07 Mar 2024 How Earning Less Impacts Social Security Benefits

Last week I met with a client who is thinking about reducing his income. Obviously, there’s a lot that goes into this decision, but one consideration we discussed is how less pay will affect his Social Security benefit. This kind of exercise can be helpful for someone looking to ease into retirement by reducing the amount they work over time, or in the case of someone self-employed who can adjust (within reason and with the help of a CPA) how much of their income is subject to Social Security taxes and how much is not.

If you are unfamiliar with how Social Security benefits are calculated, the very simple explanation is that the Administration runs your highest 35 years of earnings through their calculator in order to project the amount you’re entitled to receive at your Full Retirement Age. A more complicated explanation can be found here and includes neat terms like “average wage level,” “average wage index,” and “average indexed monthly earnings.” I know that sounds boring, but by clicking on the link you’ll find it’s actually worse.

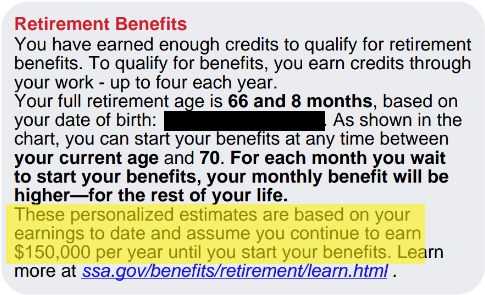

In addition to considering your high-35, Social Security also assumes you will continue earning the income you last reported to the IRS. For example, if you earned $150,000 in 2023, the benefit you see listed on your Social Security statement assumes you will continue earning that amount until you begin claiming benefits, whether that’s 62, your Full Retirement Age, or 70. This is how it looks on your statement:

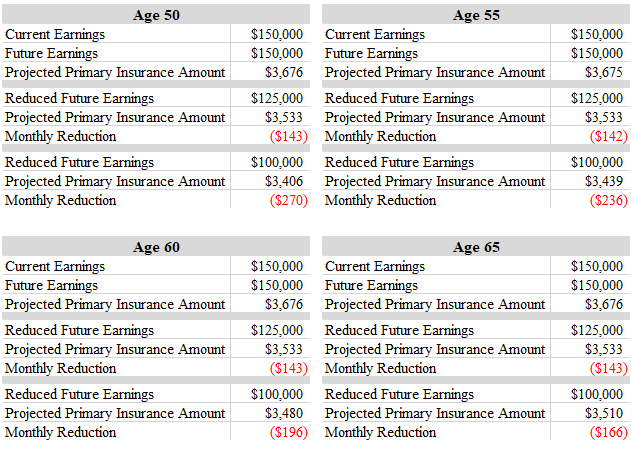

The answer to how much a reduction in pay impacts Social Security can be complicated. For our purposes today, we will use very simple examples and all dollar amounts will be in today’s dollars. Below you will see four individuals, each of whom earns $150,000 a year and has throughout their entire career. They are considering earning less so that their salary drops to either $125,000 or $100,000. They plan to claim Social Security at their Full Retirement Age of 67. The only thing different about them is their ages: one is 50, another is 55, another is 60, and the last one is 65. Below you can see their projected benefit (Social Security calls this their “Primary Insurance Amount,” or PIA) as well as the reduced benefit at reduced income levels:

A couple of things to point out about this hypothetical: First, the younger you are when your earnings drop, the greater the reduction in benefits. Second, as I said, this is a simple example. Is it realistic to assume a person earns the same generous salary year-in-and-year-out with no interruptions? Or that their first year salary was $150,000 (adjusted for inflation)? Third, only looking at the monthly amount can be misleading. Yes, we might tell ourselves, $200 a month less isn’t great, but it’s not too bad. Over 20 years, however, that missed income adds up to more than $50,000, and that is before you factor in Social Security’s annual Cost of Living Adjustment (COLA). Fourth, if this individual is married, there’s a chance a reduction in his benefits could reduce his spouse’s benefits, compounding the impact.

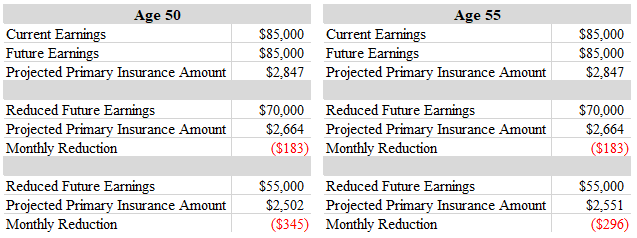

In sum, reducing income between 17-33% results in a 4-7% reduction in benefits, which is less than I anticipated. This is due to how Social Security is calculated, where earnings of more than ~$85,000 count less heavily. Which begs the question: What happens if peak income is $85,000, followed by reductions of $15,000 or $30,000? Let’s look at two examples:

As you can see, a similar reduction in income results in a far greater reduction in benefits. At the top end, benefits are reduced by more than 12%. In both examples, the reductions aren’t insignificant though how much it affects a financial plan depends on the situation.

If you are a business owner considering this (optimizing the mix between salary and distributions), it’s mostly a math problem–how much will it save you in taxes versus how much will it reduce your PIA–with a dash of behavioral finance–will you invest the tax savings so your portfolio can replace what you lost from Social Security, or will you spend it? If you’re nearing retirement and looking to scale back, there are other considerations: Can you maintain benefits, especially health insurance (pre-Medicare)? Have you accumulated enough savings? Will you need to start withdrawals from your portfolio earlier than planned? What will you do with the extra free time? How will your spouse’s benefit be impacted?

Over the last few years, the Social Security Administration has greatly improved their website. If you haven’t already, I suggest you create an account. Once you’ve logged in, you can see your earnings history, projected benefit at different ages, and you can even model how your benefit will change based on changes to your income. I spent time in my account earlier this week and here’s a screen shot of their easy-to-use modeling tool:

In closing, earning less can impact your Social Security benefit. How much, and how consequential, depends on your unique situation. Answering these questions is exactly why we’re here.

As always, reach out to us if we can help.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.