07 Sep 2023 The IRS On Its Heels

Since 2010, there have been no fewer than five significant changes to the tax code. It began with the passing of the Affordable Care Act, which added a 0.9% Medicare tax on earnings above a certain threshold plus a 3.8% Net Investment Income Tax (NIIT) on qualifying investment activity. Two years later, President Obama passed the American Taxpayer Relief Act, which reinstated the Pease Act, phasing out certain exemptions and itemized deductions for taxpayers with incomes above a certain amount, while also increasing the top personal income tax bracket as well as the highest rate paid on long-term capital gains. Six years later, President Trump passed the Tax Cut and Jobs Act which lowered most income tax rates, increased the standard deduction, capped the deductibility of state and local income taxes (often referred to as “SALT”), eliminated the aforementioned Pease Act, increased child tax credits, and, by various means, significantly reduced the impact of the Alternative Minimum Tax (AMT).

As if that weren’t enough, the SECURE Act of 2020 pushed back the age when Required Minimum Distributions (RMDs) start from 70 1/2 to 72, changed inherited IRA distribution rules, and provided small businesses a tax credit for starting a retirement plan. Finally, SECURE Act 2.0 was passed at the tail-end of 2022. We wrote about this earlier this year, noting its enormity. Changes include how 529 funds can be used, another change to RMD age, plus limits on who can make pre-tax catch-up contributions to 401(k) accounts.

All these changes have left the IRS on its heels, as evidenced by two noteworthy announcements this year.

Announcement #1: No Post-2019 Inherited IRA RMD Penalties in 2023

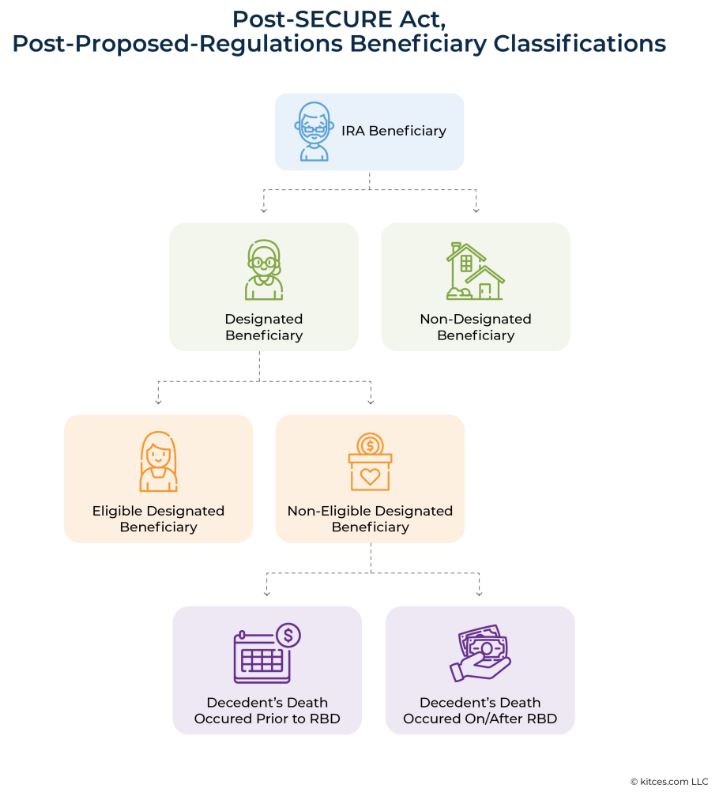

The first announcement by the IRS attempted to remove the confusion around which beneficiaries need to take an RMD from an inherited IRA in the year 2023. As noted above, the SECURE Act of 2020 said that rather than a “non-eligible designated beneficiary” taking distributions over the course of their lifetime, the inherited IRA needed to be fully depleted over 10 years. The IRS left open to interpretation whether that meant annual distributions were required in years 1-9, or if the account could be depleted over the beneficiary’s preferred timeline, as long as it was 10 years or less. They attempted to clear this up in early 2022 by saying it depended on two criteria: whether or not the beneficiary was “eligible” or “non-eligible”, and whether the original account owner had started their required minimum distributions. Here’s a chart from Michael Kitces that might help:

To make it even more confusing, all of this applies only to those who inherited an IRA after December 31st, 2019.

Of course, everyone was left sufficiently confused. So much so that the IRS announced in July of this year that if a 2023 distribution was required but not taken, no penalties would be assessed.

Announcement #2: A Delay in Forced Roth Catch-Up Contributions

SECURE Act 2.0 mandated that “highly compensated employees,” defined as anyone making more than $145,000 in 2023, eligible to make 401(k) catch-up contributions could no longer make those on a pre-tax basis. Rather, they would be post-tax, or Roth, contributions. Not all 401(k) plans offer Roth contributions so in those instances the IRS said no employee would be eligible for a catch-up contribution, pre-tax or otherwise. This law was scheduled to go into effect in 2024. Of course, such a change impacts many parties: retirement plan custodians, third-party administrators, employers, not to mention the individuals making the contributions.

Facing significant pushback, the IRS announced a two-year delay to this rule, giving all parties until 2026 before it goes into effect. This means highly compensated employees can make any kind of catch-up contributions they choose until the year 2026.

What It All Means

First, the rules around who does or does not need to take an RMD this year, and in future years, remains needlessly confusing. Prior to the original SECURE Act it only mattered whether the person inheriting the IRA was the original owner’s spouse. Now there are “eligible” and “non-eligible” beneficiaries, and needing to know if the original owner had started RMDs. Plus, unlike regular RMDs where the custodian will calculate the amount that is required to be distributed, no such help is giving to inherited IRA owners; you need to do the math yourself.

Second, while distributions this year aren’t required, it may still be in your best interest to take one. Making that determination involves consulting with your financial advisor and tax professional.

Third, beginning in 2026, if you are forced to make Roth 401(k) catch-up contributions when previously you were making pre-tax contributions, nine-times-out-of-ten you will be better off than if you put the same amount in a brokerage account. Everyone’s situation is different so make this decision with your full financial picture in mind.

Lastly, alterations to the tax code have been commonplace over the last 10-15 years and the pace of change shows no sign of letting up. The IRS, already facing a huge backlog of returns and working through them with technology that’s older than me, is struggling to keep up. Laws are passed without a full understanding of what it takes to implement them or with such opacity that they create more confusion than clarity. (See: 529-to-Roth 15-year rule.) As tax law changes come up and as their implementation is delayed, we’ll keep you informed about how they affect you and, in partnership with your tax professional, suggest ideas to help keep your financial life as tax-efficient as possible.

The content above is for informational and educational purposes only. Any links are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.