04 Mar 2021 “Watch out for inflation!” I said in 2009. (The futility of predictions.)

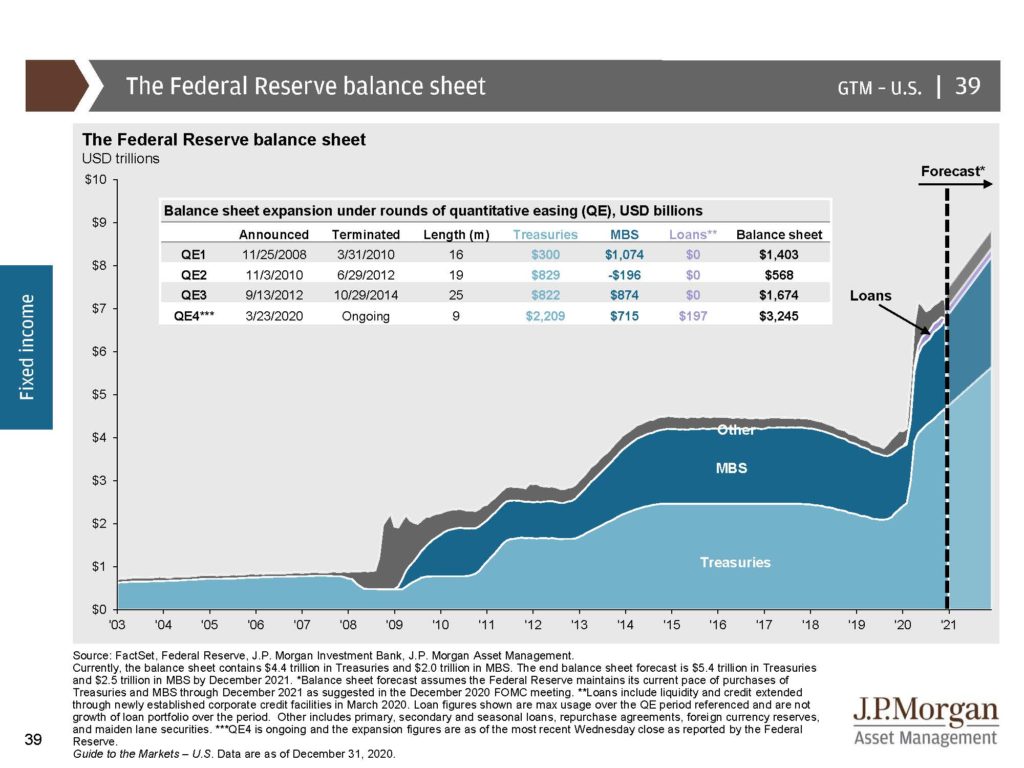

The Great Recession began in October of 2007. Financial institutions failed, families lost their homes, the unemployment rate doubled, and the stock market dropped over 60%. In November of 2008 the Federal Reserve launched “QE 1” and began buying up “toxic” assets, i.e., mortgages at risk of default, to prevent the financial system from seizing. That year the size of the Federal Reserve’s balance sheet doubled from around $1T to over $2T. They continued buying and by 2014 their assets were over $4T. As of right now that figure stands at $7T, largely due to the COVID-19 stimulus.

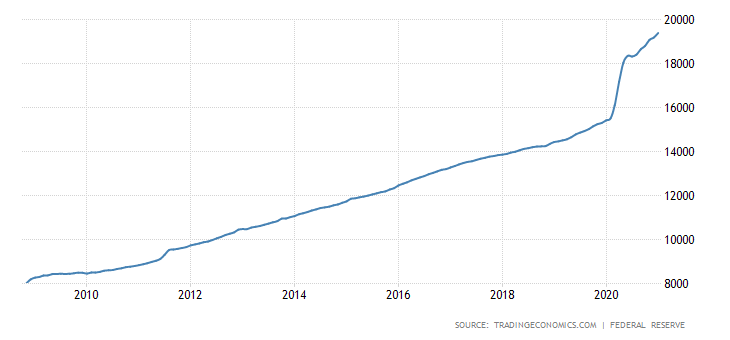

One of the first relationships you learn about in the study of economics is the one between supply and demand. During the early years of Quantitative Easing (“QE”), a concerned shared by many economists was that the excessive supply of money would push up the demand for goods, thereby increasing prices at an uncontrollable rate. Economists weren’t the only ones sounding the alarm back then about runaway inflation. I was, too. Can you blame us? Look at the increase in Money Supply since the QE programs began:

Anyone who knew in advance how much money would be pushed into the financial system would have been worried. Yet, inflation never materialized. In fact, since QE began inflation has been running lower than normal. Why? Probably a combination of factors: Demand never increased, companies became more efficient, globalization kept prices low. No matter, it was a horrible call on my part and, if I had acted on it and positioned my portfolio to benefit from high inflation, overweighting things like stocks, commodities, real estate, and Treasury Inflation-Protected Securities (TIPS), my returns would have suffered. Commodities have been terrible the last dozen years, real estate hasn’t outperformed, particularly when adjusted for risk, and TIPS have earned less than Treasuries. Stocks have done great but the rest of my portfolio would have lagged.

But let’s say I got it right, low inflation, and took the opposite tack. Well, then I may have underweighted stocks, which would have been disastrous! It’s like Geoff wrote about in December: investing is really hard, even with a crystal ball.

Of course, building an entire investment thesis around one data point, inflation, in my example, is foolish. You have to account for many other things. But it’s just that, the need to make sense of so many data points, that makes predicting the direction of the market so challenging.

Thankfully, there’s a better option: controlling the things that can be controlled. That’s why our focus is on keeping investment expenses low, taxes at a minimum, reducing the risk of underperformance, and keeping you accountable to saving an appropriate amount of your income every month (or, if you’re retired, spending an appropriate amount). Personally, I find relief in these things. I can’t control the stock market so my attempts at it only result in frustration. But I can control my savings. I can control what I invest in. And, to a certain extent, I can control how they impact my taxes.

Predictions have their place in the world. The prediction that someday our lives would return to normal gave me tremendous hope during the early days of the pandemic. But they don’t belong in your portfolio.

Interested in learning more about how we can help? Click here.