30 Mar 2023 Three Takeaways from the Silicon Valley Bank Failure

Three weeks ago today, Silicon Valley Bank (SVB) was put into receivership by the Federal Deposit Insurance Corporation (FDIC) after experiencing outflows of more than $40B the day before. Since then, most of the conversation has focused on how the FDIC balances their own insurance caps with maintaining confidence in the banking sector (of particular importance in the case of SVB when more than 85% of depositors had balances over the FDIC limits), and figuring out who’s at fault.

While these two questions will take time to answer, I believe there are three more important lessons from the 2nd largest bank failure in U.S. history that we can immediately apply to our own finances.

Takeaway #1: Diversify

The easy lesson from all this is that you must maintain account balances equal-to-or-less-than the FDIC insurance amounts. If your balance exceeds the limits, you need another account at another bank. You need to diversify.

Rather than spending more time talking about bank accounts, let’s turn our attention to SVB’s employees. Here’s what one of them had to say:

“I’ve tried to ignore the personal side of this, but we’ve lost a lot. Many employees get more than 50% of their salaries in equity — SVB stock — every year. My equity in the few years I’ve been here used to be worth more than $1 million. Now it’s gone to zero. So here you have a whole group of people who lost everything personally….”

Oftentimes, we let employers have more influence than necessary over our finances. Really, apart from receiving a paycheck, we should have as few financial ties to our employer as possible. Two avoidable examples we regularly see are large amounts of company stock and no life or disability insurance apart from what you receive as an employee benefit. If you’re too dependent on your employer, the worst case scenario is the one SVB employees’ are facing right now: no income, employer stock worth zero, and no insurance. You may not be able to easily diversify where your income comes from, but you can diversify your investments and what protects your human capital.

Takeaway #2: You can be really smart and still be REALLY wrong

A big reason SVB found itself in trouble is that it believed interest rates would fall in 2023. When they didn’t and the bank needed cash to meet withdrawals, it had to sell investments at a significant loss.

This is a bit of a head-scratcher considering the bank’s CEO, Greg Becker, sat on the board of the Federal Reserve Bank of San Francisco. As you may or may not know, members of the Federal Reserve are charged with influencing monetary policy, and one part of monetary policy involves the setting of interest rates.

So the SF Fed knew rates needed/were going to rise, their board members knew, and one of the board members ran SVB bank, and now SVB bank is no more. You see where I’m going with this?

Anyway, when the bank announced it sold investments at a significant loss in order to meet withdrawals, customers panicked. They opened their SVB app and started withdrawing even more money. That’s how $40B (or $28M every minute) left the bank on Thursday, March 9th.

There’s really two issues here. First: what made the board believe rates were going to fall when all indicators pointed to them continuing to increase? Second, how did they manage to botch the announcement of their significant loss so badly? Maybe the answer to the first question is as simple as: Hubris? Over-confidence?

Venturing a guess at the answer to the second question, I wonder if Becker, et al., weren’t able to see things through their customers’ eyes; the board imagined customers would react to the news exactly how they would have reacted: with confidence, clarity, cool, and with a full understanding of the bank’s financial position. “Look, we took a loss. It’s no big deal. Trust us. We’re still strong. ” Only it was a big deal, it’s clear their customers didn’t trust them, and, seeing as most of them had 100% of their capital at risk, they couldn’t wait to see if the bank was strong.

Which brings me to my point: you can be really smart, you can be smart-enough-to-run-a-bank smart, and still fail because your ideas are up against the masses. Millions of other people have their own perspective, feelings, biases, time-frames, and needs, all of which can get in the way of your success. As investors, it’s a lesson worth remembering.

Takeaway #3: Getting wealthy is easier than staying wealthy

I’m stealing this idea from Morgan Housel, who we refer to frequently. As he says in his book, The Psychology of Money, “(G)etting money and keeping money are two different skills. Getting money requires taking risks, being optimistic, and putting yourself out there. But keeping money requires the opposite of taking risk. It requires humility, and fear that what you’ve made can be taken away from you just as fast. It requires frugality and an acceptance that at least some of what you’ve made is attributable to luck, so past success can’t be relied upon to repeat indefinitely.”

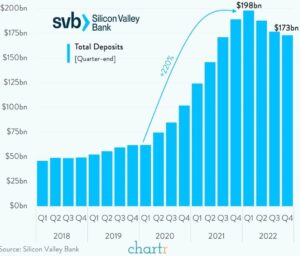

In 2018, SVB had $49B in deposits. By 2020, that number was $102B, and by 2021 it had swelled to $189B, before peaking just shy of $200B.

Their stock price reflected the growth in deposits: $246 per share at the beginning of 2018, and $678 per share at the end of 2021.

SVB had an abundance of optimism and risk-taking, but failed when it came humility, fear, and the acceptance that luck, not smarts, played a large role in their success. They behaved as if the heyday of the last few years was their new normal when it was just another bubble.

Applying this lesson to our own lives, it can be easy to look at one or two, even four or five good years as our new normal, and then increase our lifestyles in an unsustainable way. Remaining anchored to your values and goals is just as important, maybe even more important, in boom times than in normal times.

How the public views banks has changed in the last few weeks. The response from the Fed, FDIC and the Treasury have gone a long way in maintaining confidence in the financial sector. While we won’t know for awhile exactly what took place inside of SVB in the weeks and months leading up to the collapse, there are lessons that we can apply now to our own lives.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.