12 Dec 2024 2025 Contribution Amounts, Tax Bracket Changes, and Social Security Increases

We are close to year-end so we wanted to provide an update on 2025 tax brackets, Social Security benefits, and retirement plan contribution amounts. In addition, certain provisions of the SECURE Act 2.0 take effect next year so be sure to read to the end to see if they impact you.

Here’s what’s coming in 2025.

Social Security Cost of Living Increase (COLA)

The COLA for 2025 will be 2.5%, down from 3.2% in 2024. Citizens who qualify for benefits and are between their full retirement age and 70, and who aren’t yet receiving benefits, will get the COLA plus delayed retirement credits (DRC) of 8%.

For those still working, the amount of income subject to the 6.2% Social Security tax paid via payroll deduction will rise from $168,600 to $176,100, an increase of $7,500.

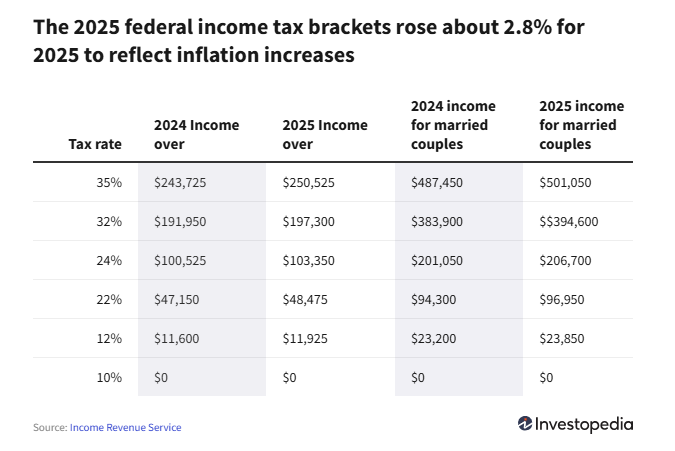

2025 Tax Brackets

The upside to the high inflation we experienced in 2022 and 2023 was that tax brackets increased significantly, meaning the same amount of income from one year to the next resulted in a much lower tax bill in the latter year. With inflation now mostly under control, tax bracket increases are back to normal: The increase from 2024 to 2025 will be 2.8%:

The standard deduction for a single filer projects to be $15,000, or $30,000 for married couples filing jointly.

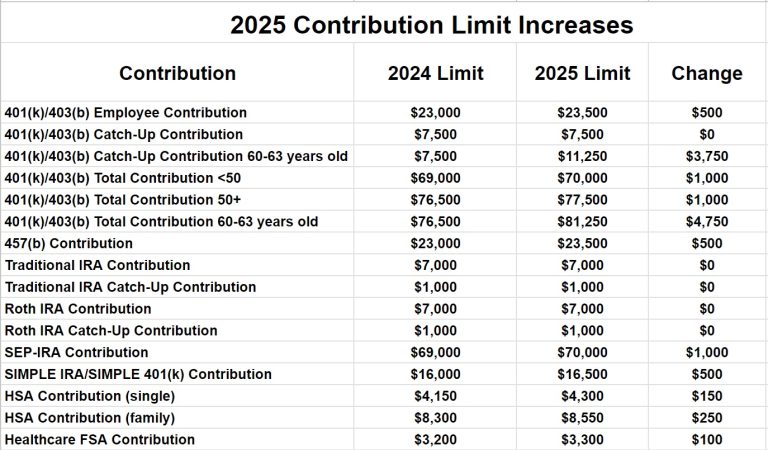

Retirement Plan Contribution Amounts

The table below, courtesy of the White Coat Investor, displays new contribution limits for various retirement and tax-advantaged accounts. Be mindful that there are eligibility rules you must meet to contribute to these accounts, so reach out to us with any questions.

Lines three and six are new this year and display the total catch-up contribution for someone age 60-63. This new contribution type was passed as part of the SECURE Act 2.0 and 2025 is the first year it takes effect. If you turn 60 or will be 61, 62, or 63 at some point next year, be sure to log into your 401(k) website soon to elect the higher contribution amount (provided your cash flow can tolerate it, of course).

Another feature that goes live in 2025 is that some employers will provide a 401(k) matching contribution for student loan payments that an employee makes. Education debt continues to be an issue for young employees so this feature could allow employees to accrue a 401(k) balance while tackling their debt. Not all employers will offer it but if you have student loan debt, be sure to check with your benefits department.

As always, please reach out to us with questions and have a great weekend!

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.