25 Mar 2021 Shooter McGavin and the “Secret of the Pros.”

Happy Gilmore was released in 1996. Three years later I started college and during my freshman year many an evening ended with me and my roommate, Andy Hilton, grabbing the VHS off the shelf to watch the Adam Sandler classic. If you told me back in 1999 that more than 20 years later I’d be writing a brief tying it together with investing, I would have choked on my ramen noodles. But alas, here we are.

For the unfamiliar, Happy Gilmore tells the story of a hockey-player-turned-golfer (with, shall we say, a “distinctive” swing) who joins the PGA Tour in an effort to save his grandmother’s house. At his first event, Shooter McGavin, the hottest golfer on tour, extends him an invitation that, at first, seems genuine.

“If you’re not doing anything later, why don’t you join us at 9 o’clock on the 9th green,” he says.

“What happens there?” asks a curious Happy.

“Eh, it’s a secret of the pros,” says Shooter, leaning in and dropping his voice an octave lower.

Sure enough, Happy goes out to the 9th green at 9 o’clock wearing his best suit (his only suit) and is promptly soaked by the automatic sprinklers.

______________________________________________________________

Early in my career I spent a lot of time researching active mutual funds for use in client portfolios. Using screens, funds could be ranked or categorized by any number of criteria. The objective was to find the “best of breed” for our clients and I believed, using the tools at my disposal, finding them was only a matter of time.

Turns out, I could have saved myself many hours and added a lot of value to client portfolios by understanding two “secrets of the pros” that I didn’t learn until much later: first, the overwhelming majority of actively-managed mutual funds underperform their benchmark and, second, the most reliable predictor of future performance is fees.

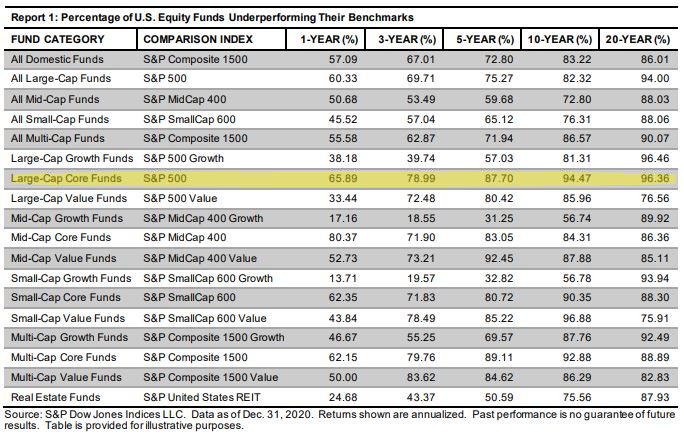

To prove the first “secret”, here’s a snapshot of the latest SPIVA Report, or “S&P Indices versus Active.” The goal of the report: to track how actively-managed mutual funds perform relative to their benchmark. In other words: are the high fees they charge justified by higher performance?

The answer is a resounding no. Focus on the highlighted line which shows U.S. stock mutual funds whose stated mission is to beat the S&P 500 index. What percentage underperform? Well, the one year number isn’t bad, relatively: in 2020, 65% didn’t beat their benchmark. Stretch the time horizon out to the trailing three years and nearly 79% underperformed. Look back over the last 10 years and almost 95% of mutual funds trying to beat the S&P 500 failed.

But, I might have told myself in the early days of my career, look at the all the tools I have! Certainly, I can find the 5% that outperformed. The trouble is that there’s only one reliable piece of data that positively impacts future performance. It’s not who the manager is or how long he or she has been at the helm, it’s not past performance, or fund size or number of holdings. It’s much simpler than that.

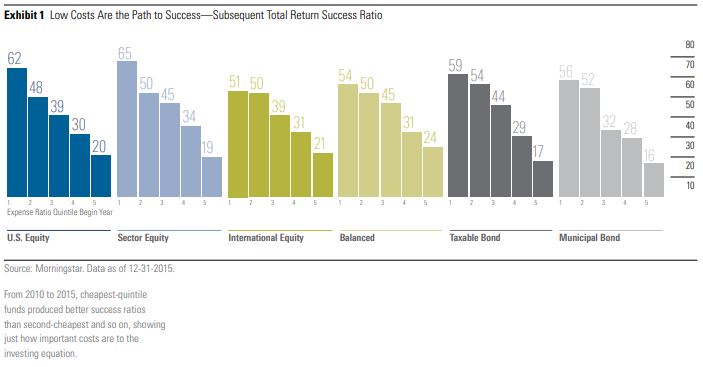

Which brings me to the second “secret”: the most reliable predictor of future performance is fees. The data below, courtesy of Morningstar, breaks down a mutual fund’s “success ratio” based on their relative fees. As you can see, funds in the cheapest-quintile have a higher ratio.

It’s that simple: lower fees increase the likelihood of superior performance. Since actively-managed mutual funds charge, on average, fives times as much as a passively-managed index fund, the odds they’ll beat their benchmark are dramatically lower. That’s why, at Beacon Wealthcare, we only use index funds, whose goal is to match the returns of the benchmark.

_____________________________________________________________

The investment industry is a bit like Shooter McGavin holding court at a party the night before an event. But instead of leaning in and, in a quiet voice, asking you to join them on the 9th green at 9, they advertise on the TV, podcasts, send you invites in the mail to fancy dinners, or by running banners on websites. They talk about their investment process as if that’s the secret to better performance, when the reality is that the field is too competitive, too expensive, and too crowded. That’s why 95% failed to beat their benchmark over the last 10 years. It’s just too hard and there’s little-to-no edge left.

These are the real secrets: fees matter most in investment selection, and most managers aren’t able to add value.

Avoid their invites. Otherwise, you might find yourself soaked.