28 Apr 2022 Treasury Bonds and the Beauty of Correlation

Four weeks ago, I argued that the correction the stock market experienced earlier this year was entirely normal. What that brief omitted was any real discussion of the bond market which, as you may have heard, is having its own problems. The instigator of most of them is inflation, currently rising at a white-hot 8.5%. While prices are up across the board, the worst culprits are used cars and trucks (+35% from March, 2021 through March, 2022), gasoline (+48%), fuel oil (+70%), and “meats, poultry, fish and eggs” (+13.7%). While we may be able to delay the purchase of a new or used car, all of us are impacted by the increase in food and fuel prices. (Follow this link if you want to dig into what’s driving inflation.)

On their own, large price increases inhibit bond returns, but when you combine it with the necessary response by the Federal Reserve–raising interest rates–you create a toxic environment for fixed income.

Today we’ll cover three things. First, a quick description of what bonds are, second, the role they play in your portfolio, and third, why we believe U.S. Treasuries are the best bonds for you to invest in.

First, a primer on bonds. A bond is a form of debt issued by a company (Google, Apple, JP Morgan, etc.), municipality (Wake County, Mecklenburg County, etc.) or government. The purchasers of bonds are lending their money to the issuer for a certain period of time (the “term”) in exchange for a fixed rate of interest. The rate of interest received depends on a few things: how long the bond is issued for, the creditworthiness of the issuer, and prevailing market interest rates. Once the term is up, the purchaser receives their money back. Issuers will sell bonds for a host of reasons: building a factory or school, financing operations, or to acquire a company, to name a few. In general, bonds are less risky than stocks because, as a debtor of the company, the purchaser is first in line to be paid back if the issuer goes out of business.

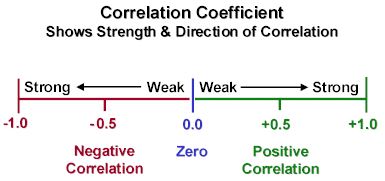

Second, the role they play in your portfolio. It’s often said that you should invest in bonds for income. While that is true, income as a reason is a distant second to reducing the risk of your portfolio. Simply put, bonds tend to zig when the stock market zags. This zig-zag relationship can be quantified as the “Correlation Coefficient” and helps reduce the riskiness of your portfolio. Commonly referred to simply as “Correlation,” it is expressed as a number between -1 and +1 and answers the question: how much of the movement of one investment can be explained by the movement of another investment? A negative correlation means the investments will move opposite each other–as one rises, the other falls–while a positive correlation means they will move in the same direction, though the usefulness depends on the strength of the relationship, depicted below:

Because bonds are generally a more conservative investment and typically have a weak or negative correlation with stocks (“weak” means the movement of stocks has no impact on the movement of bonds), they can act as ballast when the stock market is taking on water. The beginning of the Pandemic provides us a recent example:

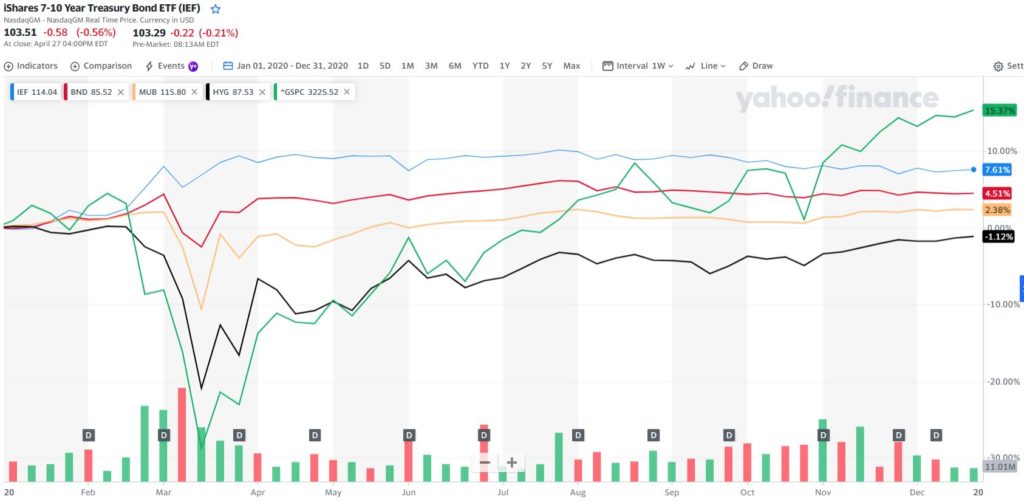

This chart, taken from Yahoo! Finance, runs from January 1st, 2020, through December 31st, 2020, and depicts five investments: Treasury bonds (blue), corporate bonds (red), municipal bonds (yellow), high-yield bonds (black) and the S&P 500 index (green). As you can see, the start of the Pandemic caused the stock market to fall more than 35% in five weeks. High yield bonds fell along with it. Municipal bonds, in yellow, held up better, corporate bonds better yet, while Treasuries were the runaway winner.

The Great Recession (2007-2009) shows similar results:

From October 2007, through mid-March, 2009, the stock market was halved with the carnage really ramping up in October of ’08. Again, you can see the relative steadiness of higher quality bonds. High-yield bonds, which tend to have a strong correlation with the stock market, offered no refuge.

Finally, why we believe U.S. Treasuries are the best bond investment for your portfolio. Because the role of bonds in your portfolio is to lessen the impact of negative stock market performance, we prefer ones that do that to the greatest extent possible. Looking at the two charts above, we see that the idea of Treasuries as a portfolio diversifier/risk-reducer passes the “eye-test”: they held up when stocks were down and did it better than the other major types of bonds.

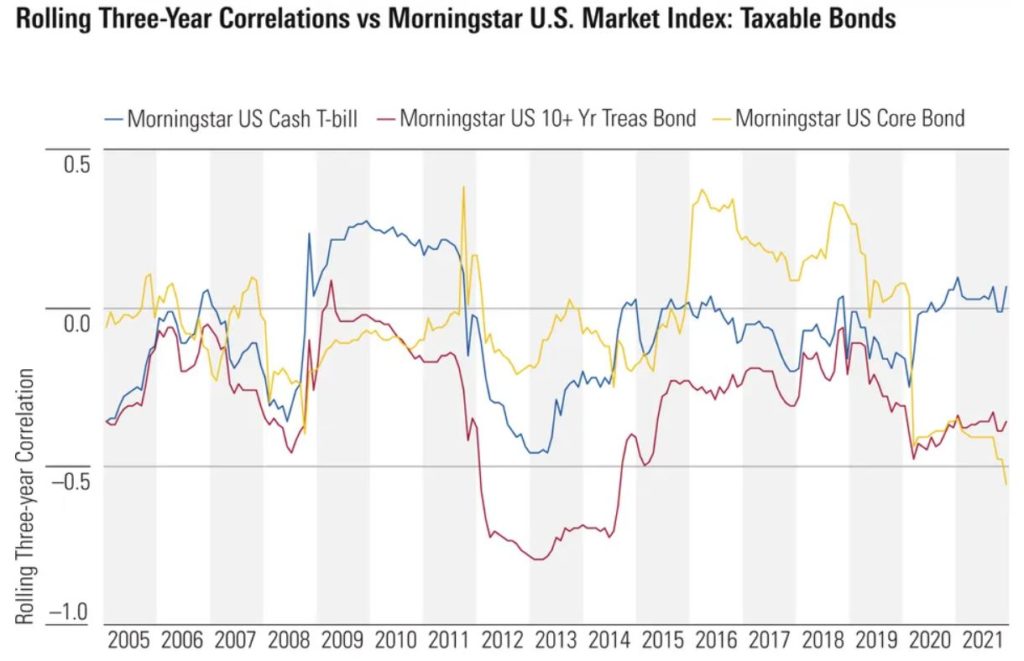

Thankfully, there is more evidence than this, courtesy of a recent post titled “Which Bonds Provide the Most Diversification for Stock Investors?” from Morningstar, a leading investment research firm. Here’s what they had to say: “Over the past two decades, Treasury bonds have provided the best diversification of any bond type–and indeed of any asset class–for investors with equity exposure in their portfolios. The correlation benefit was similar for Treasuries across the duration spectrum. Cash has been the next most attractive diversifier for stocks. The Morningstar US Core Bond Index, which is dominated by high-quality U.S. bonds, has also delivered a negative correlation with the equity market.” The rolling three-year correlation is shown below:

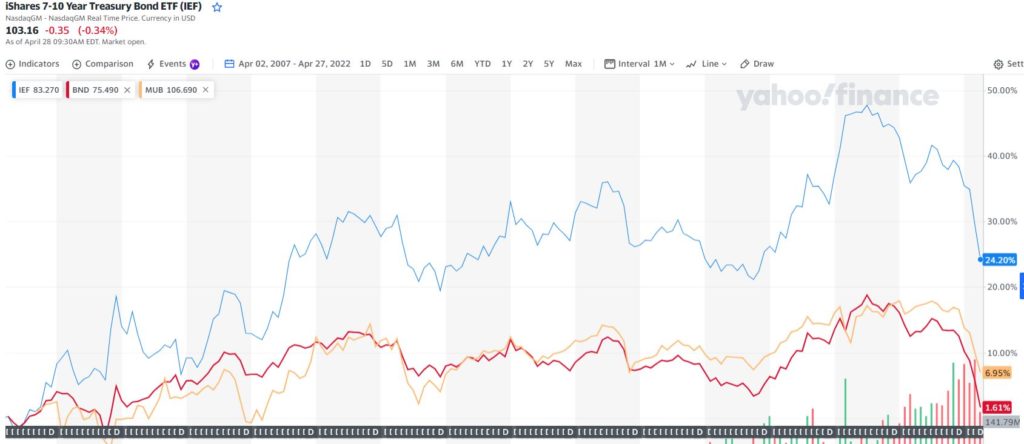

As you can see, except for short periods of time, Treasury bonds (red) have provided the greatest diversification from stocks over the past two decades. That doesn’t mean Treasuries have offered poor returns, though. Relative to high quality corporate bonds and municipal bonds, they have outperformed by a significant margin going back to 2007 (blue line represents Treasuries (+24.2%), yellow is municipal bonds (+6.95%), and red is corporate bonds (+1.61%)):

None of this is to say the current environment for bonds is ideal; it’s not. In fact, correlations for stock and bonds get stronger and more positive as inflation rises. That is, if high inflation is pushing down the price of stocks, it’s generally pushing down the price of all types of bonds, too. Inflation levels the playing field. But that doesn’t mean we remove bonds from a portfolio because there’s no telling when inflation will abate and there’s no telling when the next disruptive economic event will take place. Additionally, while rising interest rates can be somewhat painful for bondholders in the short term, they’re actually a good thing over the long haul. As I mentioned above, we own bonds for their diversification properties first and their interest payments second. With that said, it is nice to be compensated for holding on to our buffer. As new bonds are issued that pay a higher interest rate the yield on our bond investments will increase.

That’s why, in both good times and bad, you invest in bonds.

There’s no perfect portfolio, just like there’s no perfect bond. As I said four weeks ago, “The stock market is going through another of those times that test us as investors. ” The bond market is going through another one of those times, too.

If you find yourself worrying about your investments or obsessing over the state of your financial plan (or if you want to have a longer conversation about correlation!), please reach out to us.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.