03 Oct 2024 Mailbag: What should our net worth be?

A few weeks back I received the following email from a client in his early 40’s, which he gave me permission to share:

I would like to update (our net worth) if possible…it’s motivating to look at and gives me something to push towards. No idea what the number should be at retirement but would love to see it realtime. Do you have any idea what the number should be at retirement? (P)robably subjective based on the lifestyle we want to live, right?

Net worth is an easy number to calculate: add up what you own, subtract what you owe, and whatever is leftover is your net worth. Depending on where you are in life, the financial decisions you’ve made, the luck/good fortune you’ve had, that number can be satisfying or frustrating. So while it is easy to calculate, it can be hard to interpret because, as a standalone figure, the sufficiency of your net worth is largely tied to other numbers, as my client rightly points out.

Rather than focusing on one number and what it should/shouldn’t be, here are five that you can use to get a better sense of your overall financial health:

Net Worth: what you own less what you owe.

There’s a story behind everyone’s net worth. In speaking with clients, it’s always interesting to learn about the decisions that got them to where they are today. If you’re early in your career, you might not be too impressed by your net worth, and that’s alright! (We’ll talk about human capital in a few paragraphs, which is more important to focus on when you’re young and just starting out.) If you’re later in your career, it can be easy to be myopic about your net worth when, again, it won’t on its own tell you much.

When looking at a statement of net worth, it’s important to look for liquidity and diversification. Liquidity refers to how quickly an asset can be turned into cash. Obviously, checking and savings accounts are 100% liquid, brokerage accounts are liquid, too, but there may be taxes involved. IRAs and 401(k)s are less liquid, while real estate and businesses are highly illiquid. Illiquid assets aren’t inherently bad, but a net worth filled with them can result in a financial plan unable to adapt. Diversification refers to owning assets of different types: cash, brokerage accounts, IRAs, 401(k)s, real estate. There’s no perfect mix, but it is helpful to avoid being too heavily tilted towards one.

Monthly Expenses: total spending per month, ideally broken down into fixed and variable or wants and needs

Simply put: tracking your spending is one of the most–maybe the most–important financial habit to have. There are a few reasons for this. First, reliable spending data ensures a financial plan that is grounded in reality. Second, it lets you know what you need to have in cash reserves, i.e., an emergency fund. Third, when income is variable, you can plan better. Fourth, in the event you need to cut back on spending, you know which categories (eating out, Amazon, travel, etc.) to target. Finally, you’re able to see if your spending aligns with your values.

Ideally, spending is such that there’s a gap between it and income, giving you flexibility to handle unexpected expenses and the opportunity to give and save. If not, or if expenses exceed income . . . well, you won’t know unless you’re keeping track!

Debt Ratio: total debt payments (mortgage, auto, student loan, HELOC, etc.) divided by gross income.

There’s no hard-and-fast rule for how much of your income can safely be devoted to debt payments. Mortgage lenders typically want to see a ratio around 40% in order to qualify for a loan, but getting a loan and having healthy cash flow are two very different things. Because of this, how much debt you can tolerate depends. For example, a couple paying for private school or that prioritizes generosity or experiences will have less capacity for debt. Same for someone targeting a high savings rate.

A high debt ratio is an enormous influence on the rest of your financial life. It contributes to a low savings rate, high monthly expenses, and can cause you to feel trapped in a job you might otherwise leave. Most frustratingly, it takes up dollars you could be using to make memories with friends and family. As with any kind of financial commitment, but especially one that adds debt, it’s crucial to plan and give yourself margin.

Savings Rate: total goal savings (401(k), IRA, brokerage, cash accounts for short-term goals, etc.) divided by gross income.

A reliable indicator of future financial health is your savings rate. I wrote a brief a few years ago that provided examples of how much someone making $100,000, $200,000, and $300,000 would need to save in order to have a healthy retirement. Two of the takeaways: the old maxim of saving 10% of your income no longer works (it needs to be higher), and the more you make, the higher your savings rate needs to be.

An adequate savings rate is a reliable indicator because not only does it mean you’re saving a lot, it usually means your spending is under control, too. On the flipside, some people save more than they need to which, again, is why it’s important to not be singularly focused on one number.

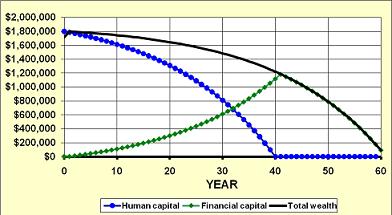

Human Capital: current annual salary times remaining years of work.

For those early in their career, it’s common to have a net worth of $0 or negative, especially as more students graduate college with significant amounts of debt.

Human capital is important to understand for a few reasons. First, to help young people in their 20’s and 30’s avoid being discouraged about a lack of assets. Second, when you realize your earnings are finite, you understand the importance of converting human capital into financial capital via saving and investing. Third, you can measure the impact of earning a higher salary, either through promotions or additional education. Michael Kitces, who we cite often, has this to say about human capital:

“(T)he accumulation of financial capital over time represents not so much the ‘creation’ of financial capital by saving, but simply the conversion of human capital to financial capital…. So why does all of this matter? It matters because, as the graph shows, human capital is actually the greater asset on the client’s balance sheet for most of his/her working career.”

I love how he phrases it: “…not so much the ‘creation’ of financial capital by saving, but simply the conversion of human capital to financial capital….”

Hopefully you are able to see that these five numbers are inextricably linked. A large net worth is obviously great, but is less meaningful when married to too high a lifestyle, and you won’t know your lifestyle unless you track spending. Debt can be necessary, but too much crowds out more enjoyable spending, limits your ability to save and give, and makes budgets tighter and less adaptable. A high savings rate is usually a positive, but sometimes you can save too much and miss out on opportunities to enjoy the fruits of your labor. Conversely, if savings is too low, what’s contributing to it: Fixed expenses? Debt? Wants? Finally, being reminded of your human capital, especially that it is finite, and the need to convert it to financial capital can make saving for long-term goals easier.

So, back to the original question: What should your net worth be? My honest-yet-deeply-unsatisfying answer: it depends. Just remember that while your net worth does tell a story, it doesn’t tell the whole story. So don’t spend too much time focusing on that one number and consider the other four to get a better sense of your financial standing.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.