27 Jan 2022 Stock Market and Beacon Portfolio Updates

Through Wednesday, January 26th, the S&P 500 index is down 8.7%, which, obviously, is not a great start to the year. (Average January returns going back to 1980 are +.82%.) While prices are down, volatility is up: we’ve already had 6 trading days where the market moved 2% or more. The Dow has had four days where it moved in a range of 800+ points, with two of them exceeding 1,000. 2021 was a remarkably average year when it came to volatility in the stock market, but thus far, 2022 is the opposite.

In today’s Brief I want to highlight three factors that are impacting the market now and that will also play a key role through the rest of 2022. I’ll also provide an update on how our Beacon portfolios are performing.

The Fed

By “the Fed” I’m referring to a host of factors because right now they have a lot on their plate: inflation, interest rates, and decisions surrounding monetary policy.

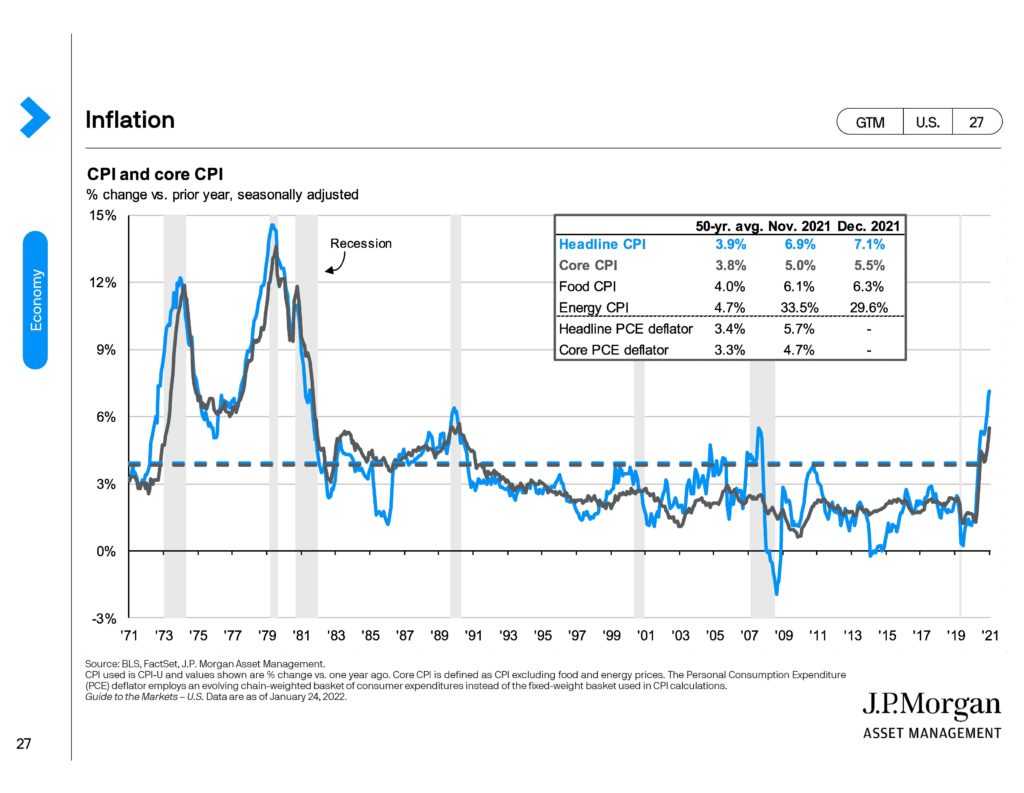

Much digital ink has already been spilled over inflation, with good reason. Prices have been rising at quite the clip, as you can see from the chart below:

(“Headline CPI” refers to the entire “basket of goods” the Fed surveys to determine the rate at which prices are changing. “Core” strips out two components: energy and food.)

Once thought “transitory”, the Federal Reserve now acknowledges it to be a bigger issue, one they plan to tackle with interest rate hikes beginning in March. After the Fed’s meeting on January 26th, where Chairman Jerome Powell indicated that inflation continued to run higher than anticipated, he had this to say: “To the extent the situation deteriorates further, our policy will have to address that,” which leaves the door open for frequent and possibly more aggressive rate hikes. The sooner inflation is tamed the better but it’s not an easy problem nor one the Fed bears sole responsibility for. Supply chains problems and worker shortages are two additional problems that must be solved.

To combat inflation, the most effective tool at the disposal of the Federal Reserve is to increase interest rates, as mentioned above. But increasing rates has the side-effect of negatively impacting bond prices, which is what we’ve seen over the last 13 months. In 2020, U.S. Treasuries returned 8% and corporate bonds returned 9.9%, but in 2021 both were negative: -2.3% and -1%, respectively. The Fed clearly communicating their strategy and avoiding surprises will prevent any unnecessary shocks to the fixed income market.

Finally, monetary policy. During the first 12 months of the pandemic the Federal Reserve injected trillions of dollars into the economy to protect against what they feared could become a depression, and they are now faced with the unenviable task of withdrawing much of that. Reducing the money supply slows the economy and can help in the battle against inflation, but it’s not a tactic that is kind to stock market investors. Here’s Chairman Powell again: “This is going to be a year in which we move steadily away from the very highly accommodative monetary policy that we put in place to deal with the economic effects of the pandemic.” (Emphasis is mine.)

Market Leaders Lagging

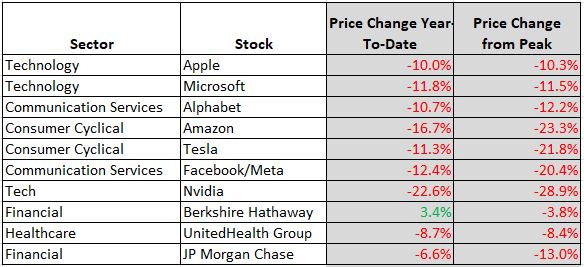

The top ten stocks in the S&P 500 are not having a good start to the year; for a few of them, this continues a trend that begin in the fourth quarter of last year. Here is their year-to-date performance through Wednesday, January 26th, as well as their performance from their most recent peak:

With the exception of Berkshire and JP Morgan, all trail the overall stock market this year. Because these 10 stocks make up 30% of the S&P 500 (as of 12/31/2021), they have an outsized impact. Six of the ten are in “correction” territory (decline of 10%+). From their peak, four are in a “bear market,” having declined more than 20%.

Stepping back from individual stocks, it’s also notable what’s taking place amongst the different styles of investing. Growth investing, led by technology stocks, has dominated value investing for more than a decade but value is the clear leader this year (upper right tic-tac-toe box):

Pandemic Reset

Looking back over the last two years, it’s clear the actions of the Federal Reserve inflated stock prices. I don’t mean that as an indictment, maybe stocks would have done alright without the help, but to acknowledge that the trillions of dollars put into the financial system pushed prices to levels they would not have otherwise reached. One look at the performance of the top ten stocks in the S&P 500 over the last two years should be enough to get the point across, but here are two other glaring examples: Zoom and Peloton.

Looking at the chart below, Zoom zoomed (sorry!) from a price of $73.59 in January, 2020, to $559 nine short months later. The same goes for Peloton: From $28 per share in January, 2020 to $162 by December of the same year. Whether they believed it or not, investors behaved as if the conditions caused by the Pandemic were creating a fundamental, eternal shift in how people worked and worked out. Recently, the Wall Street Journal did a podcast discussing Peloton’s troubles and it’s clear, in my opinion, the CEO was drinking a little too much of his own cool-aid when he predicted one-in-every-six Americans would soon own one of their bikes. One-in-six! Yet, investors believed it. For a while.

Full disclosure: We use Zoom at work and I own a Peloton. I love both products. This isn’t a recommendation to sell or buy either stock. Zoom has still been a great investment over the last two years but we cannot deny the impact of Fed policy and how we initially thought the Pandemic would change how we live our lives.

All this to say, as life (slowly) returns to normal, as Fed policy becomes less accommodative, and as inflation continues to impact our purchasing power, there will be a settling in stock market prices. Stocks that have lagged (value? financials?) may start to outperform. The winners of the Pandemic may struggle.

None of this is said to startle you, but rather to bring attention to the fact that we may be entering a more challenging period as investors. As always, if you have questions or concerns, call us. And if you aren’t yet a client but are curious what it’s like to work with us, click here to schedule a time to chat.

The content above is for informational and educational purposes only. The links and graphs are being provided as a convenience; they do not constitute an endorsement or an approval by Beacon Wealthcare, nor does Beacon guarantee the accuracy of the information.