13 May 2021 My Favorite Investment Story

“We are, as a species, addicted to story. Even when the body goes to sleep, the mind stays up all night, telling itself stories.” — Jonathan Gottschall, The Storytelling Animal: How Stories Make Us Human

We all love to hear stories. A really good one can teach us, inspire our imaginations, create common experiences, unite us with others and even move us to take action.

There is actually a scientific explanation for why we love stories. Hearing a story that resonates with us increases our levels of a hormone called oxytocin. Oxytocin is a hormone that boosts our feelings of empathy, compassion and cooperation. It motivates us to work with others and it positively influences our social behavior. It’s because of this that stories have a unique ability to build connections and enhance our relationships.

I love to hear good stories about all kinds of things; great adventures, historical events, embarrassing moments. But some of my favorite stories are about things people have learned during their lifetimes about investing. I know it’s a bit nerdy but good investment stories often involve excitement, intrigue, wins, losses, mystery and regret. Do you have a favorite investment story that you love to tell?

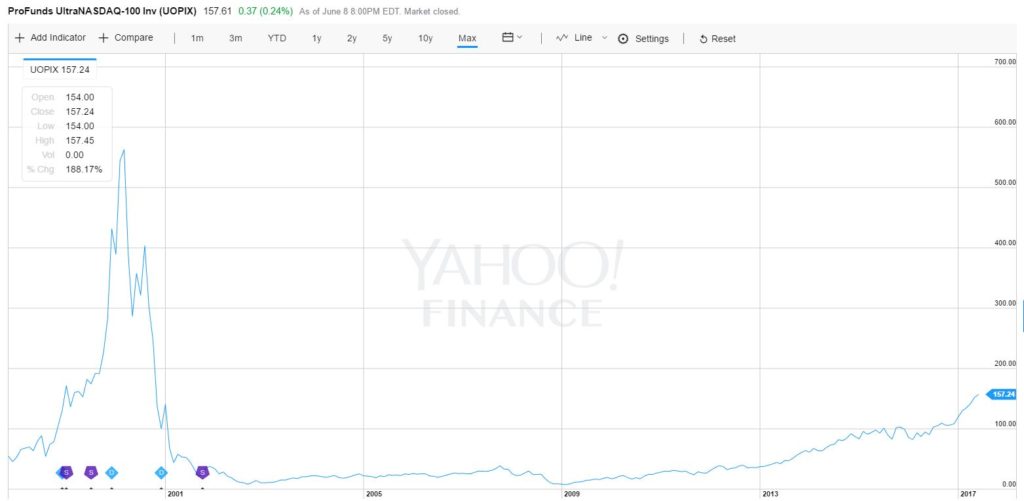

One of my favorites is a story about my investment in the ProFunds Ultra OTC mutual fund. This particular fund’s objective was to offer a return equivalent to 2x the return on the NASDAQ 100, the index containing all the big tech names of the the time. So if the NASDAQ 100 was up 2% on a particular day my investment in the fund would be up 4% but if the index was down 2%, well, you know. It was the boom years of the tech bubble in the late nineties when, at age 28, I remember realizing that my $10k investment had grown to $90k in just a year or two! It’s true, I was a financial advisor at that time and, yes, a prudent investor probably should have taken some off the table. However, a quick glance at my 2001 tax form Schedule D reminds me that I sold my Profunds investment for $6k after the tech bubble had burst. I can’t tell you why I didn’t at least sell some of my shares earlier other than that it had something to do with not wanting to pay taxes, hubris, fear of missing out on further gains and sheer greed. That was a painful lesson to learn at age 28, but I’m thankful that I learned it then and not later in my investing career when the stakes were much higher.

We should expect inevitable ups and downs any time we invest money in the stock market. However, having a concentrated bet on one stock or one market sector can unnecessarily magnify the ups and downs we experience. Concentrated investment positions can come about in several ways. Sometimes they come about when we inherit shares of stock from a relative or when we participate in our company’s stock option or stock purchase plan over a long period of time. Other times, they come about when we get in early on a stock that turns out to be a home run. Regardless, the time to address these positions is before you experience an outcome that negatively impacts your financial plan or causes lifelong (not to be dramatic, but it happens) regret.

Last year, I wrote about how large U.S. technology stocks had become an outsized percentage of most peoples investment portfolios. In my Brief, I suggested an exercise to calculate how much of your portfolio was in the big stocks like Apple, Amazon, Google or even Tesla. That same exercise still works and can also be used to calculate your total holdings in other types of stock, including public company employer stock. As a shortcut, you could also simply look for investment positions in individual stocks or market sectors that make up more than 5% of your total holdings. However you decide to do it, now is a good time to assess your exposure to individual concentrated positions.

To be clear, I’m not predicting the future of the stock market and I’m not calling for another tech bust. Nobody can do that successfully. It’s just that minimizing unnecessary risk and maintaining a diversified portfolio are both important regardless of what’s going on in the world. If you calculate that you’ve got more exposure to a particular stock than you’d like, please consult with one of us at Beacon or your tax advisor before making any changes. Reducing your exposure could come with tax consequences so it’s important to navigate the process well. But, doing so could keep you from having a Profunds story of your own.

Let us know how we can help.