19 Jan 2023 One For The Books

2022 was a tough year to be an investor. Supply chain bottlenecks, the highest inflation we’ve seen in 40 years, the war in Ukraine and a very aggressive Federal Reserve all ran headlong into elevated stock and bond valuations creating an unpleasant scenario for most investors’ portfolios.

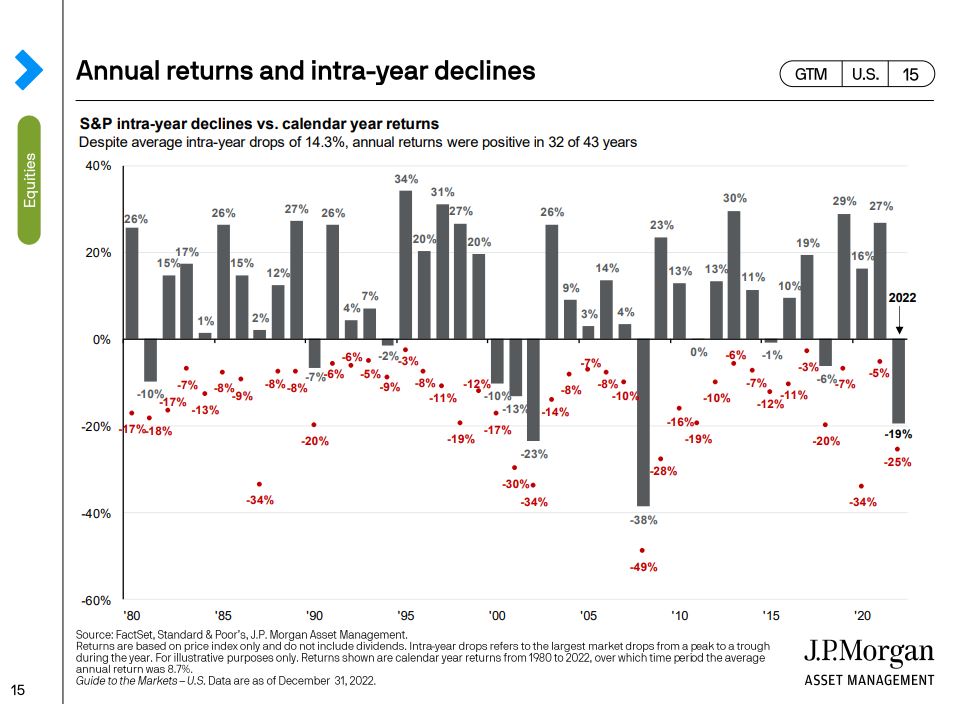

When it was all said and done, the stock market, as measured by the S&P 500, ended the year down over 18%. The chart below, from JP Morgan’s Guide to the Markets, shows annual returns (gray bars) going back to 1980 along with the intra-year pullback (red dots). As you can see, 2022 finished the year with its worst annual return since 2008. It’s also worth noting that, while we did experience some intra-year volatility, we’d gotten pretty used to seeing double digit positive annual returns over the last decade or so.

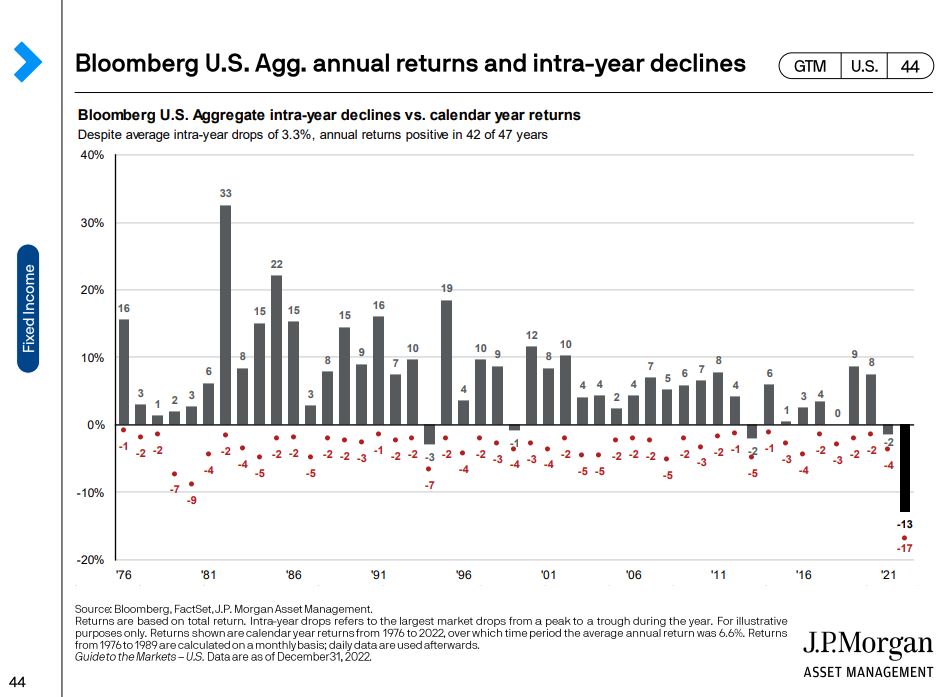

And if that weren’t enough, bonds, which typically provide ballast against the gyrations of the equity markets were down in 2022 as well. In fact, it was the worst year ever for the Bloomberg Aggregate Bond Market Index, which dates back to 1976.

By the end of the year, a typical 60/40 portfolio of U.S. stocks and bonds was down around 16%, making 2022 the third worst year ever for a diversified portfolio. A tough year to be an investor, indeed.

With 2022 behind us, we now turn our attention to the future. I don’t know what 2023 has in store for the stock and bond markets, but as I write this, we’re off to a decent start. The S&P 500 is up 2.39% and the Bloomberg Aggregate Bond Market Index is up 3.79%. I have to admit, it feels good to be able to report returns without having to use a minus sign or parentheses! It’s still very early in the year but there may be a few things we can feel encouraged about.

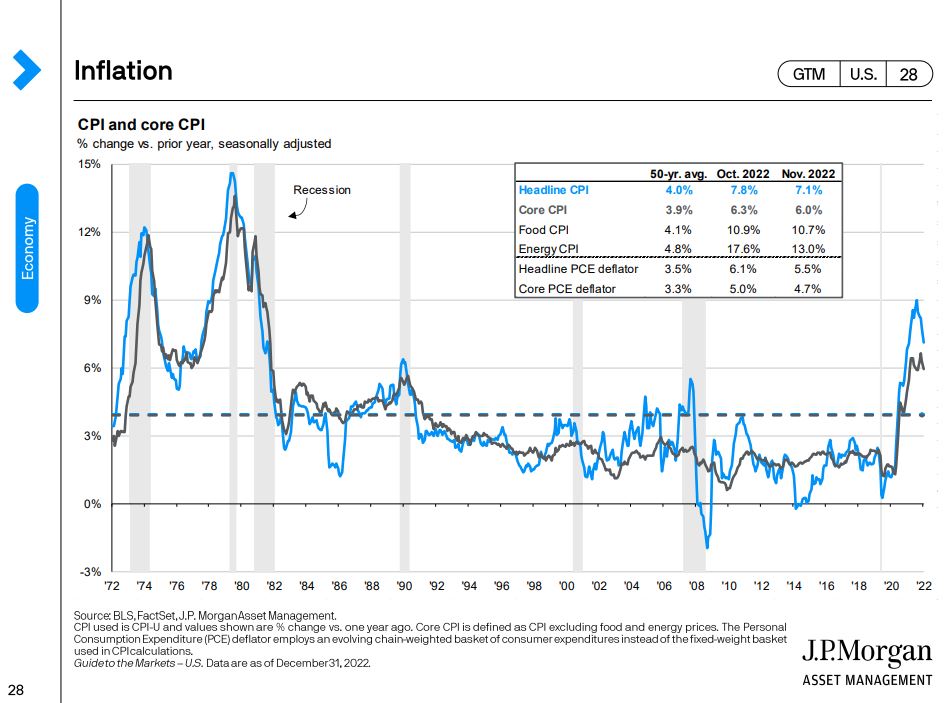

Inflation may have peaked.

One of the big questions for investors in 2023 is whether Jerome Powell and the Federal Reserve will be able to get a handle on inflation without causing a recession, accomplishing what is known as a “soft landing.” If they raise rates too fast or too far, they risk driving the economy into a deep recession. But if they take their foot off the brake too soon, inflation could come roaring back. It’s a delicate balance. Six months ago, a recession seemed all but inevitable but now it feels like less of a forgone conclusion. As you can see in the chart below, Headline and Core inflation may have peaked while we still have a healthy labor market, two key factors in taming inflation without causing too much damage to the economy.

Expected returns for stocks and bonds are are now higher now than they were a year ago.

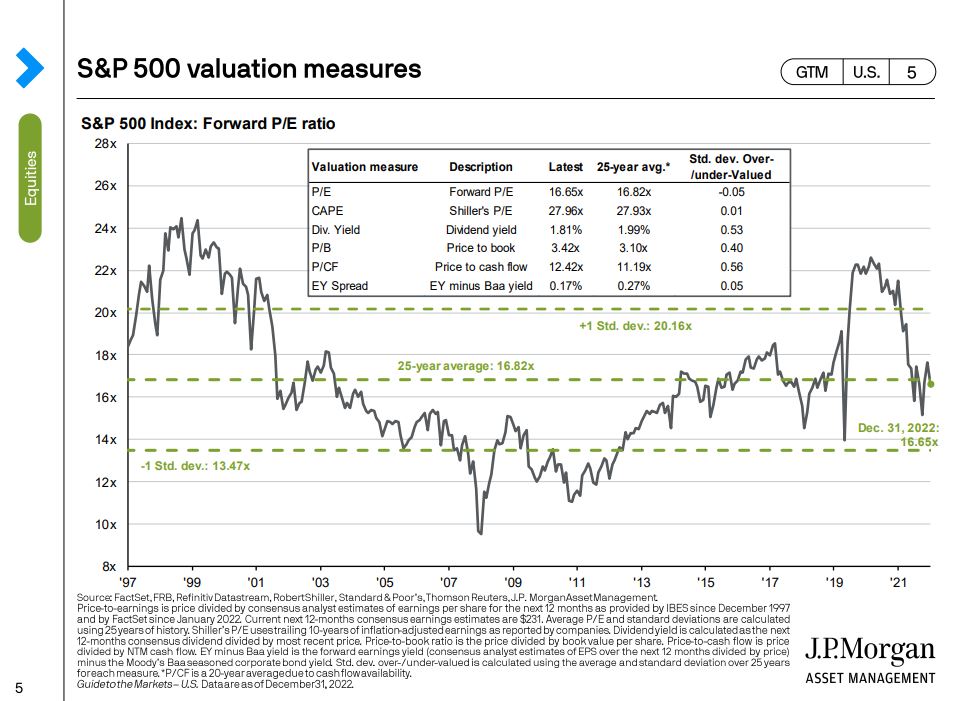

The more expensive an investment is, the lower your future returns are projected to be, ceteris paribus (finally, I get to use some of the Latin I learned 30 years ago in Economics 101!). A commonly used metric to value an investment or index is its price-to-earnings ratio, or “P/E” ratio. You can apply it to a market index, the S&P 500, for example, or an individual stock. You simply divide the investment’s price by its earnings per share to calculate its P/E ratio, which tells us how many times current earnings the market is willing to pay for that particular investment. Over the last 25 years, the S&P 500’s average P/E ratio has been 16.82. Anything higher than that number could mean the S&P 500 is relatively expensive, and the more expensive an investment is, the lower its expected return.

At the beginning of 2022, the P/E ratio for the S&P 500 was close to 23, as expensive as it’s been in over 20 years. You can see in the chart below, again from JP Morgan, that the S&P 500 ended 2022 with a P/E ratio of 16.65, about as average as you can get.

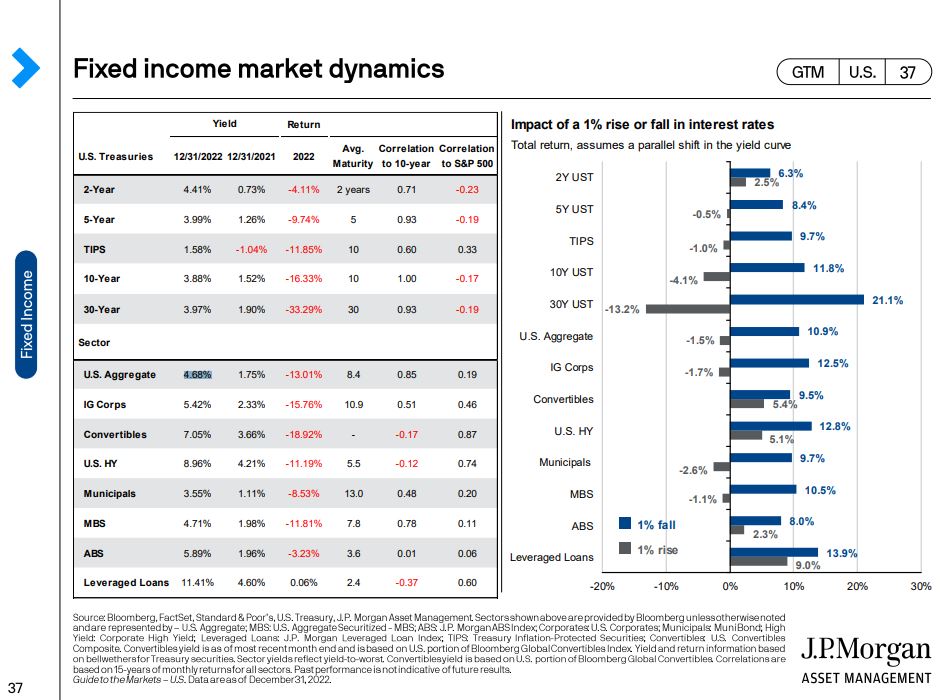

The combination of events we experienced in 2022 probably means more income from bonds going forward.

With the 2-Year Treasury yield at 4.41% and the U.S. Aggregate Index yield at 4.68%, bond investors are finally earning some income on the fixed income side of their portfolios. That’s a good thing whether you’re spending that income or reinvesting it for the future. Not to mention the fact that it can help dampen the effects of stock market volatility and insulate bond returns from potential future interest rate hikes.

Yes, 2022 was a tough year to be an investor. Hopefully the positive momentum we’ve experienced so far in 2023 will continue (but not so much so that it reignites inflation!) As I’ve written before, it can be difficult to keep a cool head during times of economic and investment uncertainty. Over the last few months, I’ve written about potential ways to survive a difficult market here and here. I hope you will also feel free to reach out to us if you you’re feeling concerned or have questions. We’d be happy to chat.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.