24 Feb 2022 What’s $1,000 Worth?

What’s $1,000 worth? As with most things in personal finance, the answer is, “It depends.” Are we talking about a thousand bucks received a year ago? If so, then about 7.5% more than if received today. If used to reduce debt, it’s worth $1,000, unless of course it’s an extra payment against a mortgage or a student loan. Then it’s worth more. The same $1,000 contributed to Social Security is often worth less than $1,000. What about $1,000 invested? What’s that worth?

A few weeks ago, Geoff and I spoke to the Raleigh Fellows about personal finance. At the conclusion of our talk, a young woman asked, “A friend says I should invest $6,000 a year, but I don’t have that much right now. Is it worth it if I can only invest $1,000?”

The answer to that question is, for many reasons, an unequivocal “Yes!” So, if this young woman forgoes spending it and instead invests it, what will it be worth? As you can imagine, it depends.

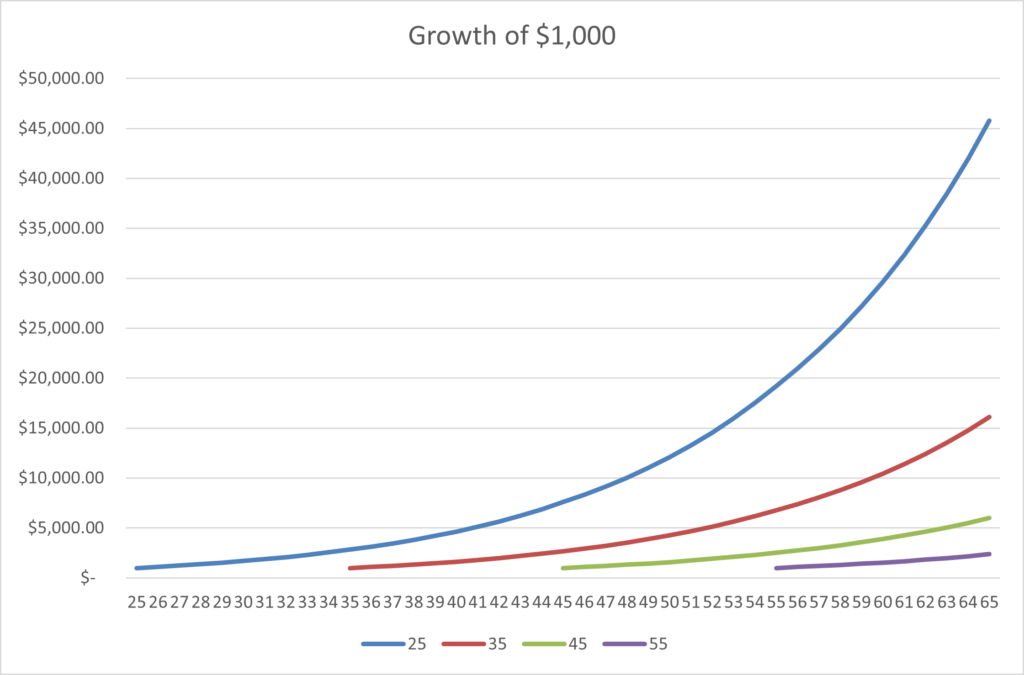

To get a clearer idea, let’s look at four different investors*. They each invest $1,000 in a simple portfolio of two investments: U.S. Stocks and Treasury Bonds. All that’s different is the age that they make the investment: the first invests when she is 25, the second, when she is 35, the third, 45, and the fourth, at 55. What’s it worth by age 65?

For the 25-year-old, that initial investment turns into $45,790. A 35-year-old would see $1,000 turn into $16,130, the 45-year-old’s $1,000 become $6,020 and the 55-year-old a bit more than doubles her money and sees $1,000 grow to $2,380.

Notably, an investor with a 40-year time horizon accumulated nearly 3x more than the 30-year investor. The extra ten years of compounding dramatically increases wealth creation. Look at how much growth happens over the final 10 years of the 40-year period (blue line). This is why starting early is so important and speaks to the immense power of compound interest.

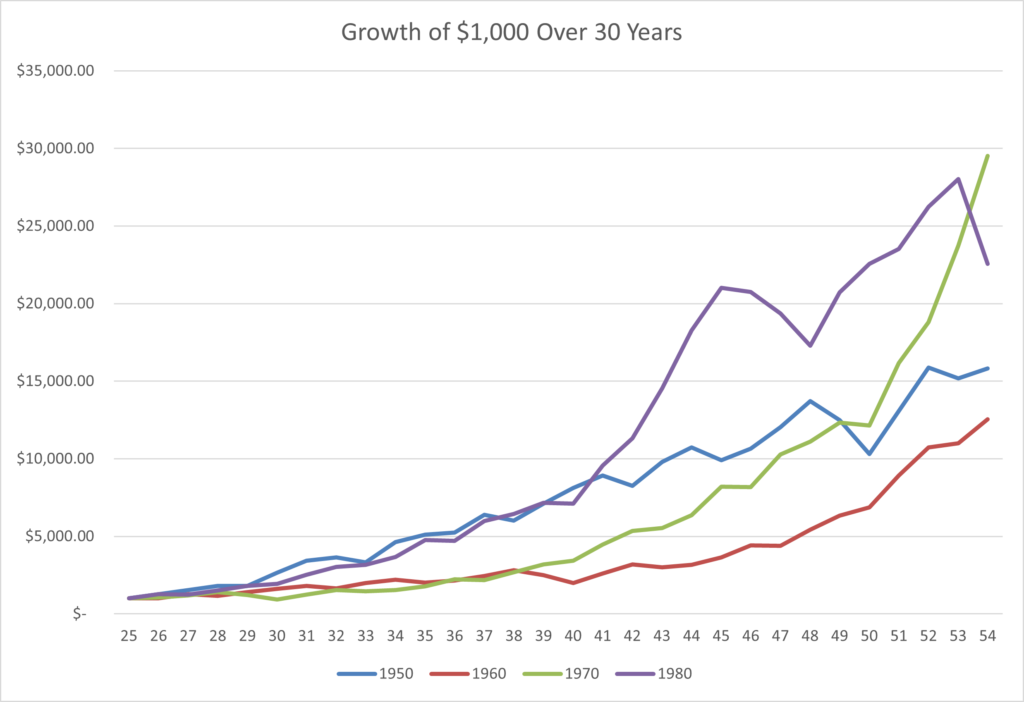

What if we move the example into the real world? That is, what if a 25-year-old invested $1,000 on January 1st, 1950, and didn’t touch it for 30 years?** How much would it be worth? What about January 1st, 1960? 1970? 1980?

As you can see, making a 30-year investment at the start of 1970 would have yielded the most return; 1960, the least. It’s also interesting to note the spread of returns. Depending on when you started investing, you could have ended up with a little more than $12,000 or a little less than $30,000.

Here are the ending values depending on when the initial investment was made:

-

- 1950: $15,830

- 1960: $12,540

- 1970: $29,510

- 1980: $22,560

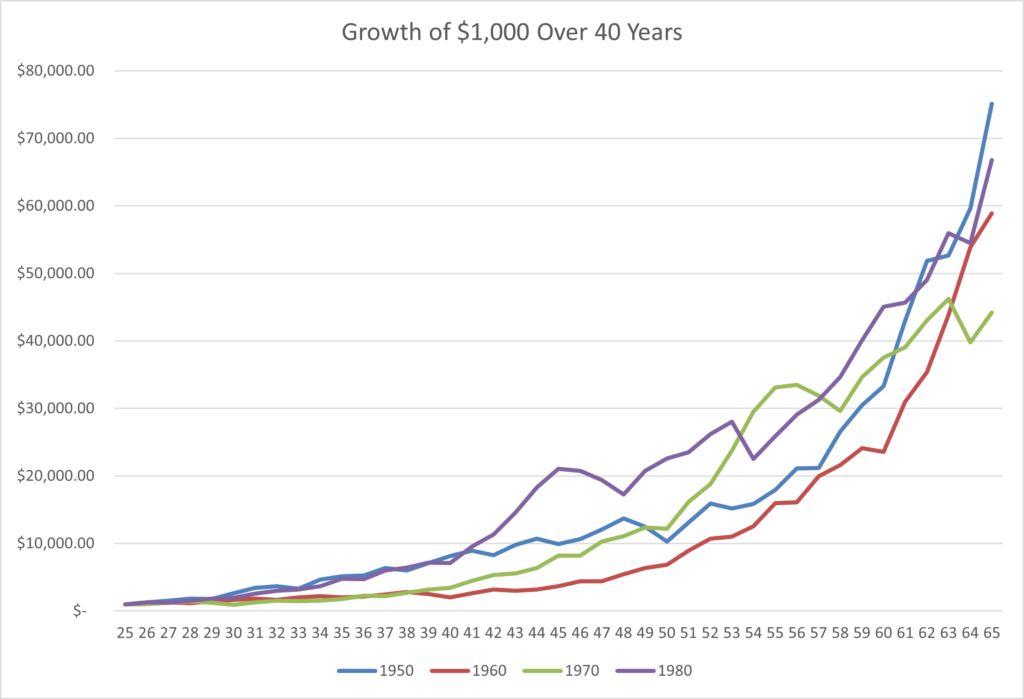

What about a 40-year investment?

Here are the ending values:

-

- 1950: $75,100

- 1960: $58,800

- 1970: $44,200

- 1980: $66,820

Interestingly, the 1970’s investor has gone from best to worst. Why? You can reduce it to one year: 2008. When her portfolio hit its highest point, boom, the Great Recession.

Back to the original question: what’s $1,000 worth? It depends. It depends on when you invest, how long you invest, and when you spend, all other things being equal.

Ultimately, though, we get to decide what $1,000 is worth by how we use it. Is it worth less? That is, do we spend it on things fleeting, of little long-term value or meaning? Or is it worth more? Do we put it towards what matters, what we prioritize? Do we spend it intentionally?

Our hope at Beacon Wealthcare is that you will get the highest value out of each dollar earned, invested, and spent. If you aren’t sure what that looks like, we’d love to help.

*Key assumptions:

-

- No taxes;

- Portfolio allocation is as follows:

- 90% US Stocks, 10% Treasury Bonds from ages 25-34;

- 80% US Stocks, 20% Treasury Bonds from ages 35-44;

- 70% US Stocks, 30% Treasury Bonds from ages 45-54;

- 60% US Stocks, 40% Treasury Bonds from ages 55-65;

- Long-term average returns can be found here: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

**The idea of investing during different decades was inspired by a post I read, but cannot now find, from Morgan Housel.

Charts are for illustrative purposes only. There is no guarantee any investment will produce positive returns.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.