10 Jul 2025 Tax Free Social Security? Not Exactly.

As you have likely seen by now, the new tax bill (commonly called The One Big Beautiful Bill) has passed both chambers of Congress and been signed into law by the President. Ryan has previously touched on the draft bill here and here. A few items have changed since those preliminary plans, but a lot of the pieces have remained largely the same. One item that we wanted to touch on has received more coverage than others: the taxation of Social Security.

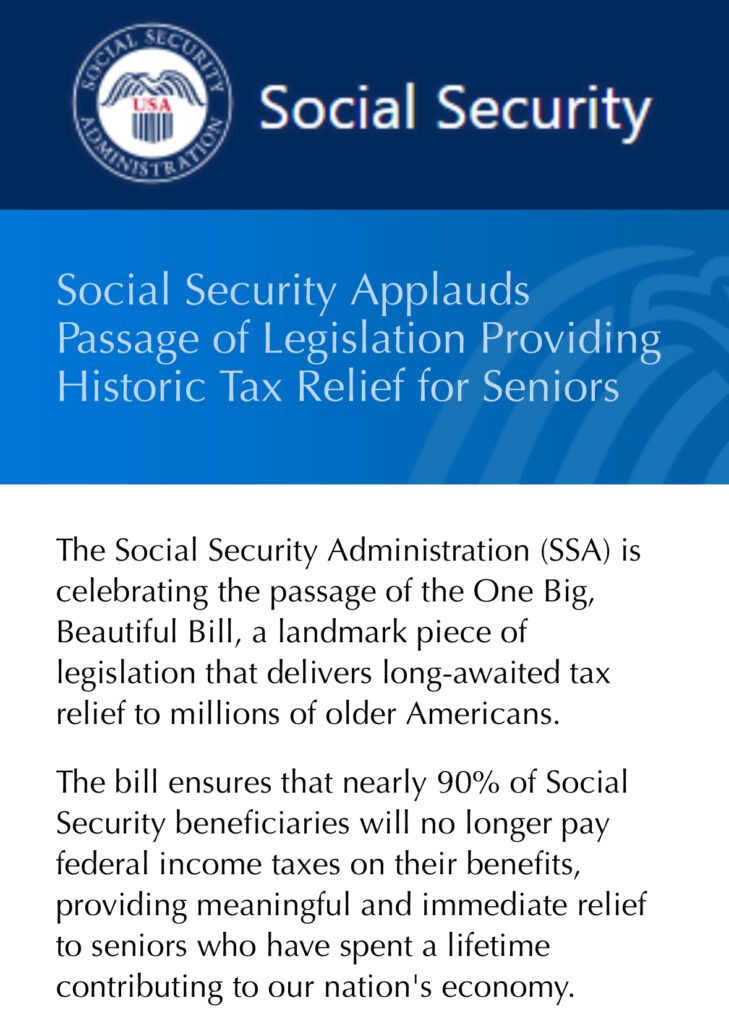

This was especially confusing for many people after the Social Security Administration sent this email after the bill was signed:

One may get the idea when they read that email that the taxation of Social Security has drastically changed based on the new tax bill. The line towards the bottom of the email, “the new law includes a provision that eliminates federal income taxes on Social Security benefits for most beneficiaries,” is especially perplexing.

What is the reality now for the taxation of Social Security income? Has the taxation around it drastically changed? Is Social Security income now tax free?

It would be helpful to know historically how Social Security income has been taxed when you go to file your taxes. Generally speaking, if you filed your taxes with income in the $25,000-44,000 range (depending on filing status), up to 50% of your benefit would be taxable. If your income was more in the $34,000-44,000+ range (again, depending on filing status) then up to 85% of a taxpayer’s benefit may be taxable.

Has the OBBB changed this taxation structure? No, the OBBB has not changed the existing taxation structure for Social Security in any way. While it is tempting to end the Brief there, we will dive into a piece of the legislation that is new.

The part of the legislation that is updated and conceivably impacts Social Security is a new enhanced standard deduction. If you are age 65 and older (by the end of the tax year), you will receive an additional $6,000 (single) / $12,000 (couple) towards your standard deduction. Notably you will receive this additional deduction even if you itemize. This begins phasing out at adjusted gross income of $75,000 (single) / $150,000 (couples) and is currently only available from 2025 through 2028.

With a new deduction for a number of Americans, here are a few planning considerations:

- Should I hold off on taking Social Security? We often talk about delaying taking Social Security as long as you can because of the increase in benefit. Since people under 65 do not receive this enhanced deduction, it could lead to one more reason to not take your Social Security early.

- Should I adjust income or IRA distributions? Since everyone age 65 and older will receive this additional deduction, it provides interesting opportunities to realize income. For example, it potentially provides an increased amount that you could convert from your Traditional IRA to Roth at a lower tax rate. There is no requirement to be on Social Security to receive the deduction, so if you are still employed you can receive the deduction and continue to delay your Social Security filing.

It is easy to get lost in the already confusing tax code. Adding more changes, especially ones that have differing windows of availability, will only add to the complexity. For the people that this will benefit, it is a great tax change that will result in less taxes owed when they file their taxes. We at Beacon are here to discuss considerations for your personal financial plan and work with your CPAs to determine the best strategies moving forward. Never hesitate to reach out and ask how your plan may be impacted.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.