29 Apr 2021 Subtractive Changes and Financial Peace

When I think about writing, I have two rules. The first came to me by way of my 8th grade teacher, Mrs. Vermeulen: Sometime in high school or maybe even college, long after she was my official teacher, she said, “Jared, the only difference between writers and non-writers is that writers write.” By which she meant that there’s no magic. There’s just the act of writing. And the second rule, which I used to think was a Mark Twain quote, but which I found out this week is actually from Blaise Pascal, is “I would have written a shorter letter, but I did not have the time.” By which he meant that for writers, deleting words is often as important as writing them.

A few weeks ago I came across this fascinating article summarizing an academic study entitled: “People systematically overlook subtractive changes.” The article is well-worth your time and easily digestible, but the basic gist of it is this: When attempting to solve a problem, humans are biased towards proposing solutions that involve adding rather than subtracting, even when the latter would lead to objectively more efficient and effective solutions.

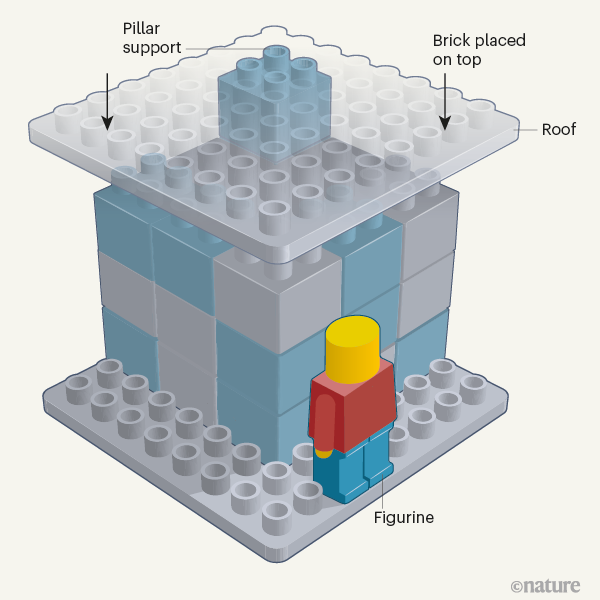

Figure 1 | Improving the stability of a Lego structure. ©nature

For example, “Consider the Lego structure depicted in Figure 1, in which a figurine is placed under a roof supported by a single pillar at one corner. How would you change this structure so that you could put a masonry brick on top of it without crushing the figurine, bearing in mind that each block added costs 10 cents? If you are like most participants in a study reported by Adams et al.1 in Nature, you would add pillars to better support the roof. But a simpler (and cheaper) solution would be to remove the existing pillar, and let the roof simply rest on the base. Across a series of similar experiments, the authors observe that people consistently consider changes that add components over those that subtract them — a tendency that has broad implications for everyday decision-making.“

In other words, we are remarkably like mediocre writers who keep trying to add better chapters rather than delete the bad ones.

Our financial lives are full of opportunities to create better, more efficient solutions by subtracting. The difficulty lies in the fact that entire industries, maybe our entire economic and social systems, are designed to engage only with “more is better” or, the slightly more subtle, “this new app/committee/policy/service is better.” We have forgotten that removing bad or underperforming or superfluous features may get us to a better place faster and more cheaply than designing something new or getting something more.

As we walk with clients through the various financial complexities that they face in the real world, here are a few “subtractive changes” that we frequently recommend:

- Reduce moving pieces. Often when new clients come on board, we spend the first several months working in this area, consolidating the number of accounts, consolidating where those accounts sit, reducing and integrating the investments within those accounts, and “deleting” unnecessary or outright detrimental insurance policies or other financial products.

- Reduce debt. Even in a period of extremely low interest rates like we’re currently in, we often work with clients to pay down debt faster than they “need” to. Any marginal benefit of leverage has a cost to it, even if that cost is one that mostly resides in our mental and emotional well-being.

- Reduce choices and decisions. This is mostly a process of automation. Automate recurring saving amounts, automate giving, automate bill pay, automate portfolio rebalancing, etc. We possess a finite amount of mental capital, and when we have too many choices and decisions to spend it on, we simply increase the odds of running out when we need it most.

- Reduce reliance on particular strategies or outcomes. Maybe that’s a long way of saying “diversify.” If one particular investment or other financial decision has to go well for you to reach your financial goals, it either 1) Won’t go well, and you won’t reach your goal, or 2) Will go well, and you’ll keep trying this strategy until 1) happens.

- Reduce lifestyle creep. Lifestyle creep is not only detrimental to retirement planning, but it’s also detrimental to our pre-retirement lives. If our purchasing increases in lock-step with our incomes, then we will find ourselves constantly trying to solve problems with “more” or “newer” or “neater” without actually getting to better. Sometimes we just need to get rid of stuff, or maybe even space, to solve a problem, and in the process we’ve saved money rather than spent it (like in the Lego example above!).

- Reduce miscellaneous. These aren’t inherently financial, per se, but they are subtractive changes that at least have financial impacts: Reduce your commute, reduce screen time, reduce calendar activities, and lastly, give more money away! (You knew that was coming…).

As the study that prompted this Brief shows, choosing subtractive changes is often the difficult, uncommon choice—we would write shorter letters if we had the time!—but these sorts of uncommon choices are part of why we exist as a firm. Uncommon choices are easier to make with someone who’s made them before and lived to tell the tale.

What about you? What are some subtractive changes you’ve made in your own life that have been better, more efficient solutions?