12 Mar 2026 Mirror, Mirror

The most frequent response I hear from people when I mention having two boys in daycare is, “Just imagine the instant raise you’ll get when they’re both in elementary school!” Which is accurate, and helps me remember that this is just a short blip of time when the days are long and the years are short. Going from no kids to two kids in two years drastically changed our annual spending breakdown. A few years ago, I wrote a post reflecting on my family’s annual spending when we became parents, and I compared our spending relative to national spending figures. Now it’s two years later, we have two kids, just changed daycares at the beginning of the year, plus Wesley changed jobs, so I thought it was an opportune time to reflect back on 2025 spending to help give insight into where we would like to (or need to) adjust our spending in 2026.

In 2023, the spending categories I used came from the Bureau of Labor Statistics’ Consumer Expenditure Surveys, which track the earnings and expenditures of American households. They haven’t released data yet for more recent years due to a lapse in appropriations, but if you’re curious, here’s their most recent report I found. I decided to use the same categories now so that I could compare to my findings in 2023. These categories don’t perfectly align with my budget categories in YNAB, but it’s close enough. I only analyzed our spending from bank accounts, so there are a few real expenditures unaccounted for in this analysis, like income taxes and retirement savings.

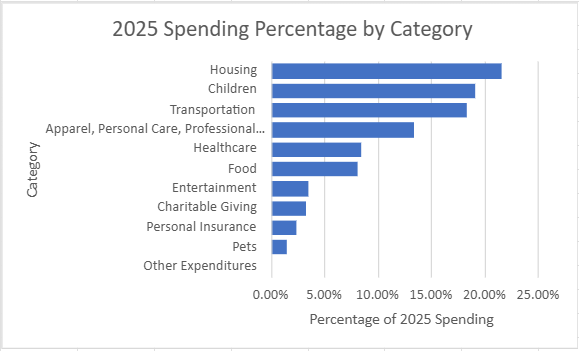

2025 Spending Percentage By Category

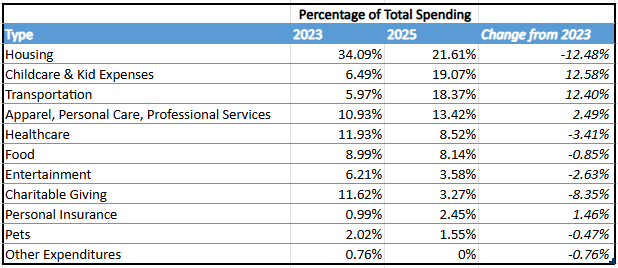

2023 vs 2025 Comparison

I feel fairly vulnerable showing this mirror to the world as some of the data does not reflect what I hoped to see. Our top 3 spending categories changed pretty dramatically between 2023 and 2025. Healthcare and charitable giving dropped off the top 3 in 2025, making room for childcare and transportation in their place. This makes sense, as we were not enrolled in daycare in 2023, and now we have two kids in daycare. Plus, in 2025, we purchased a van outright from our savings, so that skews the numbers. I anticipate transportation falling way back down the list in 2026.

Spending often reflects your real values, and it feels a bit uncomfortable to see that categories that matter to me (like giving) make up a smaller percentage of our overall spending. I also have to remember that we probably spent more than our take home pay, as we spent from our savings on a car plus house projects, which means these percentages of spending are different than percentages of our income. But regardless, our priorities clearly changed over the past few years.

I want to be mindful of that shift as we approach our budget in 2026, and as we, in just a couple years, will find ourselves without a large chunk of our spending going toward full-time childcare. I feel acutely aware that we are in some precious years in our family when we all, right now, are healthy and live in relatively close vicinity to each other. I want to prioritize making memories with extended family which means entertainment (that includes vacations) should be a greater part of our spending. I also hope giving pops back up, since we don’t have as many anticipated one-off large expenses. I already adjusted some of our recurring gifts accordingly when I realized the actual spending no longer matched our goal. We also are trying to be more generous to our community in ways that don’t count as charitable giving for taxes, but do matter for living a generous life and modeling that to our boys. But here I go trying to justify myself to you due to my uncomfortableness!

This exercise in looking in the mirror showed me that I am indeed not the fairest in all the land. I have some real takeaways though, and that makes the exercise worthwhile.

- Increase our recurring giving: Done, and set a year end reminder for myself to check in on this.

- Plan visits to loved ones: Now that we have the van, it’s easier to go somewhere and we want to prioritize memory making. One trip booked, more to come…

- Increase retirement savings: I didn’t show this part of my analysis above, but I also reviewed how much of our income is going to savings. We need to adjust this after a job change.

- Think ahead and dream: We will likely feel a future “raise” after daycare ends in a few years. Are there savings we’re foregoing now in order to pay for higher expenses? Or are there ways we can redirect those funds to other goals to align our values with spending? Or a combination of the two? What even are those future goals?

There is always more to the story not captured by a snapshot. Am I spending less time worried about finances? Is my current spending aligned with values and long-term desires? What is getting in the way of those long-term goals? What is the context surrounding changes in my spending? Am I constantly moving the goalpost forward to the point where I’m never there, wherever there is? What is enough, anyway?

Maybe I’ll be brave enough to go through this public exercise again two years from now. Until then, I hope this encourages you to take a glance at your own mirror and see if it reflects what you thought you’d see.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information