12 Jun 2020 A Proclivity For Panic or a Propensity For Patience

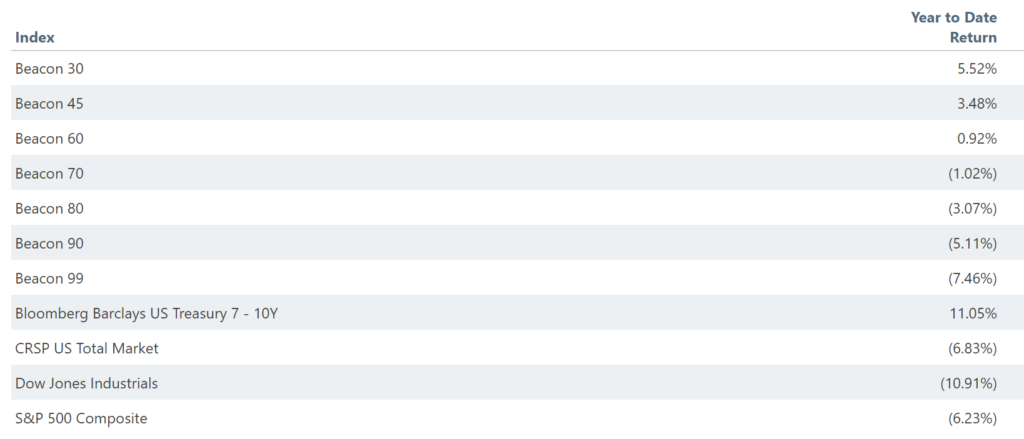

It’s hard to believe that the stock market, as measured by the S&P 500 at the end of the trading day on Thursday, was “only” down 6.23% year-to-date in 2020. This after it fell 30% in just 22 trading days – the fastest 30% decline ever from an all-time high – on fears of economic damage brought on by the global pandemic. The precipitous drop in February and March was followed by an incredible 40% rebound lasting through this past Monday.

Here’s a quick look at the at how the indices that comprise our Beacon Model portfolios have been doing relative to the stock market. After yesterday’s nearly 6% drop, the stock market as measured by the S&P 500 had fallen 6.23% for the year, but the sum of the indexes that comprise the Beacon 60 model portfolio (60% stock, 40% bonds) was actually up .92%.1

The speed and magnitude of the recent run-up has left many people asking whether it’s been too much, too quickly. Is the stock market being overly optimistic about the future prospects of the global economy? After all, much is still unknown about how the ongoing Covid-19 crisis, the current levels of civil unrest, the upcoming elections in the U.S., and the U.S government’s massive stimulus packages will impact the global economy and therefore the stock market going forward. The best answer, and least satisfying one, is nobody knows. While we can’t predict the future, we can learn some valuable lessons from the past that could help prepare us for the times ahead.

An important investment decision is how much stock to own in your portfolio. You want to ensure that you own enough to generate the return you require so you can accomplish the things in life that are important to you and your family. At the same time, it’s important to make sure you aren’t investing so much in stocks that you’re unable to stick with your investment plan during good times and bad.

Creating and maintaining a good financial plan can help answer the question of how much risk you need to take but how can you discover how much risk you should take so that you can survive the inevitable ups and downs that come with any sort of stock market investment?

For years, financial advisors have used a tool called a risk tolerance questionnaire to aid in their quest to figure out, ahead of time, how a person might react to sharp downturns in the stock market. Risk tolerance questionnaires are only marginally effective because most people have a hard time projecting themselves into specific situations in the future and recent studies have shown that our tolerance for risk actually changes based on our current circumstances.

Yes, there have been advances in risk tolerance measurement in recent years like the introduction of Riskalyze – a virtual tool we use here at Beacon – which seeks to make future market conditions more salient via powerful visuals and examples of market downturns in both dollar and percentage terms. But, could there be a better way to discover our proclivity for panic or our propensity for patience during times of market upheaval?

I’ll submit that the “opportunity” to experience a sharp downturn in the market followed by an equally sharp recovery may offer us the unique opportunity for a do-over of sorts. Now would be a good time to reflect on your experiences over the last few months and address any questions or concerns that arise. Here is a list of questions you might consider…

– How did you feel during the stock market’s steep decline in March? If you were having trouble sleeping at night should you reduce the amount of stock in your portfolio?

– But before you make such a change you need to answer this: How much risk to you need to take in your portfolio to accomplish the things that are important to you?

– Are you getting closer to retirement and planning to reduce your exposure to stocks as part of your overall financial plan? Now could be a good time to have that discussion with your financial advisor.

– Did you have money that you’ll need to spend in the next couple years in a 529 college savings account, or other shorter term account, that was invested too aggressively?

Your answers to these questions will be a good starting place for a conversation with your financial advisor. It’s important to take into account all the potential ramifications of making changes to your portfolio before doing so. Things like the impact on your financial plan, your tax bill and your future return potential.

One last thing. This isn’t an endorsement for attempting to time the market over the short-term. One of the keys to successful investing is to develop a prudent, long term investment plan and stick with it over the years. This is more about taking advantage of your experiences over that last couple of months to make sure your long-range investment plan fits your personality and your financial plan.

As always, please let us know how we can help.

1 The chart represents actual index movements, which may be slightly different than portfolio values due to fees and differences between the exchange traded fund values we own and value of the indexes at any given time. Past performance is no guarantee of future results.