27 Jul 2023 Hospitals, Baker, and Bills – Oh My!

Before our son Baker was born in March, I often wondered what a labor and delivery bill looked like. How much is charged? How many providers will send me bills? How can I be sure they are all in-network? What am I personally liable for vs the insurance provider? What happens after you meet your deductible (which I’d never done before)? Is it better to use HSA savings or pay from other savings? For those curious like me, here’s an overview of how we were charged for labor and delivery with a high deductible health plan, and how we paid for our portion of expenses.

We have a high deductible health insurance plan with an HSA through Wesley’s employer and knew that we would meet our family deductible of $5,400 this year. For a health insurance plan to meet the requirements of being a high deductible health plan (HDHP), the family annual deductible must fall within a range of $3,000 – $15,000 for 2023. So, our plan’s deductible is on the lower side of a high deductible. It also has a max out-of-pocket expense of $10,000, although I was unsure what types of medical charges would get us to that additional maximum. The plan documents state the general types of services that require coinsurance after deductible but that gives minimal insight into what that means in the real world.

What we were charged

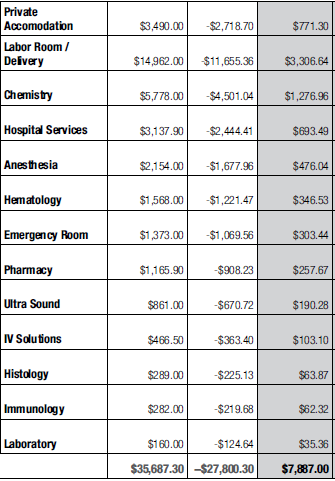

Below is a snapshot of the insurance Explanation of Benefits from my main hospital claim. I had a longer stay than average due to complications, so I would guess these are probably on the higher end of charges assessed for labor and delivery. The 3 columns show: amount your health care provider charged, Blue Cross discount, and the allowed amount in gray.

What does this show us?

- The hospital billed $35,687 for my stay.

- BCBS has allowed in-network rates, which reduced the total cost by $27,800. (Medical billing is incredibly complex and insurance adjustments are all contracted rates…I won’t be able to provide insight into how those are negotiated between providers and insurance companies – although I bet many of our readers know much more on that subject!)

- This left $7,887 as the final charge for my initial hospital visit for labor and delivery.

Not pictured:

- The hospital billed $4,587 for Baker’s care (even though he was 5 weeks early, he did not need NICU care).

- We also received a separate anesthesia charge for $3,600 before BCBS contracted rates adjusted the bill to $1,254.

- My OB’s office charged $3,989. I did know this amount ahead of time!

In summary, our allowed costs for labor and delivery totaled $17,717. We did not incur any coinsurance expenses from that stay, so we just owed our deductible of $5,400, with insurance fully covering the remaining $12,317. But if were on a different health plan with the maximum allowed high deductible, we could have been liable for $15,000 of the $17,717.

How we paid for our charges

Average health expenses for different billing codes are available on the NC Department of Health and Human Services website but unless you’re in the business of medical billing or insurance, I found the information fairly unhelpful and difficult to navigate. Providers can also give you cost estimates before known procedures but lots of medical things happen without much advance warning. Understanding your health plan and savings methods is one way to help reduce unexpected surprises in case of emergencies.

A Health Savings Account is offered with high deductible plans and can provide triple-tax savings. You can contribute with pre-tax dollars via payroll, grow tax-free earnings, and take tax-free distributions for qualified medical expenses. Or, once you are 65, you can use HSA funds to pay for nonqualified medical expenses, although those distributions are taxable much like a Traditional IRA. In 2023, the HSA contribution limit for family coverage is $7,750, which includes both employer contributions and employee contributions.

We knew we’d be liable for at least $5,400 in medical expenses this year. At a minimum, we needed to contribute $5,400 to the HSA to get the best tax benefit on that expense. If our estimated tax rate is 22%, we save $1,188 in taxes by contributing pre-tax dollars to the HSA and paying our bill from that account. It may be tempting to contribute a minimal amount to your HSA so you receive more take-home pay. As counterintuitive as it may seem, if you have a sense of your estimated annual health expenses, you can save on taxes owed by contributing pre-tax dollars to your HSA, then paying your qualified medical bills with those funds.

In our situation, we had already set aside other regular savings for health expenses to pay for this bill without using HSA funds. We still contributed to our HSA to receive the tax benefit and continue growing those assets. With this approach, we keep funds in the HSA for use in the future. Over the past several years, we’ve worked to save 2 years of our health insurance deductible in cash in our HSA. Then we just started investing the amount above that threshold. That way, if we have an emergency and need to access funds, we have protected a certain amount in cash while still growing funds with a longer time horizon.

All this to say, health expenses can get confusing quickly and you often don’t know what you are liable for until after the fact. A high deductible health plan may not make sense for your situation, and strategies for saving to and spending from an HSA differ depending on individual situations and goals. Billing often feels opaque and the amount of information you get from calling your insurer may vary depending on who you get on the phone. Health expenses in particular are not very straightforward, and I hope this transparency in our expensive health care year offers some clarity in various ways to approach it.

As a reward for reading to the very end, here’s a picture of our previously 4 lb 10 oz preemie on a recent visit to the Beacon office. Worth every penny! We had a great experience with excellent care, which was a blessing during a stressful time.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.