15 Oct 2020 Four Considerations As You Choose Employee Benefits

Benefits season is nearly upon us! The time when employees across the country pick their health insurance and other benefits for the coming year. With this in mind, here are four considerations as you choose your benefits.

Change How You Pay for Group Long-Term Disability Insurance?

Disability insurance is a must-have and, sadly, often the most overlooked form of insurance. Life insurance garners most of the attention but disability is 2.5x more common than death for men and 5x more common for women, according to the Social Security Administration.

Most employees pay the premiums for group long-term disability insurance with pre-tax dollars. By doing this, any benefits received are fully taxable based on your income tax bracket.

Consider switching your premiums to post-tax. Not all employers provide this option but if you are able to, I strongly recommend you give it some thought. The advantage is that if you ever receive disability insurance payments based on a policy paid with post-tax dollars, the benefits are received income-tax free. Yes, it will cost you a little more now but tax-free benefits if you are disabled is a strong incentive.

Group Life Insurance Can Lose Its Appeal As You Age

Employees in their 20’s and 30’s at large companies can generally purchase generous group life insurance at a staggeringly low cost. However, most group life insurance coverage is “age-banded” and the older you get the more expensive coverage becomes.

In the example to the right, group life insurance premiums start quite low and increase as you move from one age-band to the next. At age 30, an employee could purchase $500,000 of coverage for just under $480 per year. By age 45, where premiums really start to ratchet up, premiums have increased to $900 per year. At 50, it’s up to $1,380.

You may be better off purchasing a level-premium individual term policy, which, in addition to offering fixed premiums, isn’t tied to your employment.

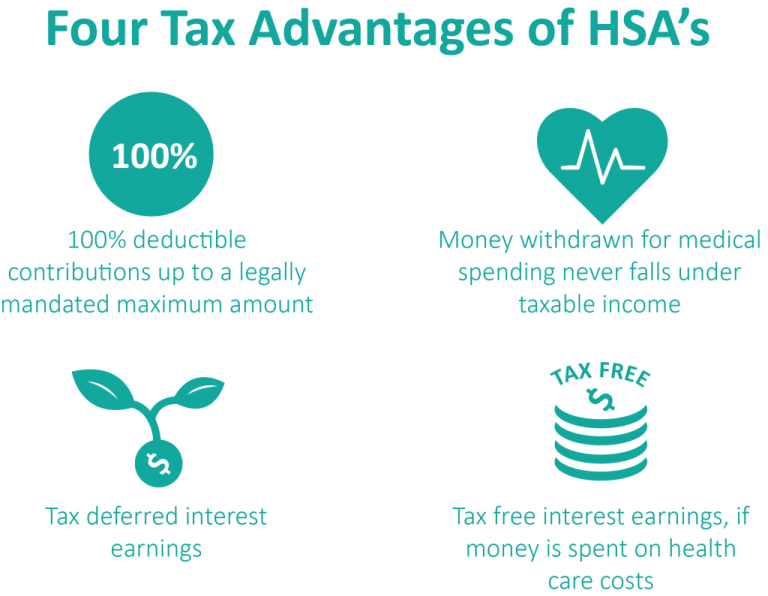

Health Savings Accounts (HSA) Offer a Triple-Tax Benefit

HSAs are unique in that they provide an income-tax deduction for contributions, tax-free growth, and tax-free withdrawals provided the money is used for a qualified medical expense. Additionally, funds in an HSA can be invested, but be sure to leave a sufficient amount in cash to cover a few years of your deductible. We’ve written about health savings accounts before and how wonderful they can be as another retirement savings account.

Oftentimes, employers will incentivize the use of health insurance plans that include an HSA. Cisco and GSK, for example, are two large employers in the Triangle who in the past have offered to contribute money to an HSA if an employee selects that health insurance plan.

Oftentimes, employers will incentivize the use of health insurance plans that include an HSA. Cisco and GSK, for example, are two large employers in the Triangle who in the past have offered to contribute money to an HSA if an employee selects that health insurance plan.

Because HSAs are tied to high-deductible health insurance plans you may be faced with a higher deductible than what you could get with another option, so be sure to understand the tradeoffs. When used optimally, an HSA can provide immediate and future benefits.

Employee Stock Purchase Programs (ESPP) Are a Great Way to Build Wealth, Provided…

A few months back I did a vlog on ESPPs. They are only offered by public companies and thus not as prevalent, but they provide a way to purchase shares of your employer stock at a discount off the purchase price along with the ability to purchase at the lower price between the start and end date of the offering period. This essentially amounts to a “guaranteed” (nothing is guaranteed) return. If you participate, it’s crucial to understand the taxation and to commit to selling the shares of stock as soon as you are able. Accruing too much employer stock is an easy trap to fall into.

Avoid the temptation to default to the benefits you chose last year. Your life has certainly changed, benefits may have changed, and there may be ways to improve coverage, save money, and secure a better financial future. A benefits review is one of the services we offer to all our clients, but if you’re not a client and are interested in having us take a look, please schedule a call by clicking here.