11 Feb 2021 The Four Taxes Most Retirees Will Face and What They Mean For Young Professionals

When it comes to income planning in retirement, it is crucial to understand the four primary taxes you will have to navigate. If you navigate them well, you can keep more of your money and send less to the IRS.

The first tax you will face is ordinary income tax. Most likely, you’ve paid these your entire life and thus are familiar with them. Here in the U.S. we have a progressive tax system which means you pay less in federal taxes on the first dollar you earn and more on the last dollar you earn. The chart below shows 2021 federal income tax brackets:

The next tax is on capital gains, which come from investments like stocks and bonds, and there are two kinds: short-term, when you own an investment for less than a year, and long-term, when you own an investment for more than a year. Short-term are particularly onerous because they are taxed as ordinary income, while long-term receive preferential tax treatment. In fact, there are situations where your federal tax rate on long-term capital gains can be 0% and others where it can be as high as 23.8% when you factor in the Net Investment Income Tax which was instituted as part of the Affordable Care Act. Capital gains are stacked on top of ordinary income to calculate the rate at which they are taxed.

Next is the tax you pay on Social Security benefits. Anywhere from 0% to 85% of the benefits you receive can be subject to federal taxation and how much depends on something called “Provisional Income”. That Social Security benefits are more tax-efficient than other sources of taxable income, including withdrawals from pre-tax IRAs, is a significant reason that delaying benefits until age 70 can be in your best interest.

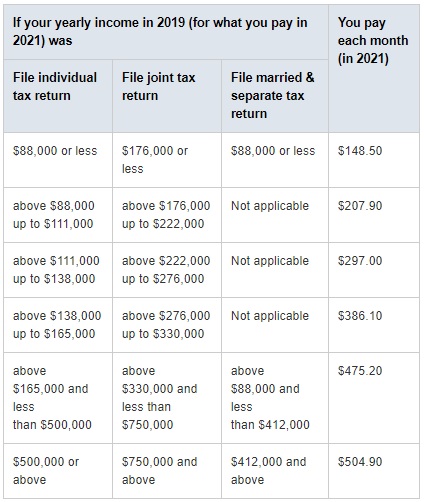

The final tax, though it’s technically not a tax, concerns your Medicare Part B premiums. It’s called an Income Related Monthly Adjustment Amount, or IRMAA. If your income is high enough you will see your Medicare Part B premiums double or even triple. In 2021, Part B monthly premiums start at $148.50 but as your taxable income increases, premiums ratchet up, as you can see below:

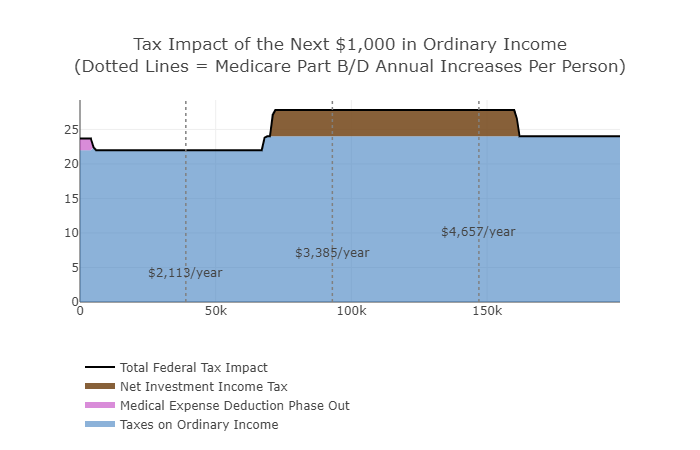

The important take-away from all this is: these four taxes are interrelated. Increasing taxable income by a dollar may not just result in more ordinary income taxes paid, it may also increase your capital gains rate and the amount of your Social Security benefits subject to taxation. It could even increase your Medicare Part B premiums. The chart below depicts some of this:

As income increases (moving from left to right on the x-axis), you can see how your ordinary income tax rate, the blue shaded region, increases (y-axis). As it increases, Net Investment Income Tax (in brown) is tacked on due to capital gains that occurred during the year. The vertical dotted lines shows income amounts at which Medicare Part B premiums increase. (Taxation of Social Security benefits and capital gains rates are not shown.) Again, they’re all connected.

These four taxes have implications for young professionals, too. Ideally, you are saving to different kinds of accounts, Traditional, Roth, brokerage, so that you have tax-flexibility in retirement. Too much of one can make your retirement income plan too brittle or cause needless taxation during your career.

Understanding how the tax code works and how to navigate it is a crucial piece of your financial plan and involves having a financial team (CFP®, CPA) working on your behalf.

If we’re not yet a part of your financial team, we’d love to be. Schedule a call to learn more about how we can help.