28 Aug 2024 Mind the Investor Gap

Jason Zweig of The Wall Street Journal is one of my favorite financial writers. Zweig recently wrote a piece that hit home for me: Messing Up the Closest Thing to a Sure Thing in the Stock Market. While the entire article could be quoted, I wanted to touch on a few things in particular. His key point is that “if you buy a handful of index funds, sit on them for decades and never do another thing, you’re likely to outperform nearly everyone who tries to beat the market by trading—including most professionals.” This, as Carl Richards has also explained in the past, is the behavior gap: The idea that certain behaviors are keeping investors from making better returns.

The part that interested me most in Zweig’s article is that this gap isn’t just a byproduct of actively trading individual stocks vs not, but also utilizing index funds in a suboptimal way. Investors may be tricked into thinking that if they are buying and selling index funds then at least they aren’t risking individual positions. Unfortunately, the data shows that they may be causing more harm than good. Zweig hits on the important psychological aspect of this: “But what’s the fun in that? Can you endure a lifetime of barbecues and cocktail parties where other people brag about their winning trades and all you can do is mutter, “Umm, I own index funds and I haven’t made a trade in a decade”?”

The data tells a compelling story: “Over the 10 years ended Dec. 31, 2023, Morningstar found, investors in the aggregate earned an average of 6.3% annually, or 1.1 percentage points less than the mutual funds and ETFs they owned.” The number is even worse for more complex index funds: “Over the 10 years ended last Dec. 31, investor returns fell behind total returns at sector index funds by 2.9 percentage points annually—even worse than the 2.0-point gap at actively managed sector portfolios. When you shoot for the moon with sector index funds, you stand a good chance of shooting yourself in the foot.”

So, what can we do with all of this information? A few quick thoughts.

- Timing Matters – A big factor in the lower-than-expected returns for these investors is that they buy and sell at the wrong time. They chase high returns, but get there after a fund has already taken off. A great example of this is the difference in returns for ARK Innovation (ARKK) as a fund vs what the typical investor received. The fund returned 9.7% on average since 2014. For the investors? Their average return was -17%. It all comes down to timing: so many of the investors bought the fund after it had already experienced high growth.

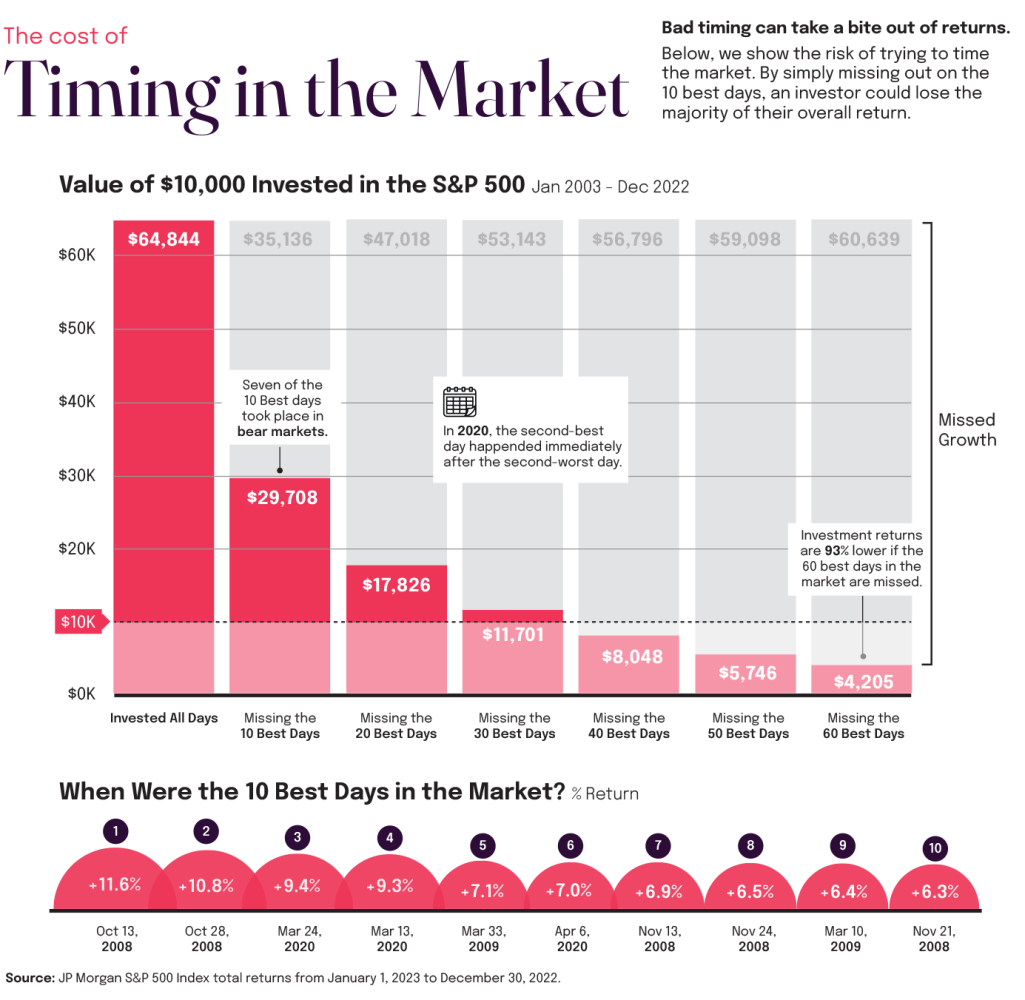

- Longevity Matters – A common phrase related to the stock market is that time in the market beats timing the market. All you have to do is look at this chart from JP Morgan to see how missing some of the best market days can be detrimental to your returns. You will also notice on the chart that so often the best days happen in the most volatile or down markets (2008, 2009, and 2020). Being invested, and staying invested, is half the battle.

It can be hard to not try to time the market by selling when things look scary or only buying when it looks like things are shooting up. These are normal human impulses. However, timing and longevity come together to emphasize discipline when it comes to your portfolio. If you are a Beacon client, you are familiar with these pieces of the puzzle and how they impact your financial plan. We are always here to be your advocate for staying the course over the long term and helping you build a portfolio that is right for you. We are also here to talk whenever the market volatility is causing you unneeded worry. Take heart in the long term approach to investing.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.