheduled to start RMDs, you now aren’t required to take your first distribution until you are 73.

It’s also worth pointing out that the penalty for missing your RMD is reduced from 50% of the amount you failed to withdraw to 25%, with an additional reduction to 10% if the error is corrected in a timely manner.

Pushing the RMD age back presents a planning opportunity by allowing more years of voluntary withdrawals. A strategy that we explore with our clients and their CPAs is estimating potential future tax brackets and comparing them to their current bracket. If the current bracket is lower the future projected bracket, it may make sense to take a voluntary withdrawal from the pre-tax retirement account, resulting in tax savings. (I wrote about this a little more than a year ago.)

Catch-Up Contributions

For most, turning 50 provides little reason to rejoice. However, the IRS, for all their faults, does their best to alleviate the pain (literal and figurative) of aging by allowing you to contribute more to your retirement account beginning in the year you turn 50.

The IRA catch-up contribution, stuck at $1,000 since 2006, is now indexed to inflation and will grow in $100 increments. This goes into effect in 2024.

For employer retirement plans, (think 401(k), 403(b)) there are multiple changes.

First, beginning in 2024, any employee “whose wages (as defined in section 3121(a)) for the preceding calendar year from the employer sponsoring the plan exceed $145,000,” (adjusted for inflation) can only make Roth catch-up contributions. That’s right: no more pre-tax catch-up contributions for high earners. In fact, if the employer’s 401(k) plan does not allow Roth contributions (there are still a few out there), then no employee is allowed to make a catch-up contribution.

Second, beginning in 2025, the IRS will allow additional catch-up contributions for eligible participants ages 60, 61, 62, and 63. To quote Jeffrey Levine of Kitces.com, “The language of the provision is a bit wonky.” I’ll spare you the language and the math it spells out, but the catch-up for the 60-63 age group, were it to go into effect this year, would be $11,250, rather than $7,500 for those 50-59, and 64+. The same rules about high wage earners apply: if you earn more than $145,000, inflation-adjusted, your contributions will be Roth.

You might wonder, based on the former change, if catch-up contributions are still worthwhile. The short answer is yes, if the alternative is investing an equivalent amount in a brokerage account.

It’s worth noting that forced Roth catch-up contributions for high earners doesn’t, as of now, apply to self-employed individuals, or for those switching jobs mid-year. To the former, because their previous year wages often aren’t known until months into the current year, and to the latter, because the language of the law looks at the wages paid by the current employer for the previous year. If you start a new job in May, you have no “previous year” earnings with that employer, so pre-tax catch-up contributions would be allowed.

Limited 529-to-Roth IRA Transfers

While the preceding two changes will impact more people, the 529-to-Roth IRA Transfer rule is getting the most ink. Here’s how it works.

Funds may be transferred tax-and-penalty-free from a 529 account to a Roth IRA, provided the following criteria is met:

-

- The 529 account must have been open for a minimum of 15 years;

- Contributions, plus earnings associated with them, made within the last 5 years cannot be transferred;

- Funds must go into a Roth IRA in the name of the 529 account beneficiary;

- The beneficiary must have earned income in the year of the transfer;

- Transfers cannot exceed the annual contribution limit ($6,500 in 2023), less any normal Roth or Traditional IRA contributions;

- There is a lifetime cap of $35,000 per beneficiary (more on this below);

- There is no income limit restricting transfers, as there are with Roth IRA contributions.

With regard to the “per beneficiary” lifetime cap, the natural next question is: If you change the beneficiary, does it re-start the 15 year clock? That is, what if my daughter, Gwen, graduates college and, by stroke of luck, me and Emily still have $105,000 in her 529 account (unlikely!). Could we, over a period of years, move $35,000 to Gwen’s Roth IRA, then change the beneficiary to me, transfer $35,000 to my Roth, change the beneficiary (again) to Emily, and transfer the remaining $35,000 to her Roth? Or would we need to wait 15 years every time the beneficiary changes?

While the IRS will need to clarify, Jeffrey Levine, who I mentioned earlier, believes it will not start a new 15-year clock.

Many parents hesitate to fund 529s out of concern their child will not attend college. Hopefully, this rule change will help alleviate their worries.

A Brief Summary of Other Changes

-

- Roth contributions to SEP and SIMPLE IRAs can now be made;

- Employer matching contributions can now be Roth, which would add the contribution to the employee’s taxable income;

- Student loan payments made by employees can receive 401(k) matching contributions (2024);

- With respect to an inherited IRA from a deceased spouse, the surviving spouse can elect to be treated as the deceased spouse. In practice, this only provides a benefit where the deceased spouse was younger, and by calculating RMDs using the uniform lifetime table versus the single lifetime table.

- Qualified Charitable Distributions (QCDs) can be used to fund certain charitable trusts, with restrictions.

- A multitude of new rules around hardship withdrawals from retirement accounts.

Surprisingly, the back-door Roth IRA strategy was not eliminated.

The SECURE Act 2.0 will have an impact on all of us, and its complexity highlights the need for expert help, not only to ensure you don’t run afoul of the rules, but to allow you to receive the greatest benefit from the rule changes that affect you.

In the coming weeks and months, we will be reaching out to our clients to discuss how 2.0 impacts them, and what, if any, proactive steps can be taken to make the most of the rule changes.

As always, please reach out to us with questions, or schedule time with one of our advisors by clicking here, then going to the bio of the advisor you’d like to speak with.

The content above is for informational and educational purposes only. The links are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.