18 May 2023 The Debt Ceiling

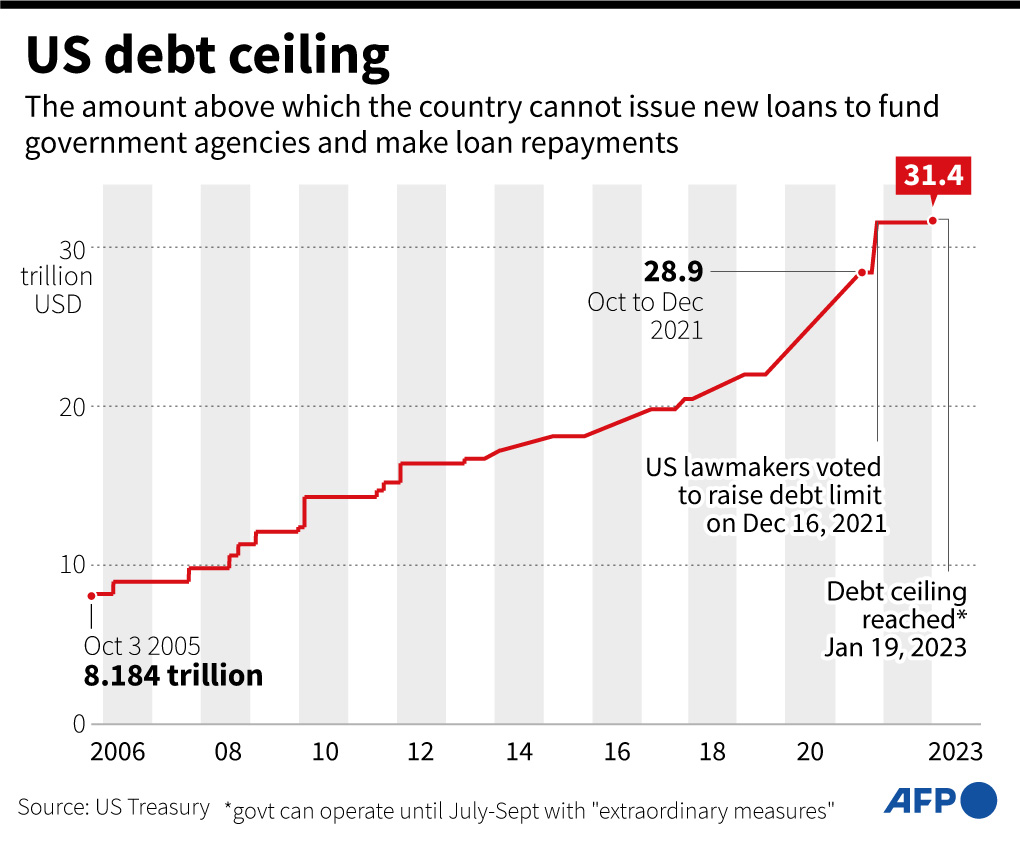

The current Debt Ceiling debate first became a thing as far back as last November when Republicans took control of the House. With a divided congress and the U.S. running its usual budget deficit, agreement would be needed within the legislative branch to raise the borrowing limit. As we all know, unity of thought between parties seems anathema to both Democrats and Republicans, which brings us to where we are today, at Debt Ceiling’s doorstep.

Let’s start with good news. Earlier this month, Ralph Axel, an interest rate strategist with Bank of America, had this to say: “What you are seeing is a consensus view that we will not cross through the X-date. At the moment that remains a low probability event that is hard to price.” Moody’s Analytics says the likelihood of an agreement being reached is 90%, and the S&P 500, up 7% through May 16th, certainly isn’t behaving as though the government is about to reach the end of their ability to borrow. Add in the fact that congress has never failed to reach an agreement and most signs point to resolution.

The bad news, as already mentioned, is that the relationship between our two parties seems as antagonistic as ever and it remains to be seen how much arm twisting each will do before one cries uncle.

Ultimately, as the Brookings Institution says, the impact of a failure to reach an agreement is largely unknown: “The economic costs of the debt limit binding, while assuredly negative, are enormously uncertain. Assuming interest and principal is paid on time, the very short-term effects largely depend on the expectations of financial market participants, businesses, and households.”

Because the U.S. has never defaulted, there is no historical comparison we can make. It may be helpful to look back to 2011, however, when we had a similar standoff. While an agreement was reached with two days to spare, the stink of the negotiations led Standard & Poor’s to cut the credit rating of the U.S. for the first time in history. (This was not without controversy, as Standard & Poor’s made a spreadsheet error that overstated federal debt by $2T.)

The reaction by investors was mixed:

Monday, August 8th, 2011, the first trading day after the downgrade, the S&P 500 (blue line) dropped 6.6%. But two short months later, it had recovered its losses and a year later was up more than 7%. Treasuries, represented by the 7-10 Year Treasury ETF (yellow line), were up 1% on the 8th and a year later had appreciated nearly 10%. The former was expected, the latter was unexpected, showing us yet again that it’s really difficult to nail both the prediction and the response.

All this said, as we get closer to the “X-date” (June 1), how should we prepare? Here are our thoughts:

Be diversified. If the U.S. defaults, there may be volatility across all asset classes—including bonds and stocks—so it will be important to be diversified. If we knew in advance what the impact of a default would be on each, then theoretically we could concentrates bets on one asset class, but, as mentioned above, we can’t know in advance. For example, U.S. Treasuries are a debt obligation that would technically be in default: on the one hand that could lead prices of those Treasuries down, but on the other hand, the default is completely a made-up event which would be resolved, and Treasuries continue to be one of the safest assets in the world. In the volatility induced by a default, there could be a “flight to quality” which would actually drive Treasury prices up. You can build these opposing viewpoints for any asset class, and therefore the importance of diversification across them is paramount.

Be liquid. If you rely on your portfolio for income, have a healthy amount of cash on hand that you can tap into without having to sell more volatile assets like stocks and bonds. The only way to make the possible consequences of a default worse would be the forced sale of stocks and/or bonds in order to raise cash to fund your lifestyle. As long as you can continue to hold volatile assets through the period of volatility, then you can avoid turning paper losses into real, economic losses. Our retired clients who live off their investments typically have 3-6 months of withdrawals in cash in their portfolio for this exact type of situation.

Be optimistic long-term while planning pessimistically in the short term. The two things above are essentially an approach to investing that has served well in every flavor of uncertainty that investors have experienced over the last 100+ years. Long-term optimism keeps our focus on time periods that far outlast even politically driven possibilities like this one, while short-term pessimistic planning makes sure we’re diversified and with sufficient cash to weather uncertainty.

Ultimately, while we are confident the Debt Ceiling will be raised before the deadline is reached, we understand this can be an unnerving time so please reach out to us if you want to discuss your plan.

The content above is for informational and educational purposes only. The links are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.