11 Aug 2022 Ripple Effects

Often in financial planning, one seemingly simple decision has ripple effects into other elements of your financial life that may not be obvious from quick glance. Sometimes the impact is more immediate and shows up on this year’s tax return. Other times the impact shows up 40 years later! As financial planners, we try to hold various priorities in balance and help you make the best decision based on the information we know now and what we know about your goals and long-term plan.

Qualified Charitable Deductions (QCDs) can be a powerful strategy that has ripple effects into other areas of your financial life. We’ve talked about QCDs before, often in our year-end planning reminders, as one strategy to reduce overall taxable income for those over 70.5. (Keep in mind that the Required Minimum Distribution (RMD) age is now 72, so there are different age thresholds for when an individual can gift to a charity from an IRA and when money must be withdrawn from an IRA for an RMD. These are the things we help you keep up with!) A QCD can count toward, or even completely fulfill, someone’s RMD. I won’t go into detail on this post about all the requirements and methods for giving via a QCD but please reach out to us if you have questions about your situation.

I’d like to show three different scenarios when giving via a QCD impacts more on a tax return than meets the eye. If you’re not yet to the age when QCDs are an option, I encourage you to continue reading anyway as this may provide insight into the general financial planning process. We often ask clients for copies of their tax return each year. This is one example of why that’s helpful to us as your financial planners.

Meet Sam and Stella Beacon. They are a married couple filing jointly and both are over age 70.5. These are hypothetical situations and are not based on any real person. The numbers would change for a single filer. These three scenarios with Sam and Stella highlight how changing their method of how they donate to charity ends up impacting their bottom line on a tax bill. We’ll compare the savings in each case study from giving via a QCD vs taking a taxable distribution, then donating and itemizing the deduction.

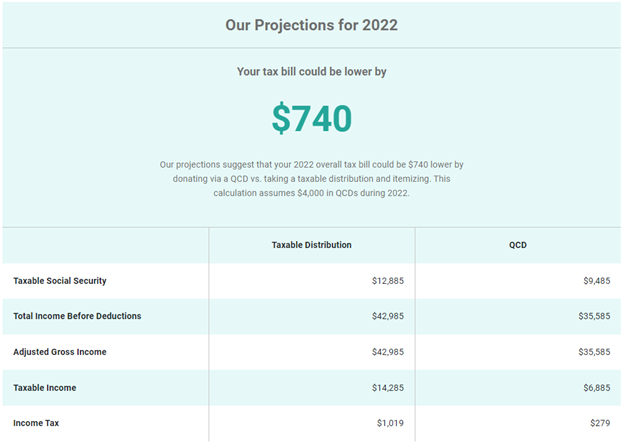

Scenario #1: Impact on Social Security Taxability

Sam and Stella Beacon’s income includes some earned income ($15k), interest and dividends ($5k), Social Security income ($44k), and IRA distributions ($10k). They will use the standard deduction of $28,700 (which includes the additional senior deductions) instead of itemizing, as they do not have high enough medical expenses, mortgage interest, or state and local taxes to itemize. They intend to donate $4,000 to a qualified charity. But what’s their best way to make that donation?

Because they are using the standard deduction, which is much higher than in years past, giving $4,000 from their checking account sadly doesn’t give them any tax benefit.

Instead, if they issue a check from either of their IRAs directly to a qualified charity, the couple’s taxable income is reduced. This gives them an above-the-line deduction which allows the charitable gift to reduce taxes without having to itemize deductions to receive a benefit!

The chart below shows how much this couple saves on their taxes by implementing the QCD strategy for their $4,000 charitable donation.

Part of the reason for the tax savings is because reducing their overall taxable income impacts how much of their Social Security benefit is taxable. Social Security benefits are up to 85% taxable, depending on total income. The QCD ended up shielding more of their Social Security income from being taxable, which helped contribute to that overall tax savings of $740.

Without QCD: $12,885, or 29%, of their total Social Security earnings of $44,000 was taxable as ordinary income.

With QCD: $9,485, or 22%, of their total Social Security earnings of $44,000 was taxable as ordinary income.

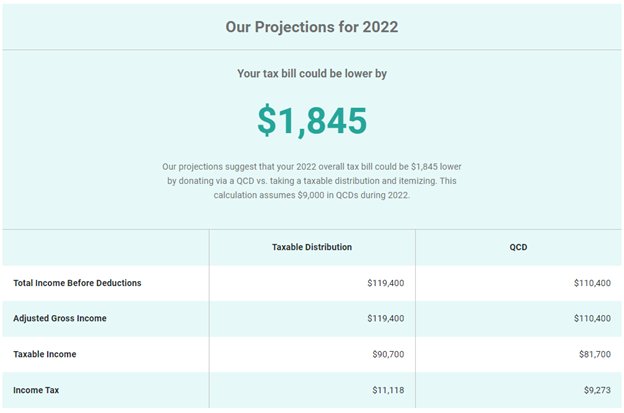

Scenario #2: Moving to a Lower Tax Bracket

Sam and Stella moved into a higher tax bracket than they were in Scenario #1. Stella loves her job and still works full time, so their total income now includes salary ($65k), interest and dividends ($2k), IRA distributions ($15,000), and Social Security benefits ($44k). They intend to give $9,000 to a qualified charity. Let’s look and see how the manner of the gift impacts their taxes.

They pay some mortgage interest and property taxes, but even with a charitable gift of $9k, their itemized deductions would be lower than the standard deduction. Their higher total income also means that 85% of their Social Security earnings are taxable, regardless of the method of the charitable gift. However, their marginal tax bracket does change depending on the gift method.

Without QCD: Their ordinary income totals $89,700. The income over $83,550 is taxed at 22%. They didn’t receive any tax benefit from the charitable donation since they use the standard deduction.

With QCD: If they give a QCD of $9k and take an IRA distribution of $6k, instead of the $15k IRA distribution described above, their ordinary income drops to $80,700, which keeps them from entering that 22% bracket. The total savings from the QCD strategy are $1,845! See below for the comparison.

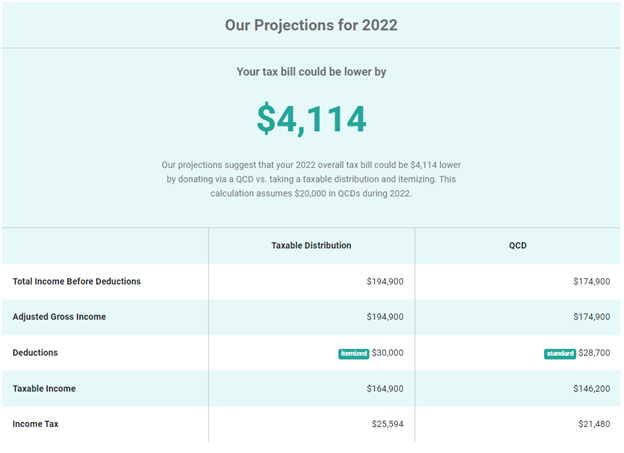

Scenario #3: Medicare Part B/D Premiums & Bonus: Itemized Deduction vs. Standard Deduction

Sam and Stella Beacon now moved up into the 22% tax bracket. They started saving aggressively at a young age and have substantial traditional IRAs that require large RMDs ($85k). They also have pension income ($35k), Social Security ($44k), interest and dividends ($7,500), and capital gains ($30,000). Unlike the previous two iterations of Sam and Stella, itemizing deductions may make sense for them. They paid $10k in state and local taxes and intend to donate $20k to a qualified charity, which brings their itemized deductions to $30k. Unfortunately, even with the itemized deduction, their Modified Adjusted Gross Income (MAGI) totals $194,400, which means their Medicare Part B and Part D Premiums will be increased in 2 years (there’s a two-year lookback for determining premiums). This is another one of those ripple effects I mentioned earlier.

However, Sam and Stella are wise and consulted their financial advisor before writing a check to a charity for $20k. Their financial advisor ran the numbers and showed that if they gift to the charity from their IRAs, they lose the ability to itemize deductions, but that ends up helping them save more on taxes! Also, their MAGI is now under the threshold of $180,000 so they won’t have a Medicare Part B/D premium surcharge in the future, based on this year’s income.

The tax savings are shown below. By donating via a QCD, they could save $4,114 on their taxes this year, PLUS the future savings from avoiding a Medicare Part B/D premium increase in a few years. That’s significant!

In the different scenarios, the decision about how to give to a charity ended up impacting Social Security taxability, marginal tax brackets, standard vs. itemized deductions, and Medicare premiums. Our income tax system is so intertwined that things that don’t seem to connect at all end up overlapping in meaningful ways. Be like Sam and Stella. Please keep us in the loop of the things going on in your life that impact your financial world. We’re always looking for opportunities to help you make wise and meaningful decisions. I hope this shows the potential value from taking the time to analyze various ways to accomplish a goal. If you want to learn more about using this strategy, please reach out to us.

The images are from hypothetical clients created in Holistiplan tax-planning software. The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.